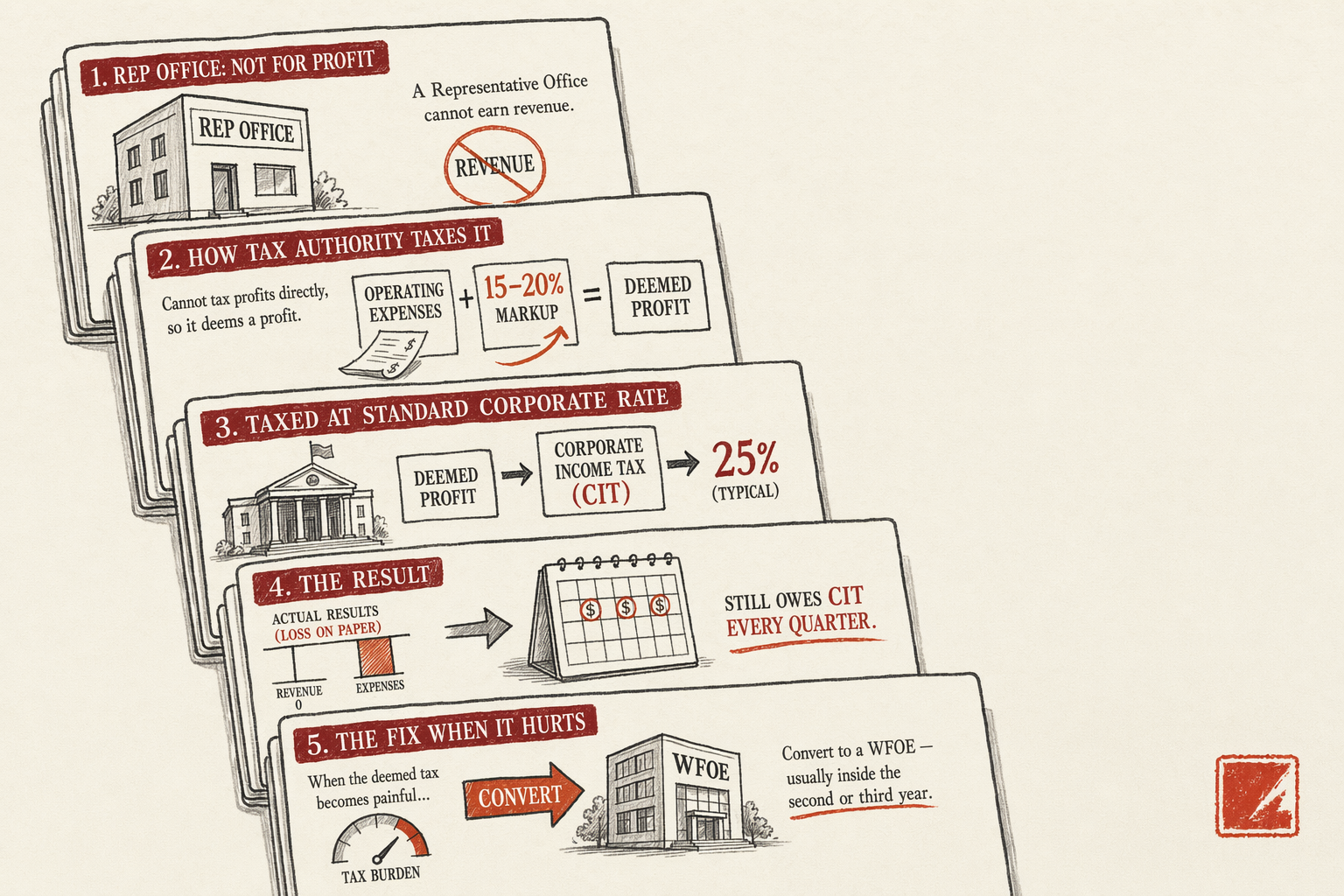

The Rep Office is the entry-level China structure most foreign brands considered first. Cheaper to register than a WFOE, faster to set up, only needs a chief representative — looks attractive on the comparison sheet. Then the first quarterly tax filing arrives and the founder learns about the deemed-profit method, which is the tax authority's answer to the question "how do we tax an entity that legally cannot earn revenue?"

