Year one of a WFOE feels like setup work — register the entity, open the bank account, hire the chief rep, file the first quarterly taxes. Year two is when the recurring compliance grind starts. Spring brings the statutory audit, AIC annual report, and tax annual reconciliation. Foreign founders who handled year one through a setup vendor often get blindsided by year-two recurring obligations that nobody scheduled into the calendar.

This article walks through the two annual filings every WFOE owes, the audit fee range to budget, what auditors actually look at versus what they nod through, what gets a WFOE fined versus what gets it on the abnormal-operations list, and how to survive the first cycle clean. Written for the operator who is approaching the first May-June filing window and wants to know what is coming.

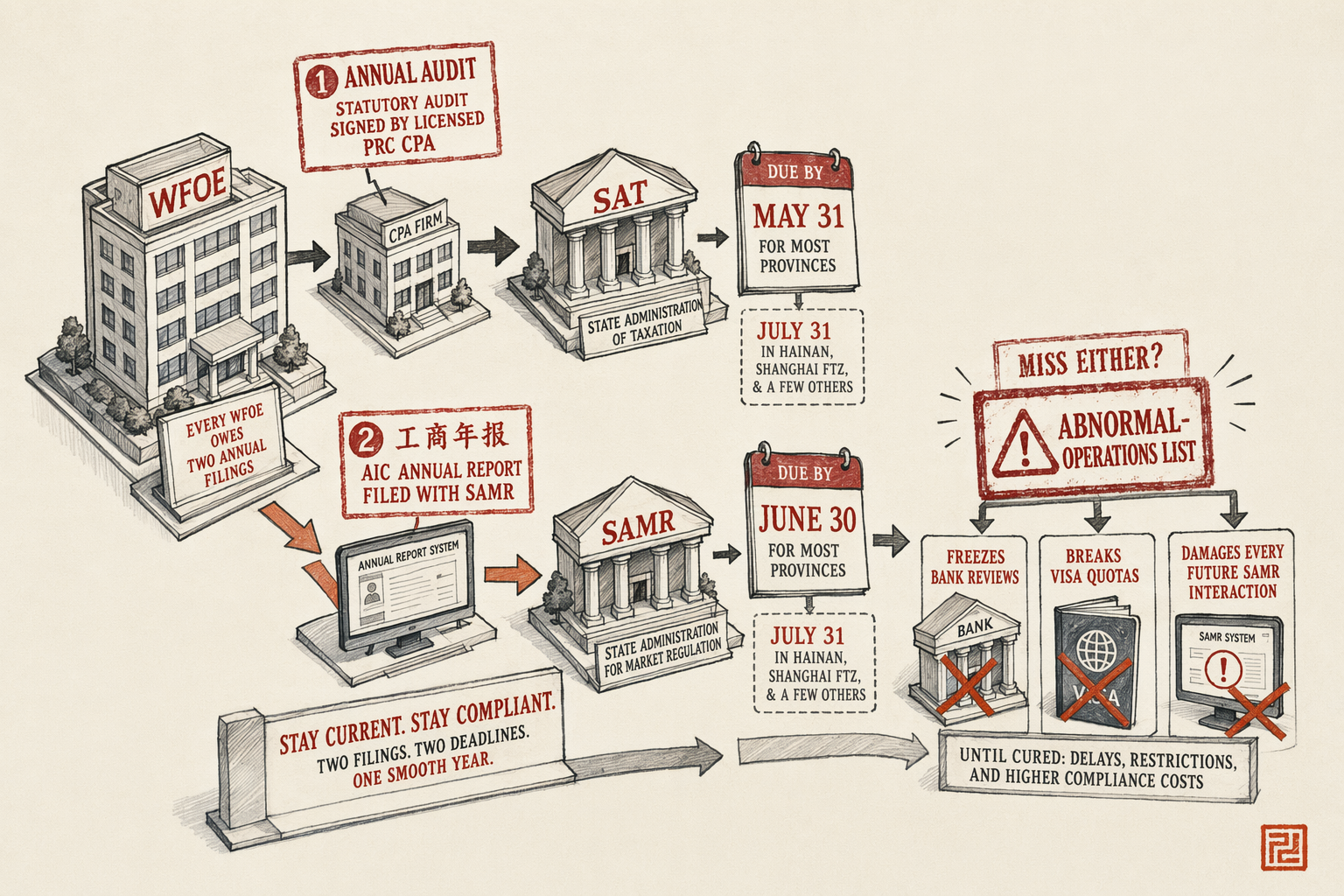

The two annual filings every WFOE owes

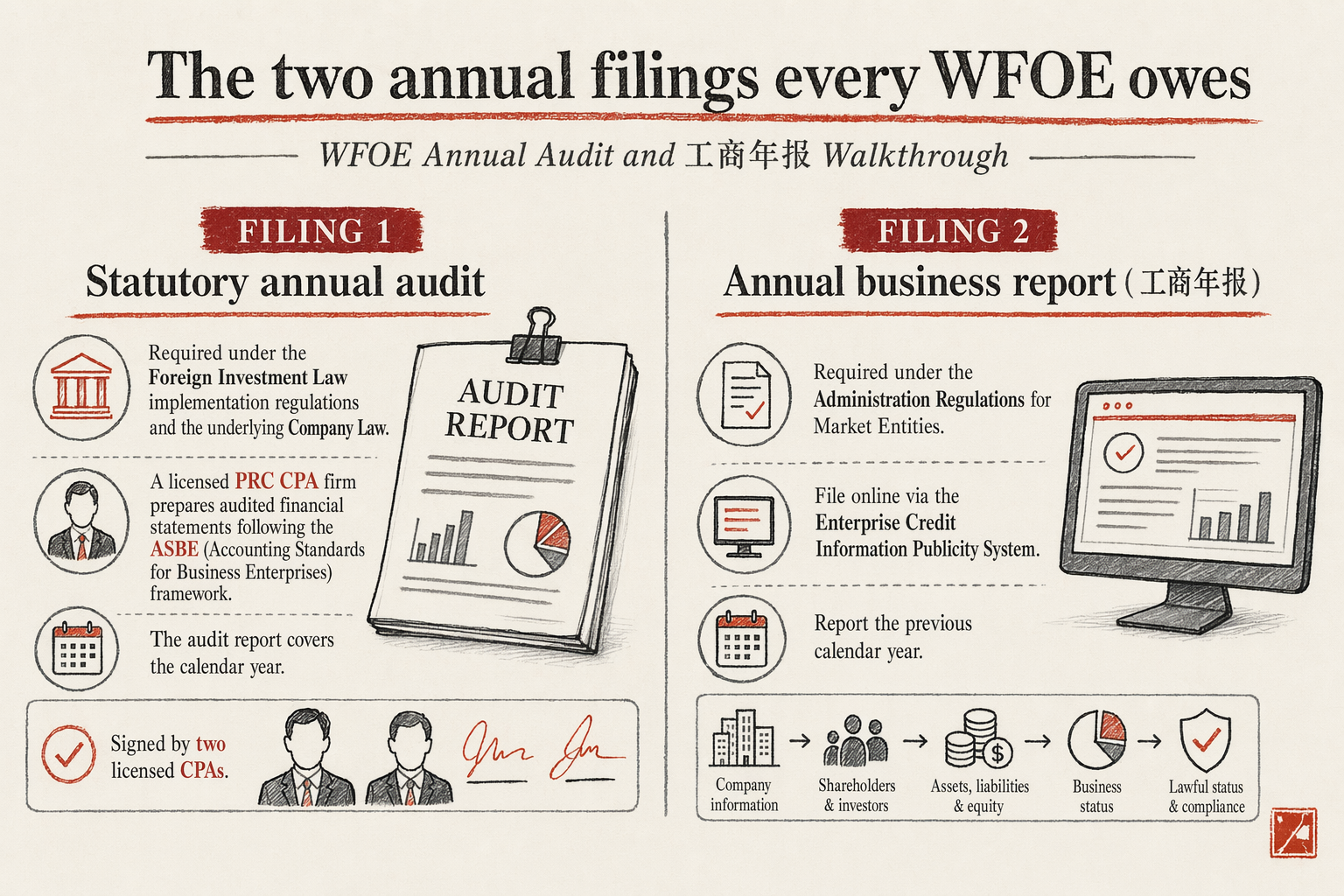

Filing 1 — Statutory annual audit. Required under the Foreign Investment Law implementation regulations and the underlying Company Law. A licensed PRC CPA firm prepares audited financial statements following the ASBE (Accounting Standards for Business Enterprises) framework. The audit report covers the calendar year, is signed by two licensed CPAs of the audit firm, and is filed with the SAT (State Taxation Administration) as the basis for the CIT annual reconciliation. The audit report is also the prerequisite for the 工商年报.

Filing 2 — 工商年报 (AIC annual report). Filed through the National Enterprise Credit Information Publicity System operated by SAMR. Reports: registered capital paid-in status, registered address verification, shareholder identity, foreign-investment information, social insurance enrolment counts, asset and revenue figures from the audited statements, and any material legal proceedings.

