What CEPA is and how it works in 2026

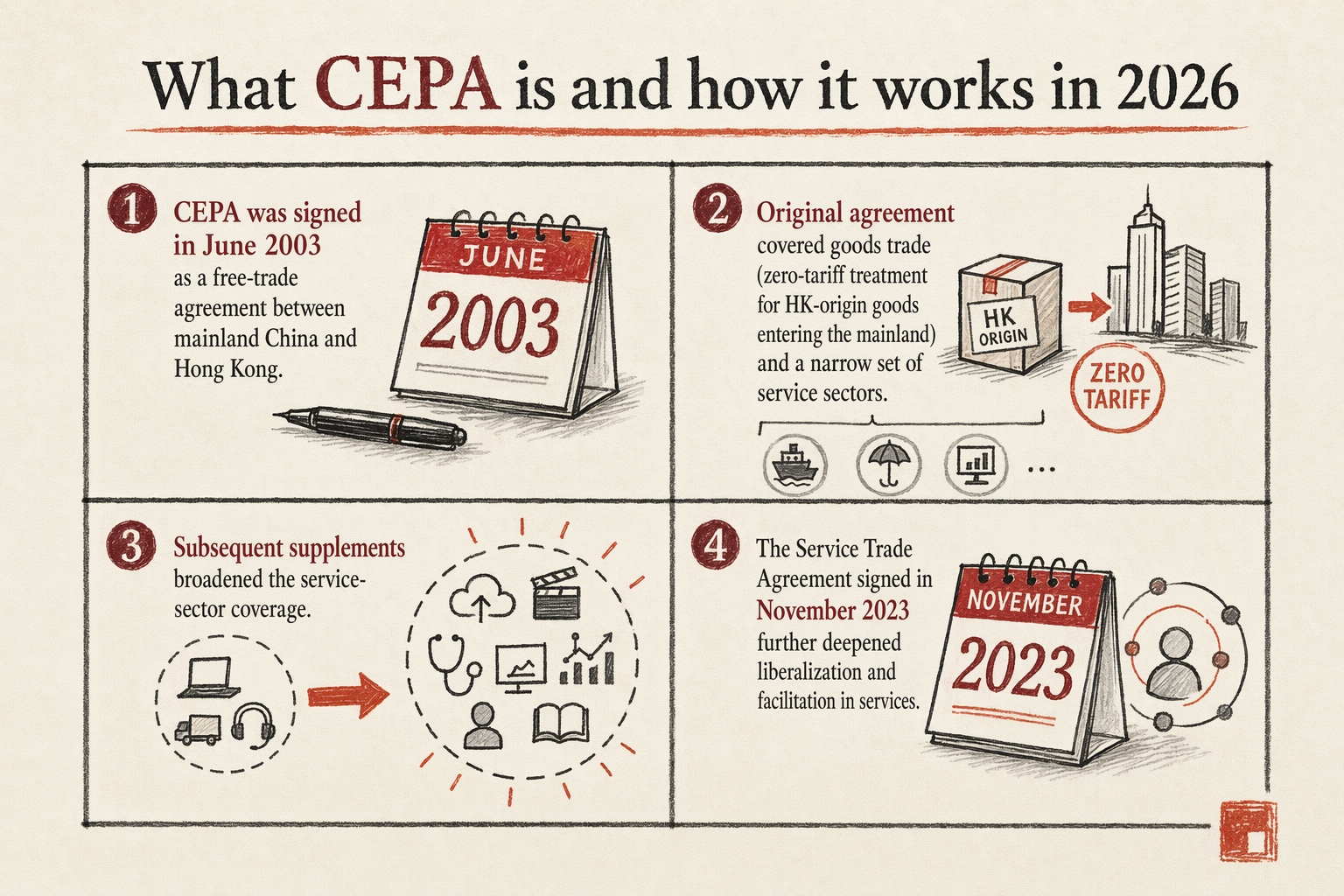

CEPA was signed in June 2003 as a free-trade agreement between mainland China and Hong Kong. The original agreement covered goods trade (zero-tariff treatment for HK-origin goods entering the mainland) and a narrow set of service sectors. Subsequent supplements broadened the service-sector coverage; the Service Trade Agreement signed in November 2015 substantially liberalised the regime; the Goods Trade Agreement signed in December 2018 modernised the goods side. By the 2024 amendments, CEPA covered preferential treatment for HK-registered service suppliers in forty-plus mainland service categories.

