The Hong Kong intermediate layer is the structure foreign founders read about, half-understand, and then either over-adopt or wrongly skip. Real holding structures with substance produce real treaty benefits; paper structures with a Cayman-style shell director produce overhead and disqualification. The 2018 HK-PRC tax arrangement revisions and the 2022 mainland anti-treaty-shopping enforcement under the General Anti-Avoidance Rule tightened what "substance" actually means.

This article walks through when the layer earns its keep, the timeline and cost to set it up, what substance the mainland tax authority will require to grant treaty benefits, the dual-track banking reality in 2026, and the operating-size band below which the layer is pure overhead. Written for the founder weighing whether to register HK Ltd → WFOE or to skip straight to a direct foreign-parent → WFOE structure.

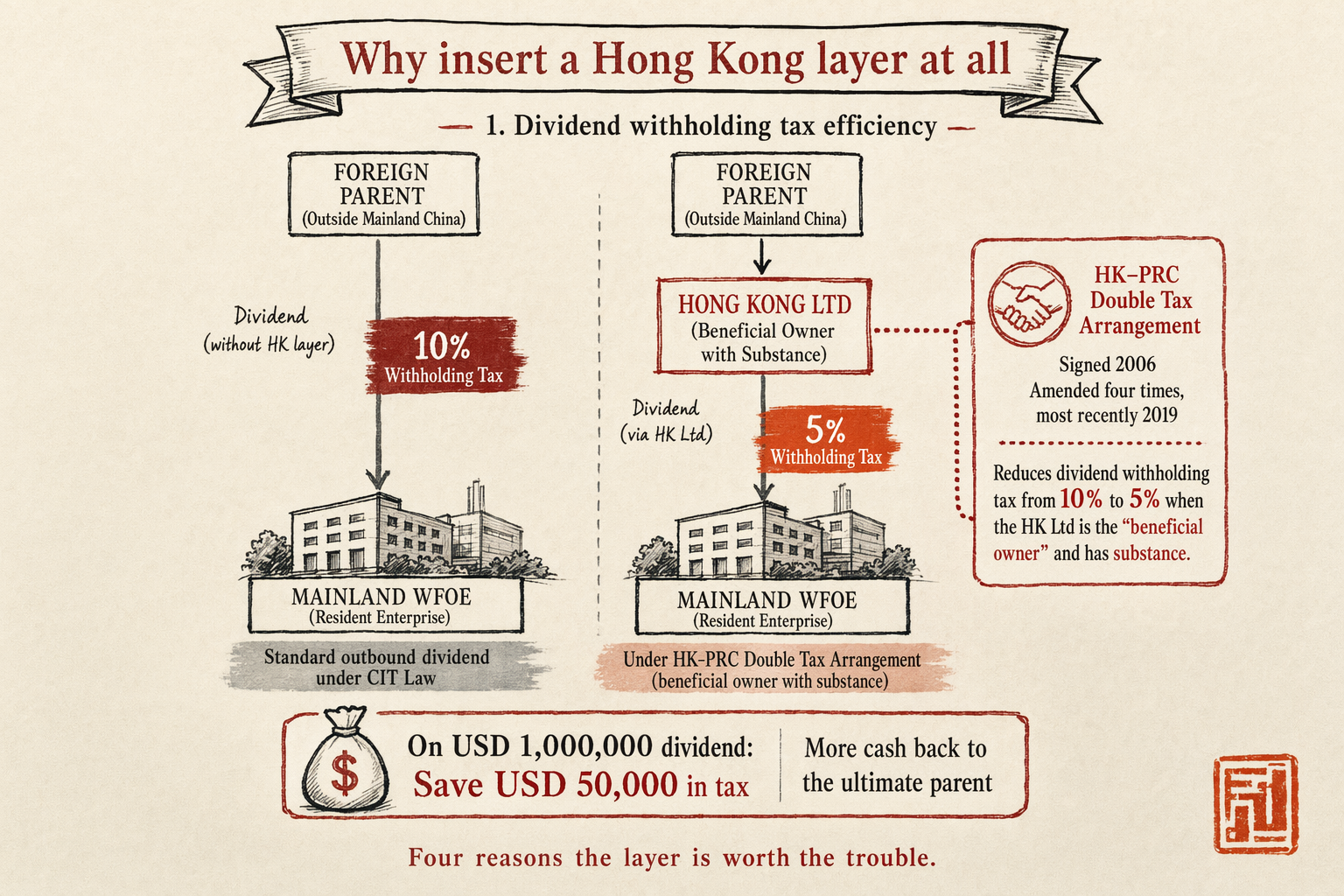

Why insert a Hong Kong layer at all

Four reasons the layer is worth the trouble:

- Dividend withholding tax efficiency. Standard outbound dividend withholding from mainland WFOE to foreign parent is 10% under the CIT Law. The HK-PRC double tax arrangement (signed 2006, amended four times, most recently 2019) reduces this to 5% if the HK Ltd is a "beneficial owner" with substance. On USD 1M of repatriated profit per year, that is USD 50,000 saved annually — material over a five-year horizon.

