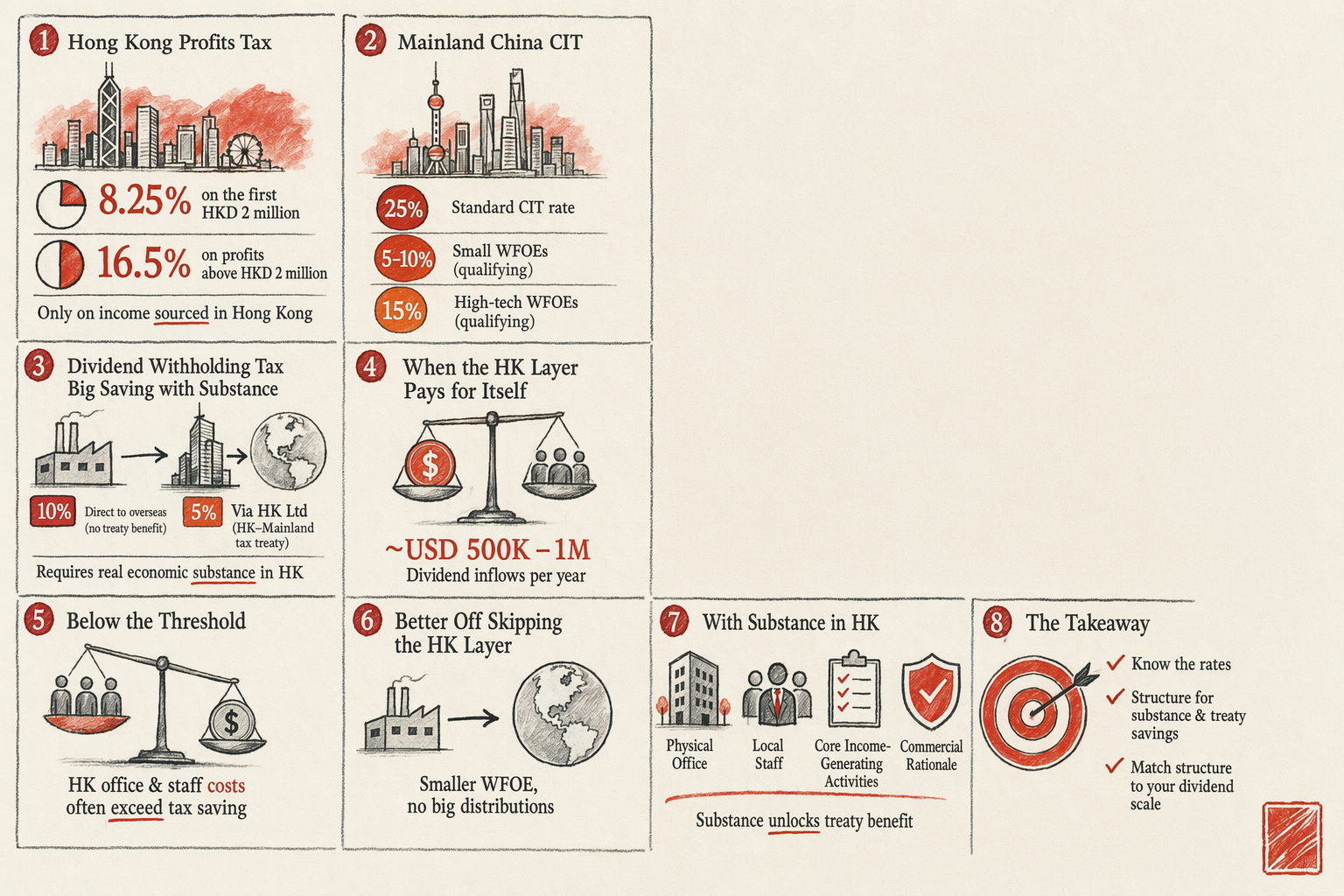

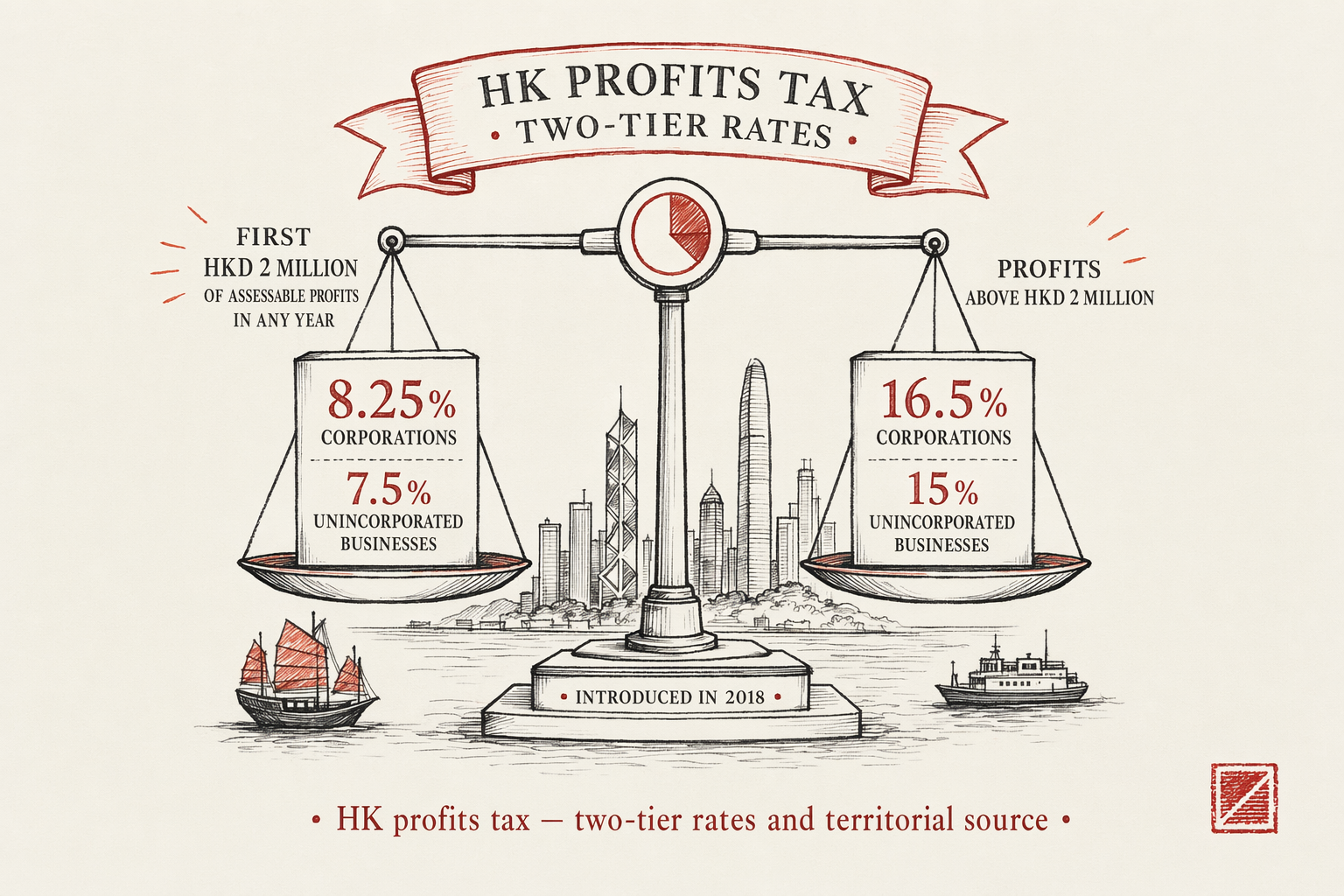

HK profits tax — two-tier rates and territorial source

Hong Kong profits tax operates under two principles that distinguish it from most major jurisdictions. The first is the two-tier rate structure introduced in 2018: the first HKD 2 million of assessable profits in any year is taxed at 8.25% for corporations (7.5% for unincorporated businesses), and profits above HKD 2 million are taxed at 16.5% (15% for unincorporated). The two-tier structure applies to each connected entity group at the group level, not per-entity, so a foreign founder cannot stack multiple HK Ltds and claim the 8.25% rate on each separately.

The second is the territorial-source principle. HK profits tax applies only to profits arising in or derived from Hong Kong. Income that is sourced outside Hong Kong is not subject to HK profits tax, even when received by an HK-registered entity. The source test is fact-based and looks at where the profit-generating activities actually occur — where contracts are negotiated, where decisions are made, where services are delivered, where the income-producing operations happen.