Deadline calendar:

- May 31: statutory audit + tax annual reconciliation deadline for most provinces.

- June 30: 工商年报 (AIC annual report) deadline.

- July 31: extended deadlines apply in Hainan FTP, some Shanghai FTZ sub-areas, and during disclosed national disruptions (the 2020 cycle's extension was the most recent broad relaxation).

The 工商年报 cannot be filed without an audit report. The audit cannot be finalized without the year's closed books. The bookkeeping has to be current by end of February at the latest to make the May audit deadline comfortably.

Statutory audit fee ranges by size

Audit fees scale with entity size, complexity, and the CPA firm tier. Working 2026 ranges:

- Small WFOE, under RMB 5M annual revenue, single business line, no cross-border transactions: RMB 8,000-18,000. Tier-3 local CPA firm.

- Mid-size WFOE, RMB 5-30M revenue, 2-3 business lines, modest cross-border activity: RMB 18,000-45,000. Tier-2 regional CPA firm with foreign-WFOE experience.

- Larger WFOE, RMB 30-150M revenue, multi-line with cross-border, related-party transactions: RMB 45,000-120,000. Tier-1 or international-affiliated firm. Required if the parent's consolidated audit references the WFOE.

- Manufacturing WFOE with inventory complexity, capitalized fixed assets, customs filings: add RMB 15,000-40,000 to the band for the increased work.