- IP separation and licensing. Hold core IP at HK Ltd level, license it into the mainland WFOE under arm's-length royalty rates. Royalty payments are deductible at the WFOE (reducing CIT base) and taxed at 10% withholding on the way out — or 7% under the HK treaty. Net effect: efficient ongoing capital stripping of WFOE retained earnings into the offshore IP holder.

- M&A and divestment optionality. Selling the HK Ltd rather than the WFOE itself avoids the PRC capital gains tax that applies to direct foreign-shareholder transfers of mainland-resident company shares (10% withholding under SAT Circular 7). HK Ltd share transfers are taxed in HK at 0% on capital gains — significant on exit.

- FX flexibility for capital injection. HK Ltd holds HKD, USD, RMB, EUR in parallel without the mainland's SAFE controls. Funding the WFOE through the HK Ltd, the parent funds the HK Ltd first in whatever currency, then the HK Ltd wires RMB-equivalent capital to the WFOE under a SAFE FDI registration. The currency conversion happens in HK, not mainland.

HK Ltd registration timeline and cost

The HK side. Hong Kong Companies Registry processes registrations in 3-5 business days for clean filings. Working timeline:

- Days 1-3: company-name search and approval, director and shareholder KYC, drafting Articles of Association, secretary appointment (legally required for HK Ltd).

- Days 3-7: filing with Companies Registry, receipt of Certificate of Incorporation and Business Registration Certificate.

- Weeks 2-4: HK bank account opening (separate process, materially slower in 2026 — see banking section).

- Weeks 3-8: SAFE Foreign Direct Investment registration on the mainland side, naming HK Ltd as the offshore shareholder of the WFOE.

- Weeks 6-12: capital injection from HK Ltd to mainland WFOE through SAFE-registered cross-border wire.

Cost in 2026, all-in including HK secretarial setup and first-year compliance:

- HK Ltd setup: HKD 8,000-18,000 (~USD 1,000-2,300) including registration fees, secretary appointment, registered office, and standard Articles.

- Annual maintenance: HKD 15,000-35,000/yr including secretary, registered office, profits tax filing, annual return filing, and minimal audit.

- HK profits tax filing: HK tax rate is 8.25% on first HKD 2M profits, 16.5% above. If HK Ltd only holds shares and receives dividends, the filing is mostly nil-return.

The HK Ltd is meaningfully cheaper to maintain than the WFOE — there is no equivalent of mainland's deemed-profit tax, the audit requirements are simpler, and the banking, while harder to open, is operationally lighter.

Substance requirements for treaty benefits

This is the part most foreign founders underestimate. SAT Bulletin [2018] No. 9 sets out the criteria mainland tax authorities apply when deciding whether an HK Ltd qualifies as the "beneficial owner" for treaty benefit purposes. The 2022 enforcement wave under the GAAR (General Anti-Avoidance Rule) tightened the test materially.

What the mainland tax authority looks for:

- Real HK office. Not a registered-agent address. A leased space (shared workspace acceptable), real business activity happening there. Photographic evidence and lease documentation requested in disputed cases.

- Real HK directors. At least one HK-resident director who actually makes board-level decisions. Pure nominee directors with no decision authority do not satisfy the test.

- Real HK staff. At least one or two HK-employed staff with documented payroll, social insurance under HK MPF (Mandatory Provident Fund), and substantive job descriptions. Holding-company-only structures can satisfy with minimal staff if the holding activity itself is the substance.

- Real HK business activity. Board meetings minuted in HK, financial decisions documented in HK, contracts executed by HK directors. A board that meets only via signature-by-circulation and never sits in HK signals lack of substance.

- Tax residency certificate. Annual Hong Kong Tax Residency Certificate issued by HK Inland Revenue Department on request. Required to claim treaty benefits at the mainland withholding step.

Operational reality: a HK Ltd that holds one mainland WFOE plus minor offshore IP, with one HK-resident director, one part-time HK-based admin staff, leased shared workspace with documentation, quarterly board meetings in HK, satisfies the test. Cost of that substance: USD 25,000-45,000/yr above bare-minimum maintenance. Below that level of substance, the 5% treaty rate is at risk.

