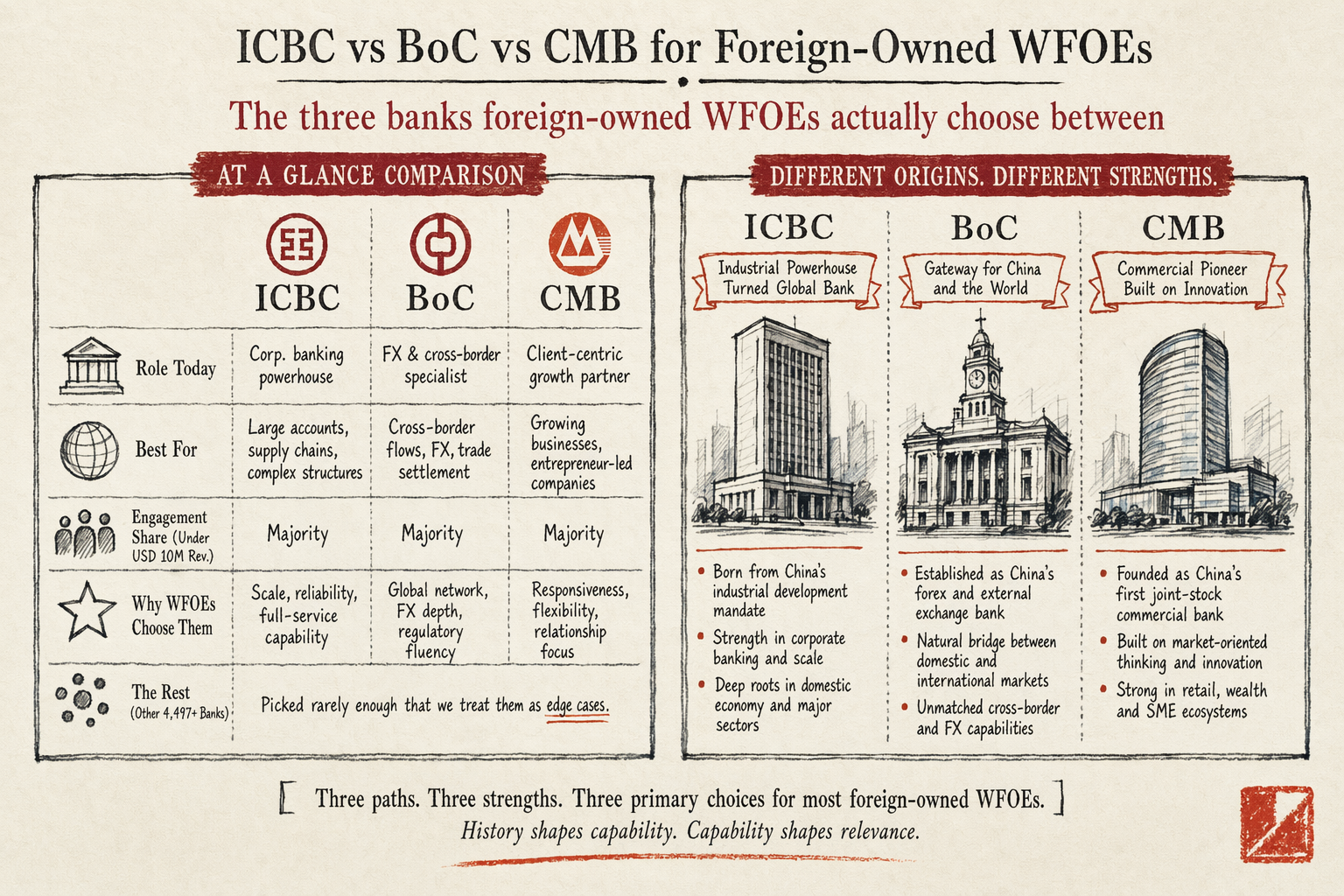

The three banks foreign-owned WFOEs actually choose between

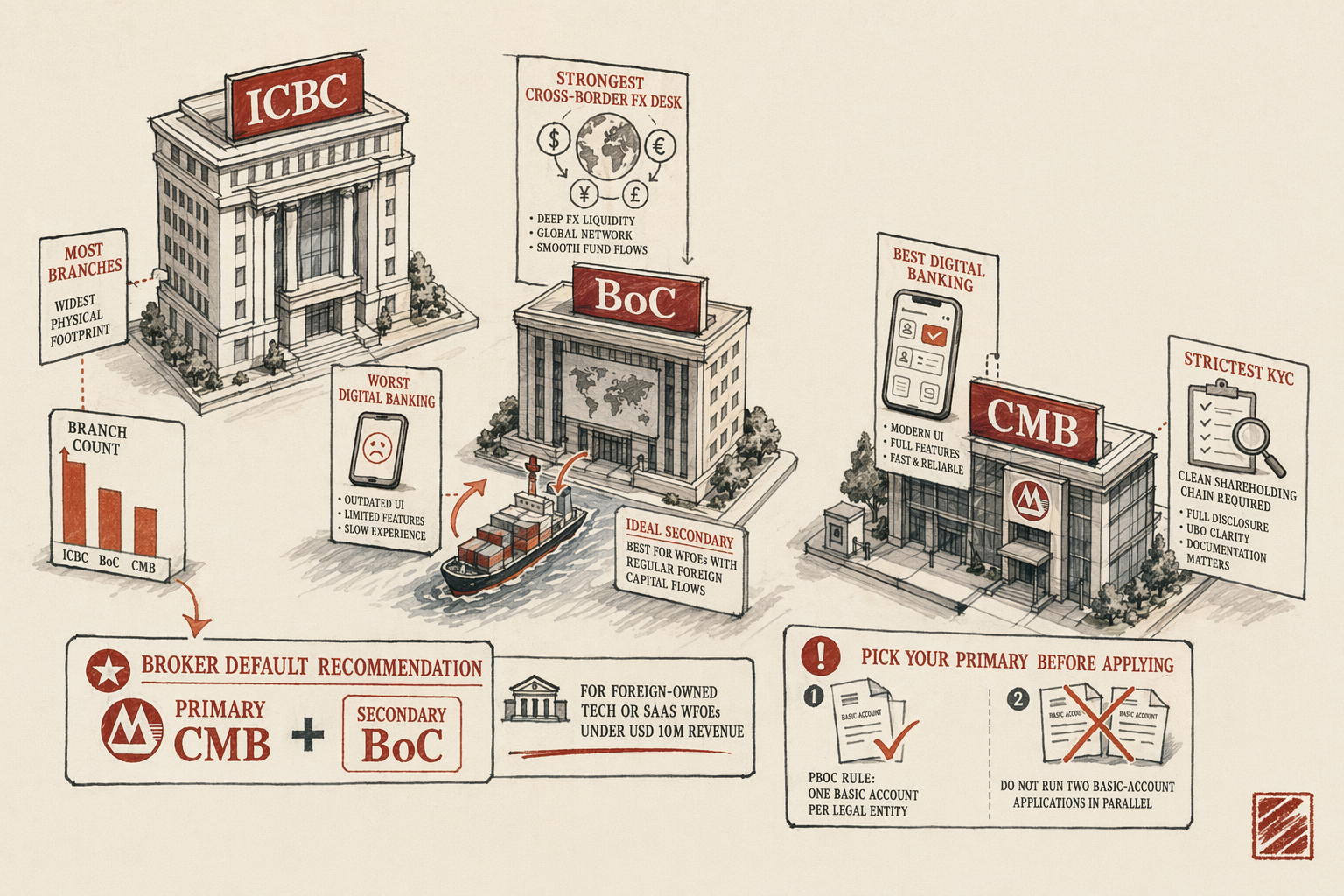

Mainland China has 4,500-plus licensed commercial banks. For a foreign-owned WFOE under USD 10 million annual revenue, three of them carry the majority of brokered engagements, and the rest get picked rarely enough that we treat them as edge cases.

