The four structures most foreign founders actually choose between

There are technically seven or eight legal entity forms a foreign investor can use to operate in mainland China. Four of them are real options in practice. The other three (state-owned cooperative, contractual joint venture, foreign-invested partnership) are vestigial — they exist for specific situations that virtually no foreign founder ever encounters, and the partner firms that file them are specialists who would refer you back through us.

The four real options:

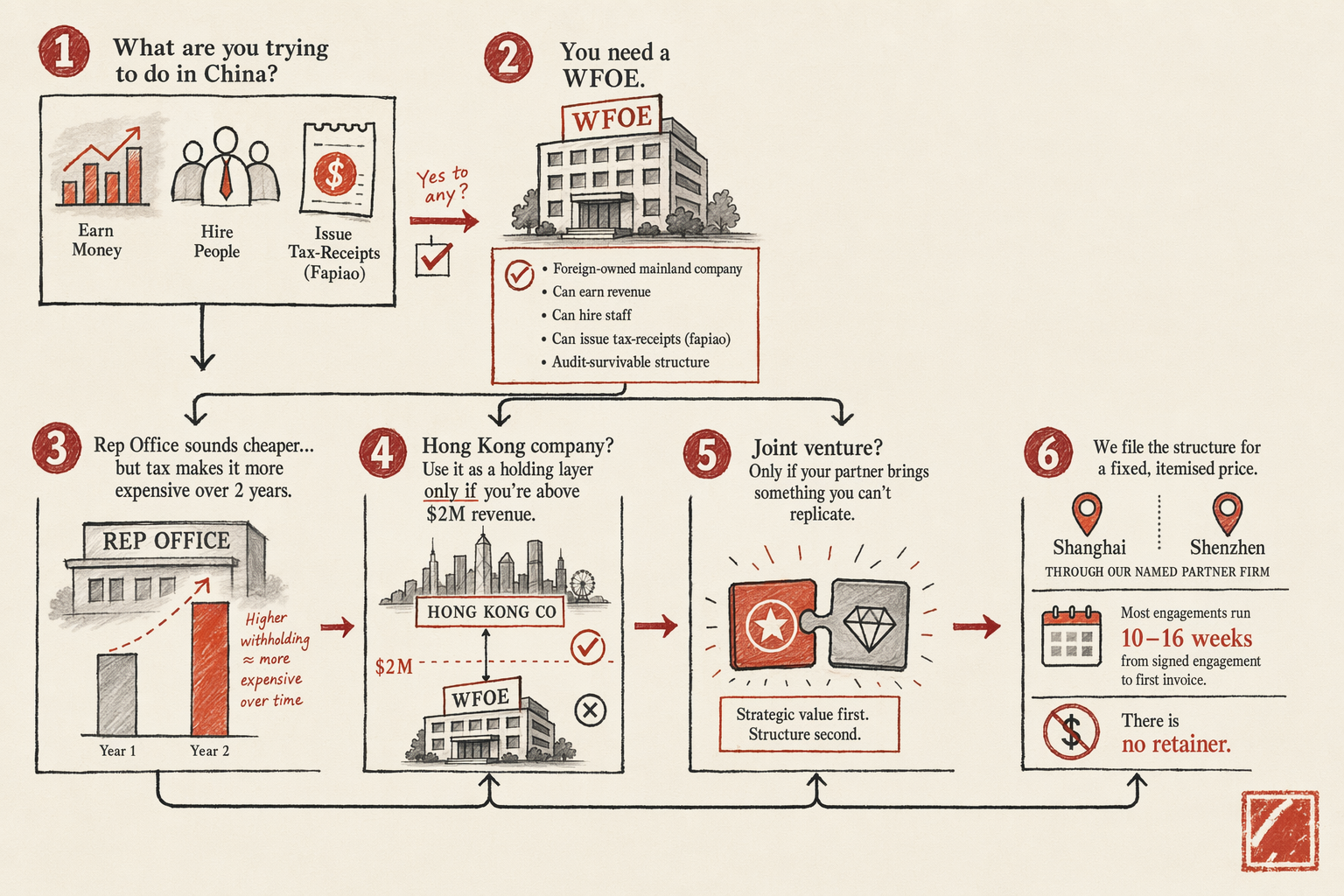

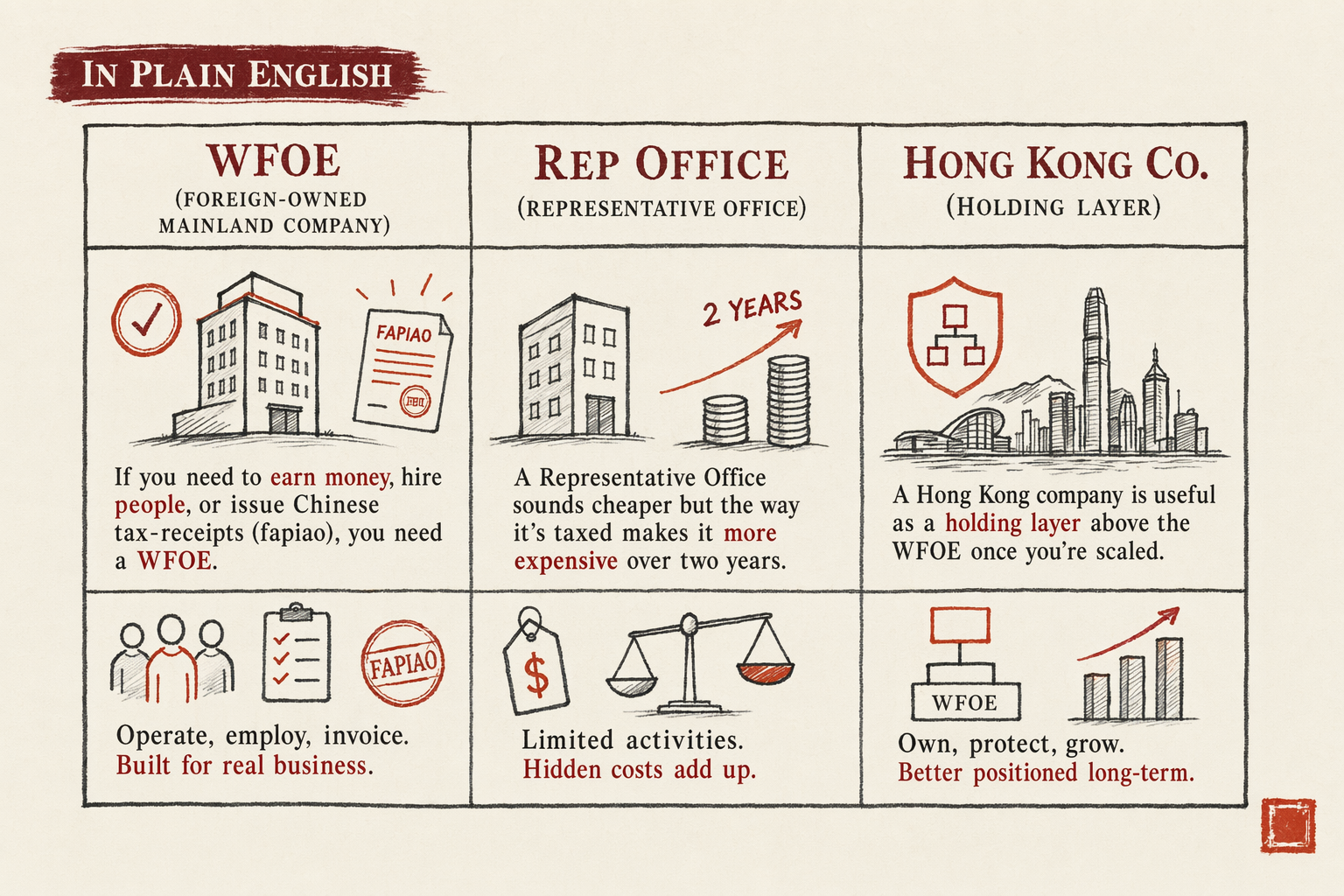

- WFOE (外商独资企业, Wholly Foreign-Owned Enterprise) — 100% foreign-owned mainland limited liability company. Can earn revenue, hire staff, issue fapiao, hold an ICP filing, own a CNIPA trademark. The default for any operational presence in China above pure market research.

- Representative Office (代表处) — Mainland branch of an overseas parent. Cannot earn revenue, cannot sign sales contracts, cannot directly hire local staff except through approved labour dispatch. Taxed on a deemed-profit basis (a markup on expenses). Useful for narrow market-research engagements; mostly outclassed by the WFOE for anything operational.

- Hong Kong limited (HK Ltd) — Offshore-ish jurisdiction with its own legal system, English common law, separate tax regime (16.5% profits tax, no VAT, no withholding on dividends domestically). Cannot operate inside mainland directly, but can hold a mainland WFOE underneath, can invoice mainland customers cross-border, can pay foreign-currency salaries. Useful as a layer above WFOE or as a standalone for cross-border-only operations.