This article walks through why the method exists, how it produces tax bills on a money-losing entity, what a realistic year-one tax bill looks like on a small Rep Office, when an RO still makes sense despite the markup, and the signals that you have outgrown the structure. Written for the founder running an existing RO or considering one, who needs to know what they are signing up for at month three.

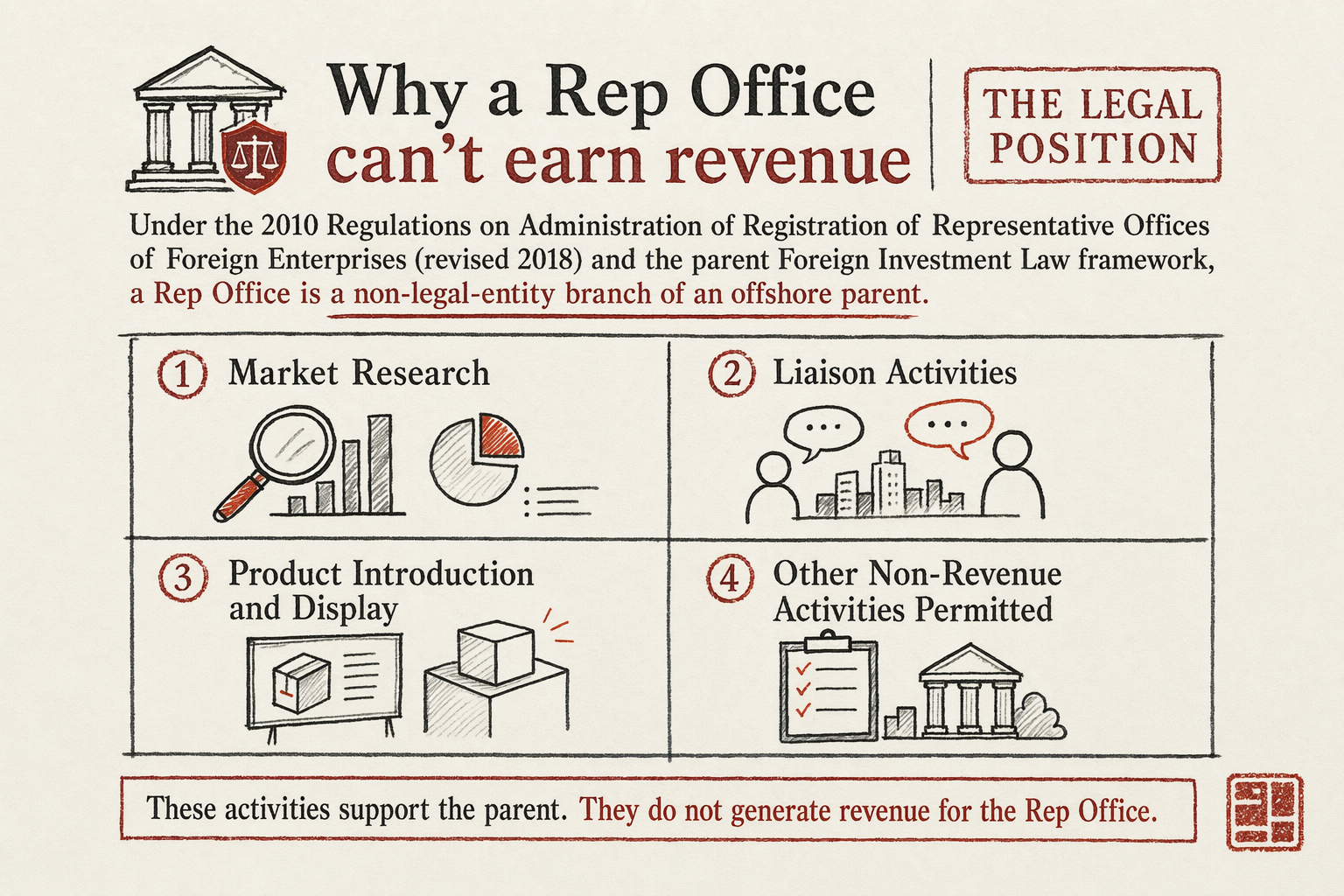

Why a Rep Office can't earn revenue

The legal position. Under the 2010 Regulations on Administration of Registration of Representative Offices of Foreign Enterprises (revised 2018) and the parent Foreign Investment Law framework, a Rep Office is a non-legal-entity branch of an offshore parent. It can conduct: market research, liaison activities, product introduction and display, and exchange of technical information. It cannot: sign customer contracts, issue invoices, take payments, hire mainland staff directly (it must hire through a labor dispatch agency), or hold inventory for sale.

Because the RO cannot sign customer contracts in its own name, it has no revenue line on its books. All revenue from China-sourced activity flows to the offshore parent. The Rep Office books only operating expenses — rent for the office, the chief rep's salary, dispatched staff salaries, office costs, business development costs, professional fees.

This creates a tax puzzle. The parent earns revenue from China-sourced activity but books it offshore where China cannot reach. The Rep Office spends money in China but has no revenue against which to compute profit. SAT (the State Administration of Taxation, now part of the State Taxation Administration) needed a method to attribute taxable profit to the in-country presence. The deemed-profit method is the answer.

How the deemed-profit tax is calculated

The mechanics live in Guoshuifa [2010] No. 18 — the SAT circular that defines the cost-plus computation for Rep Office taxation. The formula:

Step 1: Compute total operating expenses. Rent + chief rep salary + dispatched staff costs + office expenses + business development + professional fees. All expenses incurred by the RO across the quarter.