The three primaries — ICBC, BoC, CMB — each emerged from a different historical role, and that history still shapes how they treat foreign capital today. ICBC was the corporate-banking giant under the old state-owned-bank structure, with the largest branch network and the deepest enterprise-customer base. BoC was the cross-border bank, originally tasked with handling China's foreign-exchange settlement, and it still has the most experienced FX desk for foreign capital. CMB came up in the joint-stock-bank wave of the 1990s as the digital-first challenger, and it owns the best mobile banking and the fastest decision turnaround.

The other large banks — China Construction Bank (CCB), Agricultural Bank of China (ABC), Bank of Communications (BoCom), and the joint-stock cluster of Ping An, CITIC, Minsheng, Shanghai Pudong Development Bank — all open foreign-WFOE accounts. They tend to come in via referrals (your accounting firm has a contact at a specific branch) rather than as primary recommendations. The brokered-engagement default stays with ICBC, BoC, or CMB unless there is a specific reason to deviate.

ICBC — largest network, slowest digital

ICBC's strengths line up with the WFOE that wants its primary RMB account at the bank with the most branch coverage and the strongest balance sheet. Every district in every Tier-1 and Tier-2 city has at least one ICBC branch, and ICBC's settlement infrastructure clears domestic transfers in under 30 minutes on average. Foreign-WFOE account opening typically runs 6-10 weeks for the basic account, which is the slow end of the range but acceptable given the network depth.

The trade-off is digital banking. ICBC's mobile and web banking surfaces work but feel ten years behind. Two-factor authentication relies on a hardware USB-key (UKey) for higher-value transactions; the desktop client requires Internet Explorer compatibility mode for several flows; foreign-language support is partial. Day-to-day operations through ICBC mean a finance person who can read Chinese banking UI and is comfortable with hardware key fobs.

ICBC's FX desk is competent for routine inbound capital and dividend repatriation but slower than BoC's on novel structures. Shareholder loans, intercompany royalties, and capital top-ups go through fine. Anything involving an unusual treaty position or a cross-border SPV often goes back to BoC at the routing stage.

Monthly account fees at ICBC: roughly RMB 30-80 for the basic account, similar for each general account, with separate FX-desk service fees levied per transaction. Total all-in for a typical foreign WFOE: RMB 150-400/month in account fees, before transaction-specific charges.

Bank of China — strongest for cross-border FX

BoC is the bank to pick when cross-border FX flows are a non-trivial part of your operating model. Their FX desk has the deepest historical experience with foreign-shareholder capital injections, dividend repatriation to a parent in any treaty jurisdiction, and the registration paperwork that SAFE (State Administration of Foreign Exchange) requires. If you are running an inbound USD or EUR capital flow above the SAFE document threshold (USD 50,000 equivalent per transaction), BoC is the operationally-fastest path.

Account-opening turnaround at BoC is comparable to ICBC for the basic account (6-10 weeks) and slightly faster on the FX-side capital account opening (3-6 weeks once the basic is live). The KYC review for foreign-owned WFOEs is more thorough than at ICBC — BoC asks more questions about the ultimate beneficial owner and the source of funds — but the questions are reasonable and the answers do not need to be unusual. A foreign WFOE with a clean offshore parent and a documented capital source passes BoC review without drama.

BoC's digital banking is mid-range. Better than ICBC, behind CMB. Their mobile app is functional in English and Chinese; their corporate web banking is workable; the UKey is still required for higher-value flows but the activation experience is cleaner. International wires through BoC settle inside 24-48 hours on average, which is faster than ICBC's 48-72 hour median for the same flow.

The case for BoC as primary: cross-border FX is part of your business model on day one. The case against: if you are a domestic-revenue-only WFOE that will not receive foreign capital after the initial injection, BoC's FX-desk advantage is less relevant and ICBC's network depth or CMB's digital UX might win on a different axis.

China Merchants Bank — best digital UX, strictest KYC

CMB is the bank we recommend most often to tech-sector foreign WFOEs with annual revenue under USD 10 million. The digital banking is genuinely good — fully bilingual, mobile-first, decent API access for accounting-system integrations, no hardware-key requirement for most flows under defined transaction caps. Account-opening turnaround on the basic account runs 4-7 weeks, which is the fastest of the three.