- Equity Joint Venture (EJV, 合资企业) — Mainland LLC with at least one Chinese shareholder. Required only in a shrinking number of industries (some media, some publishing, some categories of regulated services). For most categories now permitted to 100% foreign ownership, the JV is a structural choice, not a regulatory necessity. Picked when the Chinese partner brings something irreplaceable — a manufacturing line, a regulatory license, a distribution network.

Choice between the four runs along three axes. First, do you need to earn mainland revenue? If yes, RO is out; you need WFOE, JV, or cross-border via HK. Second, do you need to hire mainland staff directly? If yes, RO is also out; same shortlist. Third, do you need to issue fapiao to B2B Chinese customers? If yes, you need a mainland entity, which rules out standalone HK Ltd. The interactive Structure Decision Matrix runs the question set against your specifics.

WFOE (外商独资) — when it's mandatory, when it's overkill

The WFOE is the foreign founder's default. Where it is mandatory: any business that needs to invoice mainland customers in RMB, any business with mainland staff on Chinese payroll, any business holding a mainland ICP filing on its own entity, any business filing a CNIPA trademark under its own name in mainland (rather than via Madrid). Where it is overkill: cross-border-only operations that ship from a bonded zone (Xiaohongshu cross-border, Tmall Global), pure remote SaaS that has no mainland sales presence, founders who want a single-year market test before committing to operational scale.

Registered capital — the headline number on every WFOE filing — was nominally abolished as a hard minimum in 2014. In practice it is alive and well as a soft requirement. AIC will challenge you if stated capital looks out of proportion with operational scope. Indicative bands that pass review in 2026:

- Trading WFOE in Shanghai: stated capital

$50,000-150,000 USD. The cash does not have to wire on day one; multi-year capital-injection schedules are standard, and many WFOEs run on a 5-year schedule. - Consulting / SaaS / services WFOE: stated capital

$30,000-60,000 USD. Lower because services don't require the same working-capital optics. - Manufacturing WFOE: stated capital

$200,000-1,000,000+ USD. Much higher; depends on industry-specific minimums. - Food, cosmetics, pharma WFOE: stated capital is one of several factors; regulatory licensing dwarfs the capital question.

The stated capital is a real liability. Creditors can call on unpaid stated capital; tax bureaus can use the figure when assessing operating substance. Don't inflate it for marketing reasons. The capital injection schedule should match how fast you actually expect to fund the entity.