The Inland Revenue Department's Departmental Interpretation and Practice Note No. 21 (DIPN 21) sets out the source-test framework in detail. The test is not formal but operational. An HK Ltd that signs contracts in Hong Kong, makes its key business decisions through HK-resident directors meeting in Hong Kong, delivers services from an HK office with HK-resident staff, and books revenue against HK-counterparty contracts can credibly claim HK-sourced income. The same HK Ltd that is incorporated in Hong Kong but operates entirely from a mainland office with mainland-resident staff and mainland-counterparty contracts cannot claim HK-sourced income; its profits are sourced where the operations are.

The 2022 amendments to HK's tax regime tightened the source test for offshore passive income (interest, dividends, royalties, gains on disposal of equity interests). These four categories of offshore passive income are now subject to additional economic-substance tests under the Foreign-Sourced Income Exemption (FSIE) regime. For active business income (trading, services, manufacturing) the long-standing source test still applies; the FSIE rules layer on top for passive income only.

Mainland CIT — 25% default and preferential brackets

Mainland corporate income tax is governed by the Enterprise Income Tax Law (2007, amended 2017) and runs at a 25% default rate on the worldwide income of resident enterprises and on China-sourced income of non-resident enterprises. A mainland WFOE is a resident enterprise; its worldwide income is in scope, though foreign-sourced income is typically protected by treaty.

Three preferential brackets matter for foreign-founder WFOEs:

- Small low-profit enterprise. The most common preferential bracket. A WFOE with annual taxable profit under RMB 3 million, fewer than 300 employees, and total assets under RMB 50 million qualifies as a small low-profit enterprise. For 2025 forward, the effective rate on this bracket runs at 5% on the first RMB 1 million of profit and 10% on the RMB 1-3 million tranche. Most early-stage foreign WFOEs sit comfortably inside this bracket for the first 2-3 years of operation.

- High and new-technology enterprise (HNTE). A WFOE certified as an HNTE under the Ministry of Science and Technology framework qualifies for a reduced 15% CIT rate. The HNTE qualification requires substantial R&D spend (a defined percentage of revenue), Chinese-invented IP, and a documentary track record of R&D activity. The certification is a multi-quarter project but the 15% rate is attractive once it lands.

- Encouraged industries and special zones. Specific industries on the State Council's encouraged-investment catalogue, and WFOEs domiciled in certain special zones (Hainan Free Trade Port, Qianhai, Hengqin), qualify for 15% CIT or even lower rates under sector-and-zone-specific schemes. The eligibility criteria are sector-narrow and zone-narrow; most foreign-founder WFOEs do not qualify out of the box.

Above the preferential brackets, the 25% default applies. A mid-stage WFOE with annual taxable profit of RMB 5-20 million typically pays 25% straight; an early-stage WFOE in the small low-profit bracket effectively pays 5-10%; a certified HNTE pays 15%.

Where profits get taxed — the substance question

For a structure with an HK Ltd above a mainland WFOE, the operational question is where each tranche of profit gets booked and taxed. The structural answer is that profit attribution follows substance. The HK Ltd cannot simply book all profit at the HK level by issuing a low-margin service contract to the mainland WFOE — both jurisdictions' transfer-pricing regimes (and the OECD-aligned BEPS framework) require that intercompany pricing reflects arm's-length terms and that profit ends up where the value-generating activity actually happens.

A worked example. A foreign brand sells USD 5 million of products to mainland customers through a structure of (foreign parent) → (HK Ltd) → (mainland WFOE). The mainland WFOE handles customer-facing operations, fulfilment, customer service, and local marketing — say 60% of the value-generating activity. The HK Ltd handles international purchasing, IP licensing, regional management, and treasury — say 30% of the value-generating activity. The foreign parent handles brand stewardship, product development, and global strategy — say 10% of the value-generating activity.

Under arm's-length transfer pricing, the gross margin earned across the structure gets allocated roughly in proportion. The mainland WFOE books ~60% of operating profit, pays CIT at 25% (or its preferential bracket), and remits the remainder upstream as dividends. The HK Ltd books ~30%, pays HK profits tax on the HK-sourced portion (only on income meeting the territorial-source test), and remits the remainder upstream. The foreign parent books ~10% and pays its home-country tax.

What does NOT work: shifting most or all of the operating margin to the HK Ltd via low-margin intercompany pricing on the mainland side. The mainland State Taxation Administration's transfer-pricing audits target exactly this pattern, and the audit-and-adjustment process is expensive in both fees and reputation. What does work: documented arm's-length pricing, defensible value-chain allocation, and matching substance to where profit lands.