The trade-off is KYC strictness. CMB has the highest first-pass decline rate for foreign-owned WFOE applications among the three. Their compliance desk reads through the shareholding chain in more detail, asks more pointed questions about the source-of-funds proof, and is more willing to push back on documents that ICBC or BoC would accept on the first review. The decline rate is not random — it correlates with shareholding chains that pass through more than one offshore tier (foreign parent → BVI holdco → HK Ltd → mainland WFOE triggers more review than foreign parent → mainland WFOE directly) and with business-scope language that does not match what the AIC business license actually permits.

For a clean foreign-WFOE structure with one or two layers of offshore parent and a business scope that matches the operational plan, CMB clears review at roughly the same rate as ICBC and BoC. For a structure with three or more offshore tiers, or with a complex licensed-industry scope, CMB will probe harder and the application may go to manual review at the regional headquarters, which adds 2-4 weeks.

CMB's FX desk is the weakest of the three. Adequate for routine flows; not the first choice for shareholder loans, royalty repatriation, or any structure involving an unusual treaty position. A common pattern we recommend: CMB for the basic account and primary general account (best digital banking), BoC for a parallel general account that handles cross-border flows.

6-dimension comparison table

The decision-framework comparison, across the six dimensions that matter most for foreign-owned WFOEs:

| Dimension | ICBC (工商银行) | BoC (中国银行) | CMB (招商银行) |

|---|---|---|---|

| Basic-account opening time | 6-10 weeks | 6-10 weeks | 4-7 weeks |

| First-pass approval rate (clean docs) | ~80% | ~75% | ~65% |

| FX desk quality | Competent, slow | Strongest of the three | Adequate, narrow scope |

| Digital banking | Dated, UKey-heavy | Mid-range, bilingual | Best, mobile-first, API access |

| Monthly account fees (all-in) | RMB 150-400 | RMB 200-500 | RMB 120-350 |

| Branch network | Densest in every city | Strong in trade-hub cities | Strong in Tier-1; thinner in Tier-3 |

| English-language support | Partial, branch-dependent | Strong at FX desk + flagship branches | Strong across all channels |

Default broker recommendation for a foreign-owned tech-sector WFOE under USD 10M revenue: CMB primary, BoC secondary. The CMB primary gives you the best operational UX day-to-day; the BoC secondary covers the cross-border FX edge cases CMB is weaker on. ICBC enters the recommendation when network depth in Tier-2 and Tier-3 cities matters more than digital banking, which is mostly the case for manufacturing or distribution WFOEs.

Picking a primary and a backup before your first application

Two operational rules that surface from brokered engagements:

First, decide your primary and your backup before applying anywhere. Once a foreign-owned WFOE has been declined by one bank, the next bank's compliance desk treats the second application with more scepticism. The decline is not visible to the second bank directly through PBOC channels, but the cluster of questions a declined applicant carries forward — the resubmitted documents, the explanation letter, the slightly-off business-scope phrasing — flags the file as having been through one rejection cycle. Apply to your primary, fully prepared. If it declines, run a full diagnostic before resubmitting anywhere else.

Second, plan for a parallel application at the backup bank only after the primary is open. Sequential, not concurrent. A foreign WFOE with a basic account at one bank applying for a general account at a second bank is a normal pattern; both banks accept it as routine cross-bank diversification. A foreign WFOE applying to two banks simultaneously for the basic account flags as inconsistent intent and tends to draw extra scrutiny at both. The basic account is a once-only commitment under PBOC rules; pick one and live with the decision.

For the bank-by-bank document requirement matrix and the legal-rep travel packet for whichever bank you pick, see the RMB Banking Checklist. For the topic hub linking up to all RMB-banking articles see RMB Bank Account That Clears. For the parent service see Ongoing Compliance.

In plain English

If you only read one paragraph: ICBC has the most branches but the worst digital banking. BoC has the strongest cross-border FX desk and is the right primary if foreign capital flows in regularly. CMB has the best mobile and web banking but the strictest KYC, so a clean shareholding chain is required. For a foreign-owned tech or SaaS WFOE under USD 10M revenue, the default broker recommendation is CMB primary plus BoC secondary. Pick your primary before applying; do not run two basic-account applications in parallel because PBOC rules cap basic accounts at one.