End-to-end registration timeline, signed engagement to AIC business license: 4-6 weeks in Shanghai and Shenzhen, 6-8 weeks in Beijing, 8-10 weeks in tier-2 cities. Post-license work — chops carved, tax registered, bank account opened, SAFE filing for cross-border capital, social-insurance enrollment, general-taxpayer status — adds another 4-8 weeks. Realistic total from signed engagement to first fapiao issued: 10-16 weeks. If anyone quotes you 'WFOE in 30 days' they are quoting business-license-only and you should ask what is left to do after that.

De-registration is the conversation no one wants to have at incorporation, but it matters: deregistering a WFOE that did not work out takes 8-14 months and costs more than registration, often $8,000-15,000 USD in fees plus the cost of running the entity in deregistration mode (compliance filings continue until the tax bureau signs off). Plan for it upfront. Do not over-capitalise. Pick a city where deregistration is reasonably clean (Shanghai and Shenzhen run efficient deregistration queues; tier-2 cities can drag for years).

Representative Office — the 20% expense-markup tax trap

The Representative Office is the tempting cheap option that almost always costs more in year two than the WFOE you should have set up to start with. The pitch is simple — registration is faster (3-5 weeks vs 4-10 for a WFOE), the document set is smaller, the registered capital question doesn't exist. The catch is the tax structure.

An RO cannot earn revenue. It exists to do market research and represent the foreign parent. Mainland tax authority therefore assesses corporate income tax on the RO using the deemed-profit method: a presumed profit is computed as a markup on the RO's operating expenses, and CIT (corporate income tax) is levied on that presumed profit. The markup rate is set by local tax bureaus; in 2026 it commonly runs 15-20%, occasionally higher in tier-1 cities.

The arithmetic that bites: an RO with $300,000 USD / RMB 2.15M in annual operating expenses (typical for two foreign reps and a local office assistant in Shanghai) is taxed as if it had earned $45,000-60,000 USD / RMB 320,000-430,000 in profit. CIT at 25% on that is roughly $11,250-15,000 USD / RMB 80,000-110,000 per year — owed regardless of whether the RO did anything that generated value. Add VAT (the RO is a deemed service provider for tax purposes on the same imputed base), and total annual mainland tax for that RO lands around $15,000-22,000 USD / RMB 110,000-160,000.

A small WFOE with the same operating footprint but actual revenue running through it is taxed on real margin, not imputed margin. If actual profit is zero (which it often is in year one), CIT is zero. If actual profit is positive, you pay on the actual number, not the made-up one. Over two years, a small WFOE almost always wins on tax. The RO is operationally cheaper to register and operationally more expensive to run.

When does an RO still make sense? Three cases. First, the foreign parent genuinely wants only market research with zero revenue intent — a window into the market before committing capital. Second, the business is in a category where WFOE formation is uncertain (some media-adjacent or content-adjacent categories) and a year of RO operation precedes the WFOE filing. Third, the foreign parent has internal accounting rules that make running a deemed-profit RO simpler than booking a WFOE on the consolidated balance sheet — a niche case, usually applies to PE portfolio companies or specific Japanese / Korean corporate-governance setups.

Conversion from RO to WFOE later is not in-place — it is RO deregistration plus fresh WFOE registration, with overlapping months where both entities exist for visa, payroll, and chop-custody continuity. Allow 4-6 months and budget $3,000-5,000 USD / RMB 21,500-35,800 on top of the WFOE setup cost. If you might want a WFOE inside 18 months, just start with the WFOE.

Hong Kong limited as an intermediate holding layer

The Hong Kong limited is the most over-recommended and over-debated structure in foreign-founder China advice. Some sales-gloss sites push it as a default; others write it off as a relic. Both are wrong. The HK Ltd is a structural tool with specific use cases and a real annual cost; it pays back at scale and is dead weight below scale.

