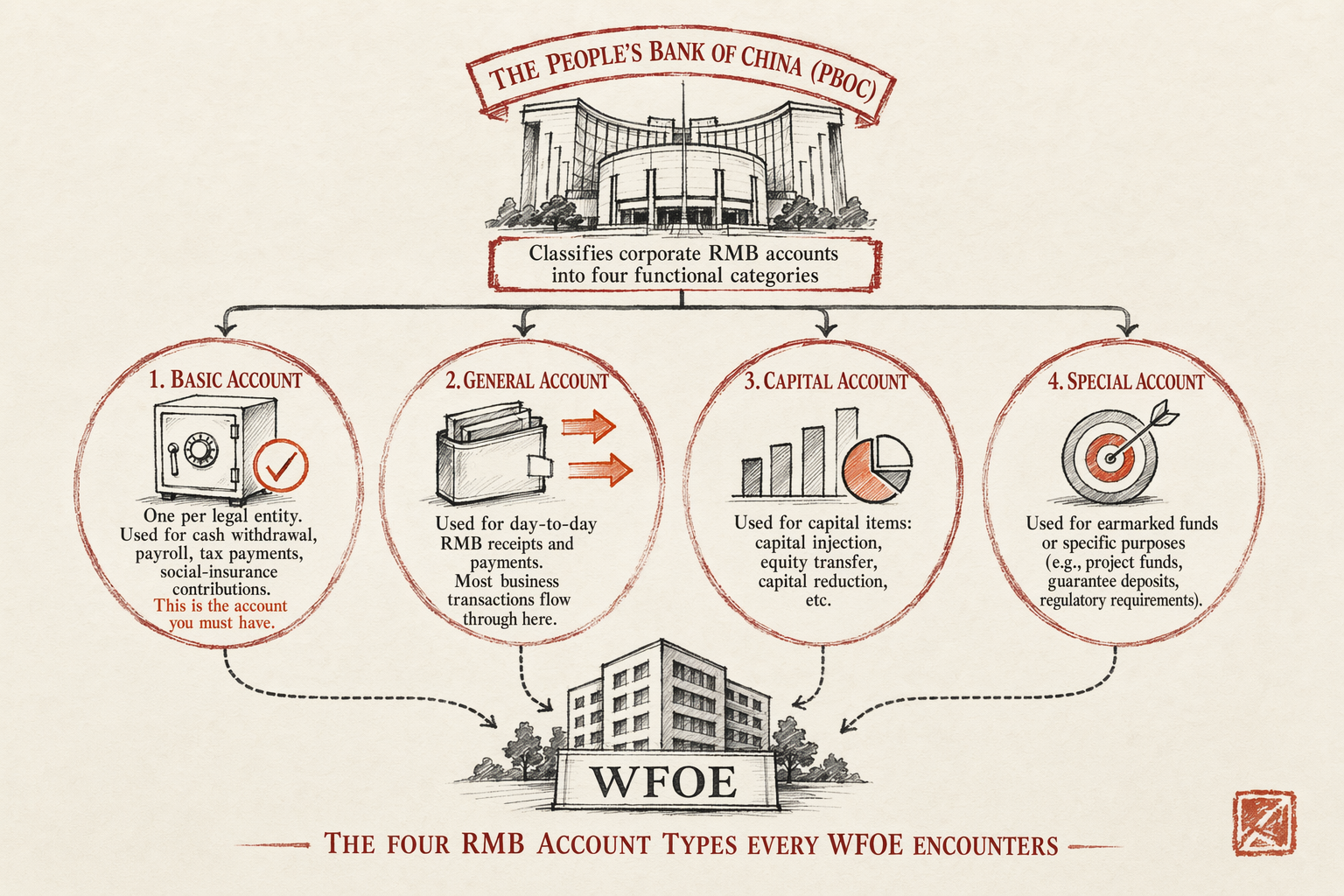

The four RMB account types every WFOE encounters

The People's Bank of China (PBOC, the Chinese central bank) classifies corporate RMB accounts into four functional categories. You will eventually touch at least two of them; some WFOEs end up with all four.

- Basic account (基本户). One per legal entity. Used for cash withdrawal, payroll, tax payments, social-insurance contributions. This is the account the tax bureau links to and the only one that can disburse physical cash above small thresholds.

- General account (一般户). Unlimited in number, opened at any bank. Used for vendor payments, customer collections, transfers between your own accounts. Cannot disburse cash directly to staff (transfers to the basic account, which then pays out).

- Capital account (资本金账户 / 资本金人民币专用存款账户). Holds inbound FX from the foreign shareholder before it gets converted to RMB and swept into the basic or general account. Mandatory if you are receiving registered capital from abroad.

- Temporary account (临时存款账户). A holding account used for one-off purposes — bank-witnessed capital verification before the basic account opens, certain government deposit requirements. Closed after the specific transaction completes.

The architecture is intentional. The basic account is the auditor-visible anchor; general accounts are the operational layer; the capital account is the FX gate. Every WFOE that takes inbound foreign capital winds through all three.