Step 2: Apply the deemed-profit margin. The default is 15% under Guoshuifa 18, but the local tax bureau has discretion to apply a higher rate (commonly 17.5% or 20%) depending on the RO's industry and reported activity. Most foreign brands in tier-1 cities encounter the 17.5-20% rate.

Step 3: Derive deemed revenue and deemed profit. Deemed revenue = Operating expenses / (1 − deemed-profit margin). Deemed profit = Deemed revenue × deemed-profit margin. With a 20% margin, deemed revenue = expenses / 0.80 = expenses × 1.25, and deemed profit = expenses × 1.25 × 0.20 = expenses × 0.25.

Step 4: Apply CIT and VAT. Deemed profit is taxed at the 25% CIT rate. The full deemed revenue is subject to 6% VAT (modern business services rate). Plus surtaxes (city construction tax, education surcharge) on the VAT, roughly 12% of the VAT line.

The effective tax burden on operating expenses, with a 20% deemed-profit margin, lands around 13-16% of operating spend, depending on surtax rates by city.

A real $300k/yr Rep Office tax bill

Working example. A market-research RO in Shanghai. Chief rep on USD 80k base. Two dispatched staff at USD 60k combined. Office in a mid-tier Pudong space at USD 45k/yr. Business development, travel, professional fees, miscellaneous: USD 35k. Office equipment depreciation: USD 5k. Total operating expenses: USD 225k. Plus chief rep housing allowance USD 30k and dispatched staff social contributions USD 25k. Grossed up: USD 280k/yr.

The Shanghai tax bureau applies a 20% deemed-profit margin to ROs in market-research scope.

- Deemed revenue: USD 280,000 / 0.80 = USD 350,000.

- Deemed profit: USD 350,000 × 0.20 = USD 70,000.

- CIT at 25%: USD 17,500.

- VAT at 6% on deemed revenue: USD 21,000.

- Surtaxes at ~12% of VAT: USD 2,520.

- Total annual tax bill: USD 41,020.

That is 14.6% of operating spend — on an entity with zero revenue on its own books and operating at a paper loss from the offshore parent's consolidated perspective. Compare against a WFOE at the same operating spend earning USD 600k of actual revenue, which would owe roughly USD 80k in CIT on real profit plus VAT netted against input VAT — the WFOE pays more in absolute dollars but generates revenue against which the tax is taken.