The three cases where the HK intermediate genuinely pays back:

- IP held offshore and licensed into the WFOE. Software code, trademarks, patent portfolio held by the HK Ltd, licensed to the mainland WFOE on arms-length royalty terms. Royalty payments flow from WFOE to HK at 10% withholding tax, or 7% in some treaty positions. The licence fee is deductible against WFOE CIT, so on net you reduce mainland tax exposure and concentrate IP in a jurisdiction with weaker subpoena exposure to mainland courts.

- Dividend repatriation efficiency. Standard mainland outbound dividend withholding tax is 10%. The China-Hong Kong tax arrangement reduces it to 5%, conditional on the HK Ltd meeting substance requirements (real HK directors, real HK office, decisions documented as taken in HK). Without substance, the tax authority denies treaty benefits and you pay the full 10%. The substance requirement has tightened materially since 2020; a brass-plate HK Ltd no longer passes.

- Cross-border invoicing and HKD-RMB FX flexibility. HK Ltd invoices mainland customers cross-border on cross-border service contracts. Inflows land in HKD or USD in the HK bank account; capital injections downstream into the WFOE flow back in RMB after SAFE registration. Used correctly, this is a clean way to fund a WFOE's working capital from foreign-currency revenue. Used incorrectly, it triggers transfer-pricing audit risk and SAFE rejections.

The three cases where the HK Ltd is dead weight:

- Founder ARR under roughly

$2 million USD / RMB 14.3Mper year — the annual cost of running the HK Ltd (audit, accounting, designated representative, registered office) at$2,800-5,200 USD / RMB 20,000-37,200often exceeds the tax benefit. - No IP to separate (pure trading business with no trademarks worth licensing).

- Founder has not yet built any operating substance on the HK side and is unwilling to fly to HK to attend board meetings, sign documents, and document decisions on HK letterhead.

HK incorporation itself is straightforward — Companies Registry filing, BR certificate, NNC1 form, all done online. Indicative cost $1,400-2,200 USD / RMB 10,000-15,700 including year-one designated representative and registered office. The work isn't the incorporation; it's the ongoing substance requirement and the cross-border accounting discipline.

Banking on the HK side has gotten harder. HSBC, Standard Chartered, and Hang Seng now require in-person account opening, a business plan, and proof of operations. Approval is uncertain and timelines run 8-16 weeks even for clean applications. Virtual banks (ZA Bank, WeLab, Mox) are easier to open but limited in cross-border transfer scale, which limits their usefulness for funding a WFOE.

Equity Joint Venture — when the JV partner is non-negotiable

The Equity Joint Venture (EJV) is the structure foreign founders pick when they have no choice. Almost every category that historically required a JV has been opened to 100% foreign ownership over the past decade. The categories that still mandate Chinese participation are narrow: some types of media and publishing, certain regulated services (some financial services categories, some healthcare), some categories of telecom services. Outside those categories, a JV is a strategic choice rather than a regulatory one.

The two strategic cases where a JV is worth the cost:

- The Chinese partner brings something operationally irreplaceable. A manufacturing line you cannot replicate, a regulatory license you cannot get on your own, a distribution network into channels you cannot access, or government relationships that materially change what is permitted. The test: would you struggle to operate at all without them in the first 18 months? If yes, JV. If no, WFOE.

- You explicitly want operational risk shared. A 51-49 or 60-40 JV puts the Chinese partner on the hook for the half of operations they know better, with both sides exposed to upside and downside. Rare for foreign founders to pick this voluntarily, but it does exist in JV structures where the foreign side has capital and the Chinese side has market access.

The cost of a JV vs a WFOE is not registration cost (similar) — it is governance cost. JVs require a board of directors with both sides represented, a JV agreement covering deadlocks, dispute resolution, transfer restrictions, exit terms, profit-sharing mechanics, and IP allocation. The JV agreement is the most-important document; we strongly recommend not skimping on the lawyer, and we route JV engagements through partner firms with specific JV-arbitration experience.