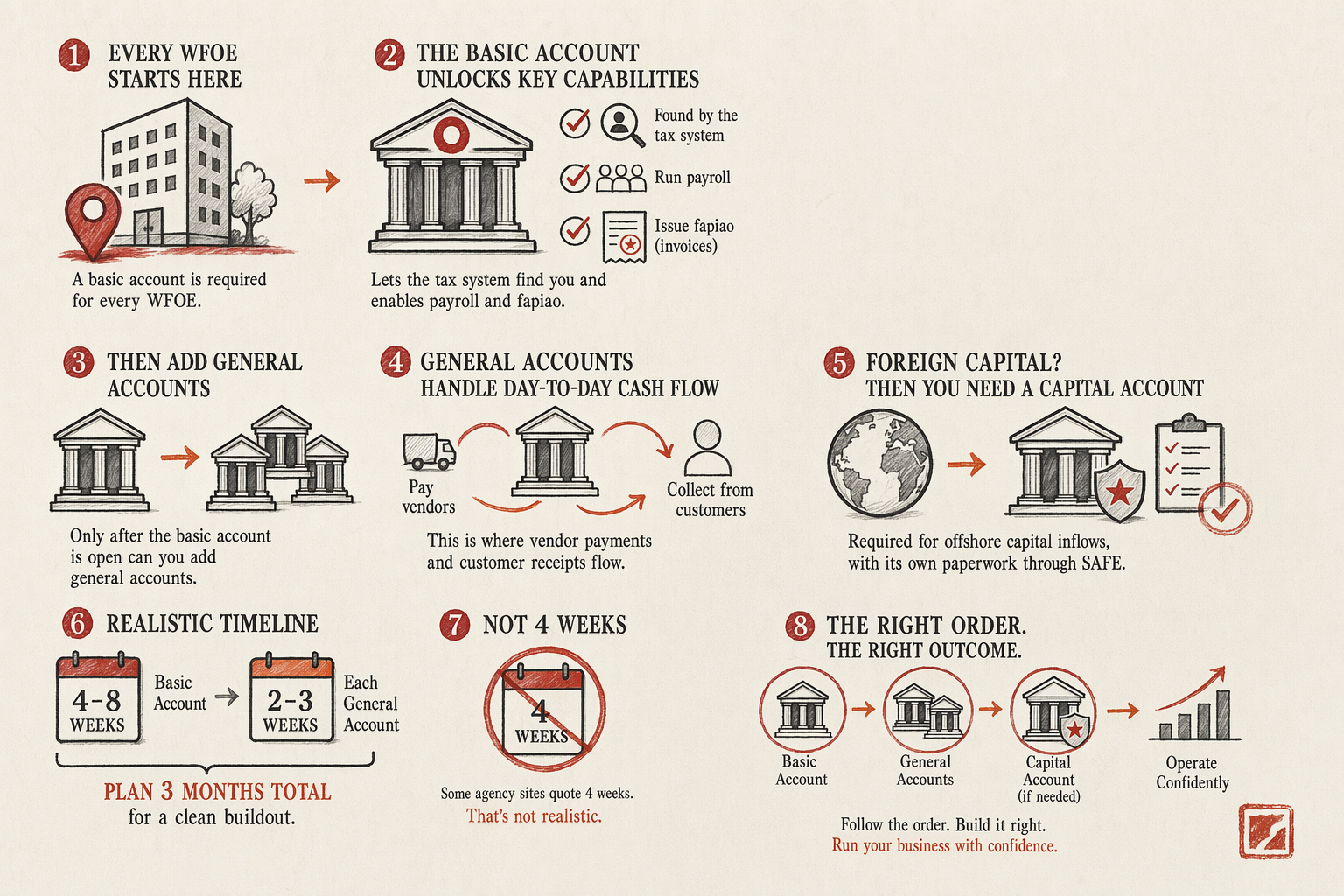

Why the basic account (基本户) must come first

Three things hinge on the basic account, and none of them can happen without it. First, the State Taxation Administration (税务局) cross-links its taxpayer identifier to the basic account number. Until that link exists, you cannot issue a fapiao (发票, the official tax-receipt invoice) and you cannot file VAT returns. A WFOE that has the AIC business license but no basic account is legally alive but economically dead.

Second, social-insurance bureaus and the housing-fund administration require the basic account on the employer registration form. Without it, you cannot enrol your first employee in 五险一金 (wǔxiǎn yījīn — the mandatory five insurances plus housing fund). Without enrolment, you cannot lawfully run payroll, which means you cannot host a Z-visa interview for your first foreign hire.

Third — and this is the rule that catches first-time foreign founders — PBOC's account-opening regulations require any general account application to reference an already-open basic account at another bank. Some branches will accept a temporary capital account in the basic account's place, but most will not. Trying to open a general account at BoC (Bank of China) before the basic account exists at ICBC (Industrial and Commercial Bank of China) lands you in a rejection-then-waitlist loop that nobody warns you about.

The basic account also has to be opened at the bank branch closest to your registered AIC (Administration for Industry and Commerce — now under SAMR, State Administration for Market Regulation) address. Some banks enforce same-district matching; others accept same-city. Pudong-registered WFOEs that try to open the basic account at a Puxi branch routinely get bounced for documentary mismatch. Check the branch list against your registered address before scheduling the legal-rep visit.