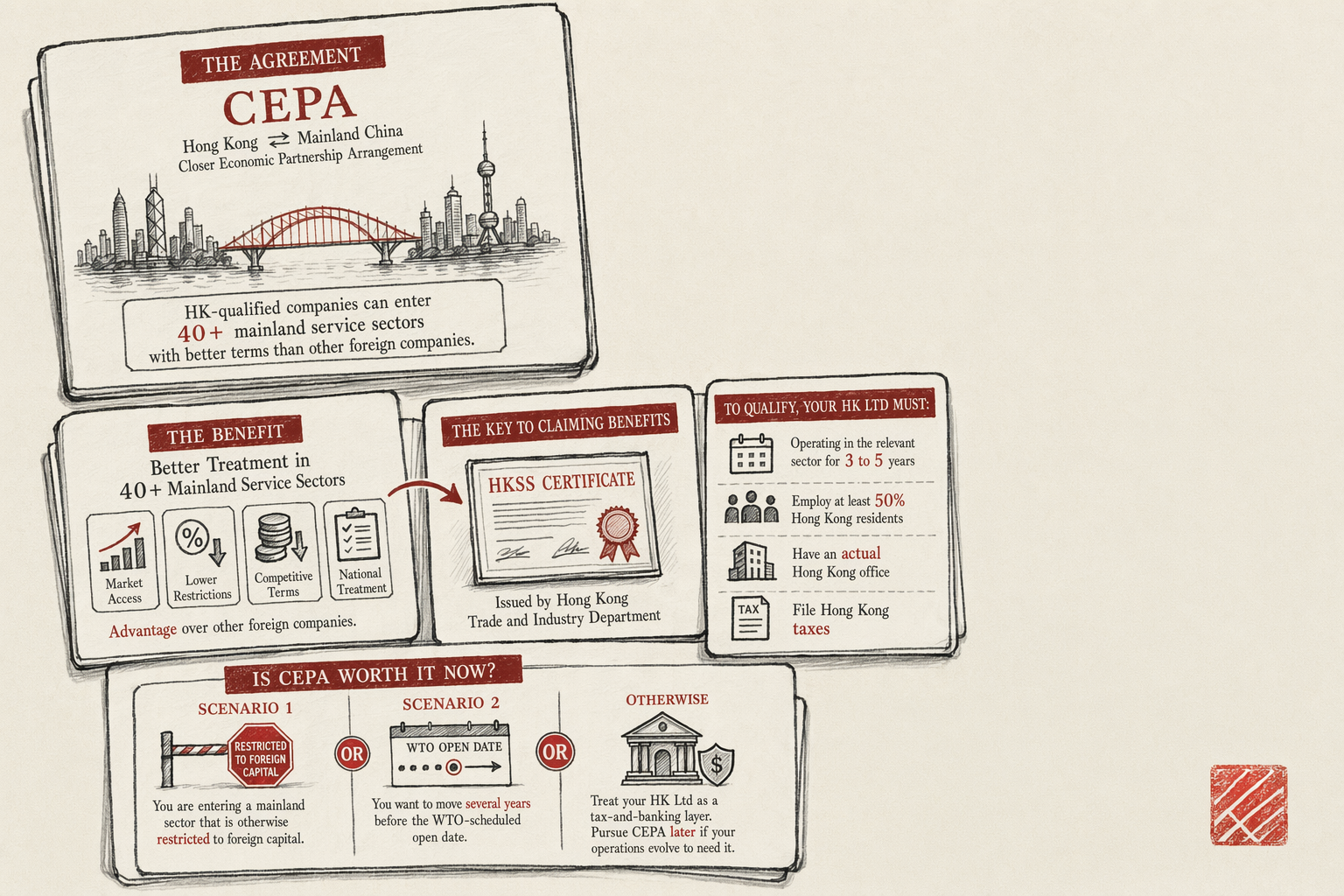

Three concepts make CEPA work operationally. The first is the Hong Kong Service Supplier (HKSS) designation — a certificate issued by the Hong Kong Trade and Industry Department that recognises an HK-registered company as eligible for CEPA preferential treatment. Without an HKSS certificate, the HK Ltd is treated as any other foreign-investment entity by mainland regulators; the CEPA preferences do not apply.