Profit-sharing in a JV defaults to equity proportion. Asymmetric profit-sharing (e.g. 60-40 equity, 50-50 profit) is permitted but adds tax complexity. Dividend distribution is subject to the JV board agreeing on it, which is the most-common deadlock point in second-year JVs.

Exit mechanics matter most. The standard JV agreement should include a right-of-first-refusal on share transfers, a tag-along and drag-along on third-party offers, a buy-sell mechanism (Texas shoot-out or Russian roulette) for deadlocks, and a clear path for the foreign partner to exit to either the Chinese partner or a third party. Without these, year-five deadlocks turn into multi-year litigation in mainland courts, which is a structurally bad position for the foreign party.

Business scope (经营范围) drafting and AIC pre-clearance

The single most-consequential piece of paperwork in your formation is the *经营范围* (business scope). This is the explicit list of activities the entity is authorised to conduct, recorded on the business license itself, and enforced by AIC, the tax bureau, and every platform that runs a verification against it. Get it wrong on day one and you spend the next 12-18 months filing amendments and getting rejected from platforms.

Three things make business-scope drafting hard. First, the catalogue is in Chinese; the English translations are advisory, and the legally-effective version is the Chinese phrase. Second, the catalogue is hierarchical — narrow phrases authorise narrow activities, broad phrases trigger broader regulatory review. Third, certain phrases auto-trigger regulated-category review (anything with 'medical', anything with 'finance', anything with 'food', anything with 'education') and bounce your filing into a queue that takes 8-16 weeks instead of 2-3.

The common drafting errors we see:

- Scope is too narrow. Filed for 'cosmetic product wholesale' only; six months later wants to add cosmetic e-commerce direct-to-consumer; amendment is a 4-6 week filing.

- Scope is too broad. Filed for 'wholesale and retail of various products including but not limited to' — AIC bounces; the catalogue does not accept open-ended scopes.

- Scope triggers a regulated category by accident. Filed for 'consulting services' which is fine; added 'health consulting' which is a TCM-adjacent regulated category that requires an extra license.

- Scope conflicts with the WFOE's stated capital. Filed for trading scope with $20k stated capital; AIC asks why capital is below the soft-floor for trading.

- Scope language is not on the standard catalogue list. Made-up phrases are bounced; the catalogue is closed-vocabulary.

Our standard pre-clearance pass: draft three candidate scope statements covering everything the entity might do in 24 months, run each through an informal AIC pre-clearance with our partner firm in the target city, pick the cleanest version. The pre-clearance costs nothing extra; the partner has the relationship to ask. Skipping this and filing speculatively is the most common reason WFOE filings come back for rewrite.

Once filed, amending the scope is a separate AIC filing — typically 2-4 weeks in Shanghai/Shenzhen, 4-6 weeks elsewhere. Plan for at least one scope amendment in years 2-3 as the business evolves.

Why formation filings get bounced

Bounces during WFOE / RO / JV formation cluster around documentary problems on the foreign side and substance problems on the AIC side. Most-common, ordered by frequency:

- Apostille on the wrong document, or by the wrong authority. The apostille has to be on the certificate of incorporation of the parent, issued by the competent authority of the country of incorporation, with the certificate dated within 6 months. We have seen apostilles on the wrong document, apostilles from a notary in a third country (invalid), and apostilles that have expired by the time the filing lands in queue.

- Board resolution does not authorise the specific actions. Generic 'authorisation to do business in China' is not enough. The resolution must name the entity to be formed, the city, the legal rep, the stated capital, and the business scope at the level of specificity that AIC requires.

- Stated capital does not match operational scope. $20k stated capital on a trading WFOE will trigger questions. $5M stated capital on a 2-person consulting WFOE will trigger different questions. Aim for the middle of the band for your category.

- Legal rep passport is in the wrong scan format or expires too soon. Filing systems want 12+ months remaining validity.