The brutal moment for a Rep Office is its first full year. Operating expenses are mostly fixed (rent + payroll), tax is computed mechanically, and the offshore parent's actual revenue from China activity is irrelevant to the local tax bill. A Rep Office that the parent has decided to wind down still owes deemed-profit tax until the deregistration completes — and Rep Office deregistration takes 4-6 months.

When an RO still beats a WFOE on cost

Three scenarios where the RO economics still work out, all of them narrow:

Scenario 1 — true 12-18 month market exploration. Operating expenses under USD 150k/yr, chief rep on rotation rather than full hire, no firm decision yet on whether to commit to mainland operations. RO total cost of ~USD 180-220k/yr including tax. WFOE setup cost (USD 8-15k) plus capital injection (USD 50k+) is wasted if the answer to the market question is "no." In this band the RO is cheaper than committing capital to a WFOE you may dissolve.

Scenario 2 — service-side intelligence gathering for an offshore contracting model. The offshore parent contracts with mainland customers directly, ships and invoices from offshore, and just needs in-country liaison and customer-success support. No fapiao requirement, no domestic Chinese B2B invoicing. RO scope fits and the tax bill is the cost of doing business.

Scenario 3 — pre-WFOE proving ground. The RO is explicitly the first phase of a planned 2-3 year transition into a WFOE. The chief rep becomes the WFOE's first GM. The RO's network and operating cadence become the WFOE's foundation. The RO tax bill across two years is the price of running the experiment before committing capital.

Outside these three, the WFOE is cheaper over a 24-month horizon. The decision flips around USD 200k/yr of operating expense — above that, the RO tax burden grows faster than the WFOE's overhead.

When to convert to a WFOE

Five signals that the RO has reached the end of its useful life:

- You need to issue fapiao to mainland customers. The RO cannot. The minute a customer requires a B2B VAT-special invoice (mandatory for any meaningful corporate buyer), the offshore-parent invoicing model breaks down.

- You want to hire mainland staff directly. RO labor dispatch costs an extra 10-15% on top of salary versus direct WFOE hire, and the dispatched relationship strains in years two-plus.

- Operating spend crosses USD 250k/yr. The deemed-profit tax at this scale exceeds what a WFOE would owe on real revenue.

- The offshore parent's China revenue exceeds USD 1.5M/yr. Cross-border VAT and withholding tax on the offshore-invoiced model start outweighing the cost of a domestic WFOE that issues fapiao locally.

- The chief rep wants residency stability. RO visas are renewable but capped; a WFOE's legal rep visa has broader stability paths.

Conversion is not in-place — it is dissolve-the-RO + register-the-WFOE. Allow 6-10 months for the full transition; the dissolve and register run in parallel after month two. See converting a Rep Office into a WFOE for the operational sequence.

For the full RO vs WFOE economic comparison see the WFOE vs Representative Office comparison. The parent topic WFOE vs Rep Office vs Hong Kong limited covers the broader structural choice, and the China company formation service hub shows quoted prices for both RO and WFOE setup.

Frequently asked questions

Can I reduce the RO tax bill by reducing reported expenses?

The deemed-profit method requires accurate expense reporting; under-reporting expenses to lower the deemed-revenue base is tax evasion. Operating leaner is fine; misreporting is not.

Is the 15% margin still available anywhere in 2026?

For ROs in remote provinces or in encouraged-industry research categories, yes. Tier-1 city ROs in standard scopes face the 17.5-20% margin almost universally.

Does an RO need to register for VAT separately?

Yes. The RO files quarterly VAT returns on the deemed-revenue base, separate from CIT filing. Most foreign brands let their compliance vendor handle both filings — combined fee is typically RMB 1,200-2,500/month for an RO in the size range above.

What happens to the deemed-profit tax during RO deregistration?

It continues to accrue until the deregistration is complete (4-6 months). Plan the deregistration timing accordingly — closing operationally in Q1 saves a partial Q2 tax bill versus a Q2 close.

Next step

To run the RO vs WFOE economics for your specific operating profile, use the China Expansion Budget Estimator — XLSX with the deemed-profit calculation built in. Side-by-side RO and WFOE tax bills against your inputs. Free.