The second is negative-list liberalisation. Mainland regulators publish a negative list of sectors with foreign-investment restrictions; CEPA-qualified HKSSs receive a separate, shorter negative list for those same sectors. In practice this means: a sector restricted to foreign capital but liberalised under CEPA can be entered by an HKSS where it remains closed to a non-HKSS foreign entity.

The third is WTO-default open dates. China's WTO accession commitments include schedules for opening various sectors to foreign competition over time. CEPA-qualified HKSSs enter many of these sectors before the WTO-default open date applies, sometimes by years. The early-mover advantage in regulated sectors is the practical translation of CEPA's strategic value.

The sectors with the strongest CEPA benefits

The forty-plus service sectors covered by CEPA's Service Trade Agreement vary widely in the scale of preference. For foreign-founder use cases that come through chinaonramp, four clusters carry the most consequential benefits in 2026:

Cluster 1: E-commerce and online services. Mainland regulations restrict foreign-capital participation in value-added telecom services (VATS), which includes most online platform businesses. An HKSS qualifies for participation at higher equity ratios than a generic foreign-investment entity, and for specific VATS sub-categories the HKSS can hold majority control where a non-HKSS foreign entity is capped at minority. The practical effect: an HK-founded e-commerce or SaaS business has a faster path to a fully-controlled mainland operating WFOE.

Cluster 2: Professional services. Legal services, accounting services, management consulting, advertising and market research, architectural and engineering services — all have preferential CEPA tracks. HKSS-qualified law firms can enter mainland partnerships with mainland-licensed firms under CEPA's specific arrangements; HKSS accounting firms qualify for cross-border audit work; HKSS architectural firms can practice in mainland projects under lighter licensing requirements.

Cluster 3: IT consulting and technology services. Software development, IT consulting, technical services for hardware integration — all have HKSS-favourable terms. The threshold for HKSS-driven WFOE registration in these categories is lower than for non-HKSS foreign-investment entities; some sub-categories that are restricted to foreign equity caps for generic foreign investors are unrestricted for HKSSs.

Cluster 4: Education and training services (limited). Non-formal education (corporate training, language education, vocational training) has selected CEPA liberalisations. Formal-education sectors (primary, secondary, tertiary) remain heavily restricted regardless of CEPA status.

Sectors where CEPA delivers little or no preference for the typical foreign founder: manufacturing (the mainland-trade WFOE path is already open to foreign capital), cross-border e-commerce on bonded-warehouse models (the cross-border-zone regime applies regardless of HKSS status), pure import-export trading (similarly open), and food and beverage retail (CEPA terms exist but are rarely the binding constraint).

HK Service Supplier (HKSS) status — the gating certificate

The HKSS certificate is issued by the Hong Kong Trade and Industry Department (TID) and is the prerequisite for any CEPA preferential treatment. Without it, the HK Ltd is treated as a generic foreign-investment entity by mainland regulators; with it, the HK Ltd accesses the CEPA-preferential pathways for its qualifying sectors.

The application process is documentary and reasonably fast:

- Eligibility self-assessment. The HK Ltd reviews the published HKSS qualification criteria for the specific service sector it intends to claim. The criteria vary by sector but cluster around three core tests (covered in the next section).

- Application submission to TID. The HK Ltd files the HKSS application form, supporting documents (Business Registration Certificate, financial statements, employment records, tax filings), and an application fee.

- TID review. The Trade and Industry Department reviews the documentation, may request supplementary materials, and decides on certification. Median review time: 4-8 weeks.

- Certificate issuance. The HKSS certificate is issued for the specific sector(s) claimed. The certificate is valid for one year and must be renewed annually.

- Mainland recognition. The HKSS certificate is presented to the relevant mainland regulator at the moment of WFOE registration, sector-licence application, or whichever CEPA-preferential pathway is being claimed. The mainland regulator verifies the certificate with TID and applies the CEPA-preferential terms.

The HKSS certificate is not free-floating; it is tied to a specific service sector. An HK Ltd that operates in multiple sectors needs an HKSS certificate for each one it claims under CEPA. The annual renewal means the HK Ltd has to maintain HKSS-qualifying substance on an ongoing basis, not just at the moment of initial certification.