- Registered address lease is not from an AIC-approved address. A residential address fails. A shared-office without a real lease fails. The lease must be in the name of the entity-to-be (or the parent with an undertaking to assign), have at least 12 months remaining term, and come from a building on AIC's approved-clusters list.

- Business scope language is not from the standard catalogue. Discussed above.

- The foreign parent is itself opaque. An ultimate-beneficial-owner that traces back through three offshore jurisdictions can trigger an enhanced due diligence pass that takes 8-12 weeks.

The fix is documentary discipline before submission. Our partner firms run a full pre-clearance pass, flag the issues, and resolve them before the filing hits queue. The cost is a week of pre-submission work; the benefit is not losing 6 weeks to a resubmission.

Who actually forms your entity

Mike brokers; named partner firms in Shanghai, Shenzhen, or Beijing handle the AIC filings. Partner-firm assignment depends on the entity type and the city — Shanghai-based partners for Shanghai WFOEs and Shanghai FTZ filings, Shenzhen partners for Qianhai filings, Beijing partners for Beijing-specific industries. Each partner has at least seven years of foreign-investor formation filings on record with the relevant AIC office; several have direct relationships at the regional MOFCOM and tax bureau desks.

JV filings route through a smaller subset of partners with specific JV-arbitration experience, because the JV agreement matters more than the AIC mechanics. HK Ltd filings route through a Hong Kong-licensed corporate services firm; the mainland partners do not file HK directly.

Partner names appear on the engagement letter, on every document the partner sends, and on the AIC certificate. Partner-firm fees are itemised separately from Mike's brokerage on the engagement letter; there is no margin built into the partner line. If a partner is unresponsive mid-engagement, Mike re-routes to a backup in the same city at no extra fee, and the original is removed from the directory. This has happened twice in three years.

In plain English

If you only read one paragraph: If you need to earn money in China, hire people, or issue Chinese tax-receipts (fapiao), you need a WFOE — a foreign-owned mainland company. A Representative Office sounds cheaper but the way it's taxed makes it more expensive over two years. A Hong Kong company is useful as a holding layer above the WFOE once you're above two million dollars in revenue, otherwise it's dead weight. A joint venture only makes sense if your Chinese partner brings something you genuinely can't replicate. We file the structure for an itemised price through a named partner firm in Shanghai or Shenzhen, and most engagements run ten to sixteen weeks from signed engagement to the first invoice you can issue. There is no retainer.

How an engagement actually runs

- 01

Structure scoping call (free, 60 min)

Walk through the four options against your revenue model, headcount plan, IP location, and exit horizon. We will tell you if you don't need a WFOE.

Within one Asia-Pacific business day

- 02

Name pre-clearance + 经营范围 drafting

Three candidate Chinese names submitted to AIC for clearance; final business scope drafted to cover everything you might do in the first 24 months without triggering a regulated-category review.

Inside the first three weeks

- 03

Document set + apostille

Certificate of incorporation of foreign parent, board resolution authorising the formation, passport of legal rep, lease for registered address. Apostille handled by your home country; partner firm receives translated set.

Two to four weeks (apostille is usually the bottleneck)

- 04

AIC filing + business license

Partner firm files with the local AIC. Shanghai and Shenzhen typically issue the business license in 12-18 business days; Beijing in 20-30; tier-2 cities in 25-40.

Three to eight weeks

- 05

Chops, tax, bank, SAFE, social insurance

Five sequential post-license filings. Chops carved (5 pieces), tax registration, RMB bank account, SAFE registration for cross-border capital, social-insurance enrollment for future hires.

Four to eight weeks post-license

- 06

General-taxpayer status

Required to issue fapiao to B2B customers. Filing runs 2-3 weeks after tax registration; some cities require evidence of operating substance first.

Two to three weeks post-tax

- 07

Year-one compliance handover

Bookkeeper introduced, monthly filing calendar shared, annual audit scheduled. You can keep our partner for compliance work or move to your own; we don't lock you in.

On general-taxpayer issuance