Dividend repatriation and the 5% treaty rate

The headline tax-rate comparison is incomplete without the dividend-withholding layer. When the mainland WFOE remits profits upstream, those dividends are subject to mainland withholding tax at a default rate of 10%. Treaty rates can reduce this materially. The Hong Kong–mainland Double Tax Arrangement provides a 5% withholding rate on dividends paid by a mainland enterprise to a Hong Kong shareholder, provided the Hong Kong shareholder is the beneficial owner of the dividend and meets the substance tests defined in State Taxation Administration Bulletin 9 (2018).

The beneficial-owner test under Bulletin 9 examines whether the HK Ltd has substantive economic activity (or, in practice, performs substantive functions in the value chain). Pure-holding HK Ltds with no operational activity often fail the beneficial-owner test and lose the 5% treaty rate, defaulting back to 10%. HK Ltds with genuine operational substance — HK-resident directors, HK office, HK staff, HK-counterparty contracts, HK tax filings — usually pass.

The 5% rate is preferential but not nominal. On a USD 1 million dividend remittance from a mainland WFOE to its HK parent: at 5%, withholding is USD 50,000; at 10%, withholding is USD 100,000. The substance investment that earns the lower rate pays for itself once dividend flows reach scale.

For the actual remittance mechanics — SAFE-side registration, document review, tax clearance certificate — see SAFE registration for cross-border FX inflows.

A realistic two-jurisdiction tax model

Pulling the layers together, a representative tax model for a foreign-founder structure with HK Ltd above mainland WFOE, both operationally substantive, USD 5M annual revenue:

| Layer | Headline rate | Effective rate after substance and treaty |

|---|---|---|

| Mainland WFOE — small low-profit bracket (early stage) | 25% | 5-10% on first RMB 3M profit |

| Mainland WFOE — standard bracket (mid-stage) | 25% | 25%, or 15% if HNTE-certified |

| WFOE→HK Ltd dividend withholding | 10% default | 5% under HK-mainland DTA with substance |

| HK Ltd — HK-sourced income | 16.5% (8.25% on first HKD 2M) | 16.5% (or 8.25%) — territorial-source applies |

| HK Ltd — non-HK-sourced active business income | 0% | 0% — territorial-source exempts |

| HK Ltd→foreign parent dividend | 0% from HK | 0% from HK; home-country tax applies at parent |

The structural advantage of the HK layer comes from three places: the dividend-withholding reduction (10% → 5% saves 50% of the withholding line), the HK profits-tax territorial-source rule (income arising outside HK is not taxed in HK), and the zero-withholding remittance from HK to the foreign parent (HK does not levy outbound dividend withholding).

The structural disadvantage of the HK layer is the substance overhead. An HK office, HK-resident staff, HK tax filings, HK regulatory compliance — these are real costs that scale with how convincingly the structure has to defend its substance under audit. For a small early-stage WFOE that sits in the mainland small-low-profit bracket, the HK overhead can exceed the tax benefit. For a mid-stage WFOE producing meaningful dividend flows, the HK structure typically pays for itself once dividends reach roughly USD 500k-1M per year.

For the topic hub covering HK as gateway see Hong Kong as Your Mainland Gateway. For the parent service see Ongoing Compliance. For when the HK layer is the wrong call regardless of the tax math see when NOT to use Hong Kong.

In plain English

If you only read one paragraph: Hong Kong taxes profits at 8.25% on the first two million HKD and 16.5% above, but only on income actually sourced in Hong Kong; mainland China taxes profits at 25%, dropping to 5-10% for small WFOEs and 15% for high-tech ones. The big saving from running an HK layer above your mainland WFOE comes from the dividend withholding — 10% drops to 5% under the HK-mainland tax treaty if your HK Ltd has real substance. The structure pays for itself once dividend flows reach roughly half a million to one million USD per year. Below that, the cost of maintaining a real HK office and HK staff often exceeds the tax saving, so a smaller WFOE without big distributions is better off skipping the HK layer.

Related

7 min read

Hong Kong as Your Mainland-China Gateway

HK Ltd holding mainland WFOE, CEPA benefits, banking dual-track, tax treaty position, common pitfalls.

6 min read

How to Choose an ICP Sponsor for Your Domain

Picking an ICP sponsor — entity-tied filings, sponsor fee ranges, support quality, what happens when a sponsor disappears.