Banking the HK Ltd in 2026

HK banking became materially harder in the 2018-2022 KYC tightening cycle. Where a 2015 founder could open HSBC HK in a week, the 2026 founder budgets 8-16 weeks for a traditional-bank account and considers virtual-bank alternatives in parallel.

Traditional banks (HSBC HK, Standard Chartered HK, Hang Seng, DBS HK, BoC HK): in-person account opening, full business plan, proof of operations, source-of-funds documentation traced back through the parent's history, director and shareholder KYC including residence and tax residency. 8-16 weeks if accepted; 30-40% rejection rate for cross-border-controlled shell-like structures even when properly substantive.

Virtual banks (ZA Bank, WeLab Bank, Ant Bank HK, Mox, livi): fully digital onboarding, 1-3 weeks, lower KYC bar but capped transaction sizes (HKD 5-50M depending on bank and tier), no physical chequebook, no SWIFT for some banks. Sufficient for an HK Ltd that primarily receives and distributes dividends; insufficient for an active operating HK Ltd.

Dual-track is the working pattern: open the virtual bank first for immediate operating use, while running the traditional-bank application in parallel for higher-limit and SWIFT capability. By month four most foreign founders have both.

The HK Ltd's bank then connects to the mainland WFOE's bank via a SAFE-registered cross-border arrangement. Capital injections wire HKD or USD from HK Ltd to WFOE; dividends wire RMB-converted from WFOE to HK Ltd; royalty payments similarly. Each cross-border wire is a SAFE filing.

When the layer becomes overhead

Run the math. The HK Ltd full operating cost — substance, banking, secretarial, audit, compliance — lands around USD 35,000-55,000/yr in 2026. Against that, the 5% dividend withholding saving versus the 10% non-treaty rate is 5% of repatriated profit.

Break-even on the dividend saving alone: USD 35-55k in annual savings requires USD 700k-1.1M of repatriated dividends per year, which implies roughly USD 2-3M of post-tax mainland WFOE profit. Below that, the dividend saving is smaller than the overhead.

Including the IP-licensing benefits and the M&A optionality, the break-even moves down toward USD 1-1.5M/yr of mainland operating profit. Below that, direct parent → WFOE structure is cleaner.

Three scenarios where the HK Ltd makes sense even below the dividend break-even:

- Existing HK operations. If the parent already operates in HK for other reasons (regional sales, holding HK staff, banking the regional region), adding the mainland WFOE under the existing HK entity is incremental.

- Planned M&A exit. If a strategic exit is plausible within 5 years, the HK Ltd structure protects against the SAT Circular 7 capital-gains exposure on direct WFOE share transfers.

- IP protection strategy. If core IP needs to sit offshore for IP-defense reasons (against mainland trademark squatting, against forced technology transfer concerns), the HK Ltd as IP holder provides the offshore home.

For the broader Hong Kong context see the Hong Kong as your mainland-China gateway topic hub. The WFOE vs Hong Kong limited comparison covers the structure-vs-structure analysis. The China company formation service hub shows quoted prices for the HK Ltd registration plus mainland WFOE bundle.

Frequently asked questions

Can I convert a direct foreign-parent → WFOE structure to a HK-intermediated structure later?

Yes, through a share transfer of the WFOE from the foreign parent to a newly-formed HK Ltd. The transfer triggers SAT Circular 7 capital gains tax on the transfer price unless an exemption applies. Plan the structure at formation; retrofitting is expensive.

Does the HK Ltd need its own audit?Yes, statutory audit is required for HK Ltd under the Companies Ordinance unless it qualifies for SME exemption (very small turnover and asset thresholds). Most holding companies do not qualify for SME exemption. Audit fees are modest — HKD 15,000-35,000/yr for a holding company.What if HK substance fails the mainland tax authority test?The mainland authority denies the 5% treaty rate and applies the 10% non-treaty rate. The disallowance is typically prospective; back-year disallowances are rare without clear evidence of treaty shopping. Cure: build substance and re-apply for the tax residency certificate in subsequent years.Is a Singapore or BVI structure better than HK?BVI has no treaty benefits with China and is increasingly flagged. Singapore has a treaty with similar terms to HK but is more remote operationally and slower to bank. HK remains the working choice for mainland-focused holding structures despite all the friction.

Is a Singapore or BVI structure better than HK?BVI has no treaty benefits with China and is increasingly flagged. Singapore has a treaty with similar terms to HK but is more remote operationally and slower to bank. HK remains the working choice for mainland-focused holding structures despite all the friction.

Next step

To run the HK Ltd vs direct-foreign-parent economics for your operating profit profile, use the China Expansion Budget Estimator — tab 4 includes the break-even calculator for the HK intermediate layer. Free XLSX.