Realistic timeline for the basic account, document-clean and address-matched: four to eight weeks from license issuance to active account. The PBOC interagency cross-link adds 5-10 business days at the back end after the bank says the account is open.

What the general account (一般户) unlocks

Once the basic account is live and the PBOC system has cross-linked it, general accounts become straightforward. A general account opens in two to three weeks at any bank, and you can open as many of them as you need — one per bank for operational redundancy, one per business unit if you run separate cost centres, one at a foreign-friendly bank for cross-border flows even if your basic account is at a domestic giant.

What the general account actually does, day to day:

- Pays domestic suppliers. Vendor invoices land here, fapiao reconciliation runs from here.

- Collects from domestic customers. Customer transfers, e-commerce payouts from Tmall or JD, WeChat Pay and Alipay merchant settlements all clear into a general account.

- Holds working capital. Operational cash balance, distinct from the basic account's smaller payroll-and-tax float.

- Provides redundancy. If one bank's systems go down on a Friday afternoon — and they do — you have settlement somewhere else.

The general account does not replace the basic account; it sits beside it. You cannot pay payroll out of a general account directly to staff. You move funds from the general account to the basic account, then payroll disburses from the basic account. The two-step is a feature, not a bug — it creates an audit trail that the tax bureau and the social-insurance bureau can both reconcile against.

Capital account (资本金账户) and FX settlement

If your registered capital arrives from a foreign shareholder, the inbound USD or HKD or EUR cannot land directly in the basic or general account. It lands in the capital account, sits there as FX, and gets converted to RMB through a SAFE (State Administration of Foreign Exchange) settlement transaction before sweeping into the operational accounts.

Two things matter about this account that surprise first-time founders. First, the capital account is a separate application. The bank you chose for the basic account does not automatically open a capital account for you; it requires its own paperwork, its own SAFE pre-registration, and its own foreign-exchange desk approval. BoC's FX desk is the most experienced with this on the foreign-WFOE side; ICBC's FX desk is competent but slower; CMB (招商银行) is fast on the basic side but their FX desk on smaller WFOEs is hit-or-miss.

Second, FX settlement out of the capital account requires a documented use of funds. You cannot convert USD to RMB and let it sit. Each settlement transaction has to point at a specific outflow — a supplier invoice, a payroll obligation, a rent payment — and SAFE will request the supporting documents if the transaction exceeds the no-document threshold (currently USD 50,000 equivalent per transaction, sometimes lower at conservative branches).

If you do not need inbound FX from a foreign shareholder — for instance, you incorporated with debt-financed capital that arrived before WFOE registration, or you are running entirely on revenue once the entity exists — the capital account is optional. Most foreign WFOEs do open one, even if only to keep the option live for future capital top-ups or shareholder loans.

The 6-step opening sequence

The sequence that minimises downtime, based on engagements we have brokered over the last three years:

- Confirm the registered AIC address before applying. The basic account branch will be selected by district. Get the address right at SAMR registration time, not after.

- Pre-register with SAFE if FX is in scope. The SAFE foreign-direct-investment registration (now mostly online via the DigiSAFE portal) takes 1-3 weeks and is a prerequisite for the capital account at any bank.

- Open the basic account first, in person. The 法人 (legal rep) appears at the chosen branch, signs the signature card, witnesses the chop registration, supplies passport plus apostilled corporate documents. Plan 4-8 weeks from this visit to active basic account.

- Wait for the PBOC cross-link. The basic account number gets registered with the local tax bureau via PBOC's interbank settlement system. This adds 5-10 business days. Until it completes, you cannot issue fapiao or enrol staff in 五险一金.

- Open the general account at the same bank or a sibling bank. Two to three weeks once the basic account is live. Most WFOEs open one general account at the same bank as the basic, and a second at a foreign-friendly bank for redundancy.

- Open the capital account if FX is inbound. Coordinate with SAFE timing. A capital injection that lands before the capital account is open sits in suspense at the receiving bank, which generates SAFE notifications and is a paperwork mess.

Full sequence end-to-end, document-clean, runs 8-12 weeks from WFOE license to all three accounts operational. Plan for 14-16 weeks if any single document needs resubmission, which is the median outcome for first-time foreign WFOEs.

For the per-bank requirement matrix and the legal-rep travel packet, see the RMB Banking Checklist. For the bank-comparison framework see ICBC vs BoC vs CMB. For the topic hub linking up to all RMB-banking articles see RMB Bank Account That Clears.

In plain English

If you only read one paragraph: Every WFOE needs a basic account first, which lets the Chinese tax system find you and lets you run payroll and issue fapiao. Only after that account is open can you add general accounts, which is where vendor and customer money actually flows. If foreign capital is coming in from offshore, you also need a capital account, which has its own paperwork through SAFE. Realistic timeline: four to eight weeks for the basic account, then two to three more weeks for each general account. Plan three months total for a clean buildout, not the four weeks some agency sites quote.