Substance tests to qualify as an HKSS

Three substance tests drive most HKSS-eligibility decisions. The exact thresholds vary by service sector — the published HKSS criteria for legal services differ from those for IT consulting — but the conceptual structure is consistent.

Test 1 — incorporation and operating history. The HK Ltd must have been incorporated in Hong Kong and engaged in substantive business operations in the qualifying sector for a minimum period before HKSS certification. The minimum operating history is typically 3-5 years depending on sector. A newly-incorporated HK Ltd does not qualify; the HK Ltd needs an operating track record.

Test 2 — HK-resident employees. The HK Ltd must have a minimum number of full-time employees in Hong Kong, of whom a defined percentage must be Hong Kong residents (HKID holders or holders of HK employment visas working from HK). The threshold is typically 50% or higher HK-resident headcount on the full-time staff. The headcount must be documented through Mandatory Provident Fund (MPF) records, employment contracts, and payroll filings.

Test 3 — HK tax filing and operational locus. The HK Ltd must file HK profits-tax returns annually, must have an HK-based office or premises where its substantive operations occur, and must be able to demonstrate that its decision-making and operational management happens in Hong Kong rather than offshore. The Inland Revenue Department's records, the lease for the HK office, and the documented presence of HK-resident directors all contribute to satisfying this test.

The combined effect of the three tests is that HKSS qualification is a multi-year project, not a same-week filing. A foreign founder who wants CEPA benefits has to build the HK substance — an actual HK office, an actual HK team, an actual HK operating history — over three to five years before claiming HKSS status. This is the part of CEPA that the marketing pages tend to gloss over and that the substance tests make unavoidable.

When CEPA actually moves the needle for foreign founders

CEPA delivers practical value for foreign founders in two scenarios. Outside these scenarios, the HKSS-qualification overhead exceeds the benefit and the HK Ltd should be structured as a tax-and-banking layer rather than a CEPA-leveraged entity.

Scenario 1 — entry into a CEPA-favoured restricted sector. The foreign founder is building a business in one of the forty-plus sectors where CEPA provides material market-access preference (e-commerce, VATS, professional services, IT consulting) and the alternative non-CEPA path is either fully closed or capped at minority equity. In this scenario, the multi-year HKSS-qualification project pays for itself because the alternative is no market access at all. Run the substance build deliberately, hire the HK team, file the HKSS, claim the preference at mainland WFOE registration.

Scenario 2 — early market entry ahead of WTO-default open dates. The foreign founder wants to enter a mainland sector where CEPA opens the sector to foreign capital meaningfully earlier than the WTO-default schedule. This early-mover advantage can be substantial in fast-developing sub-categories. The cost-benefit depends on whether the early years of market access produce enough commercial value to justify the substance build.

Outside these two scenarios, the typical foreign-founder HK Ltd should treat CEPA as an option that is potentially valuable in the future but not as a binding constraint on the immediate structure. The HK Ltd functions as a tax-efficient and bank-accessible holding entity above the mainland WFOE; CEPA qualification is something the founder can pursue later if the operating evolution warrants it.

For the topic hub covering HK as gateway see Hong Kong as Your Mainland Gateway. For the parent service see China company formation. For when the HK layer is not the right call regardless of CEPA see when NOT to use Hong Kong. For the tax framework above CEPA see HK profits tax vs mainland CIT.

In plain English

If you only read one paragraph: CEPA is the trade agreement between Hong Kong and mainland China that lets HK-qualified companies enter forty-plus mainland service sectors with better terms than other foreign companies get. To claim those benefits you need an HKSS certificate, which the HK Trade and Industry Department issues only if your HK Ltd has been operating in the relevant sector for three to five years, employs at least 50% HK residents, has an actual HK office, and files HK taxes. So CEPA pays for itself only in two scenarios: when you are entering a mainland sector that is otherwise restricted to foreign capital, or when you want to move several years before the WTO-scheduled open date. Outside those cases, treat your HK Ltd as a tax-and-banking layer and pursue CEPA later if your operations evolve to need it.

Related

7 min read

Hong Kong as Your Mainland-China Gateway

HK Ltd holding mainland WFOE, CEPA benefits, banking dual-track, tax treaty position, common pitfalls.

6 min read

Setting Up an HK Ltd to Hold a Mainland WFOE

Why and how foreign founders use an HK Ltd to hold a mainland WFOE — substance requirements, treaty benefits, banking dual-track.