The temptation to choose the cheapest tier-3 firm is real and usually a mistake for the first audit. Tier-3 firms accept the engagement and then run into questions about cross-border related-party pricing, foreign-exchange treatment, and capital injection accounting that require senior-partner attention they cannot provide. The first audit running late forces the May 31 deadline into extension territory. Tier-2 with foreign-WFOE specific experience is the sweet spot for the first 2-3 cycles.

What auditors actually check

Audit procedure under ASBE is well-defined. The areas where foreign WFOEs trip up:

- Capital injection completeness. Did the foreign parent wire the stated capital tranches on the schedule recorded in the Articles of Association? Auditors trace each tranche from the offshore parent's bank to the WFOE's basic account through the SAFE (State Administration of Foreign Exchange) cross-border record. Missing tranches surface here.

- Related-party transaction pricing. If the WFOE bills the offshore parent for shared services, or buys from a related foreign supplier, the transfer-pricing position is reviewed against arm's-length benchmarks. The 2017 OECD-aligned transfer pricing rules are enforced in mainland through SAT Circulars 6 and 42. Documentation needs to support the prices used.

- Fapiao matching. Every revenue line traces to issued fapiao; every cost line traces to received fapiao. Cash-in-hand transactions, fapiao not yet issued for revenue recognized, fapiao received but not yet booked — auditors flag every one.

- Foreign exchange treatment. Receivables and payables in foreign currency, translation gains and losses, hedging instruments. Auditors validate the rates used against SAFE-published references.

- Inventory and revenue recognition. For trading and manufacturing WFOEs, the year-end inventory count and the cut-off testing on revenue recognition are typically the highest-effort audit areas.

What auditors usually nod through: minor immaterial items, prior-year retrospective adjustments that have no current-year impact, standard depreciation schedules, social insurance reconciliations. The 80/20 of audit work concentrates on capital, related-party, and revenue recognition.

工商年报 (AIC annual report) — what gets you fined

The 工商年报 itself is a structured form on SAMR's national enterprise credit publicity system. Fields include: registered capital paid-in, registered address verification, total assets, revenue, profit, equity, social insurance enrolment counts, foreign-investment metrics, related-party transactions summary, and a declaration of any material legal proceedings or administrative penalties.

Fines and consequences for getting it wrong:

- Late filing (filed between June 30 and end of cycle, typically December 31): RMB 10,000-50,000 per offence under the Company Registration Regulation. Entity is placed on the abnormal-operations list.

- Not filed by year-end: escalates to serious-violation list. Bank reviews fail. Visa quotas freeze. Tax invoice issuance can be restricted. Customers conducting due diligence see the entity flagged.

- Materially false reporting: RMB 30,000-200,000 per offence. Personal liability attaches to the legal rep. Repeat offences can result in license revocation.

- Inconsistency between 工商年报 and audited statements: surfaces in the next audit cycle, requires retroactive amendment, and typically triggers a SAMR clarification request.

The abnormal-operations list is the consequence most foreign founders underestimate. Bank account opening requests, large transaction reviews, customer due diligence, foreign-talent visa applications, and SAFE FX registrations all check the abnormal-operations list. A WFOE flagged for a missed 工商年报 cannot reliably move capital, hire foreign staff, or expand its banking relationships until the flag is cleared — typically 3-6 months after the cure filing.

Surviving the first audit cycle clean

Six things that produce a clean first cycle:

- Bookkeeping current by end of February. The first cycle's bookkeeping carries setup-period transactions that need to be classified correctly. Allow two months of work, not two weeks.

- Capital injection documentation in one folder. Foreign parent wire confirmations, SAFE FDI registrations, basic account credit notices. Auditors will ask for this on day one — having it ready saves a week.

- Related-party transaction memo. One-page memo describing every related-party transaction class, the volume, and the transfer-pricing basis. Pre-empts the auditor's transfer-pricing questions.

- Choose the CPA firm before March. Mid-tier firms with foreign-WFOE experience get booked solid by April. Engagement in February gives the audit two clean months.

- Pre-cycle clean-up of fapiao mismatches. Run a fapiao-to-ledger reconciliation in January. Cure mismatches before the auditor sees them — pre-emptive cure is operational; auditor-caught mismatch is a finding.

- Don't combine the audit firm with the bookkeeping firm. Conflict of interest under PRC auditor independence rules. Separate firms; bookkeeping firm prepares the books, audit firm audits them.

For the broader compliance schedule see the compliance and operations service hub. The parent structural context is in the WFOE vs Rep Office vs Hong Kong limited topic. To budget the audit alongside other recurring compliance line items, the expansion budget estimator includes the audit-fee tier table.

Frequently asked questions

Can a foreign parent's auditor sign the mainland WFOE audit?

No. PRC statutory audits must be signed by two CPAs licensed in mainland China and registered with the Chinese Institute of Certified Public Accountants. Foreign audit firms with mainland-affiliated offices satisfy this; foreign-only audit firms do not.

Is there a small-business exemption from the statutory audit?

No. Every foreign-invested enterprise owes a statutory audit regardless of size. Domestic micro-enterprises have certain reliefs that do not extend to foreign-invested entities.

What if the audited statements show a loss?That is fine. Operating losses are normal in early-year foreign WFOEs and do not by themselves trigger any regulatory action. The audit reports the loss, the 工商年报 records it, the tax return claims the loss as a carry-forward.Can I refuse to give the auditor specific documents on confidentiality grounds?Limited grounds only. Genuine commercial-secret documents can be redacted; auditor independence rules require auditors to flag access restrictions, which becomes a qualified opinion if material. Plan to share what is requested or accept the qualification.

Next step

To build the audit + 工商年报 + tax reconciliation timeline into your operating calendar, use the China Expansion Budget Estimator — page 3 includes the May-July compliance window plotted against the WFOE's first three years. Free XLSX.