HK banking after the 2022 reset

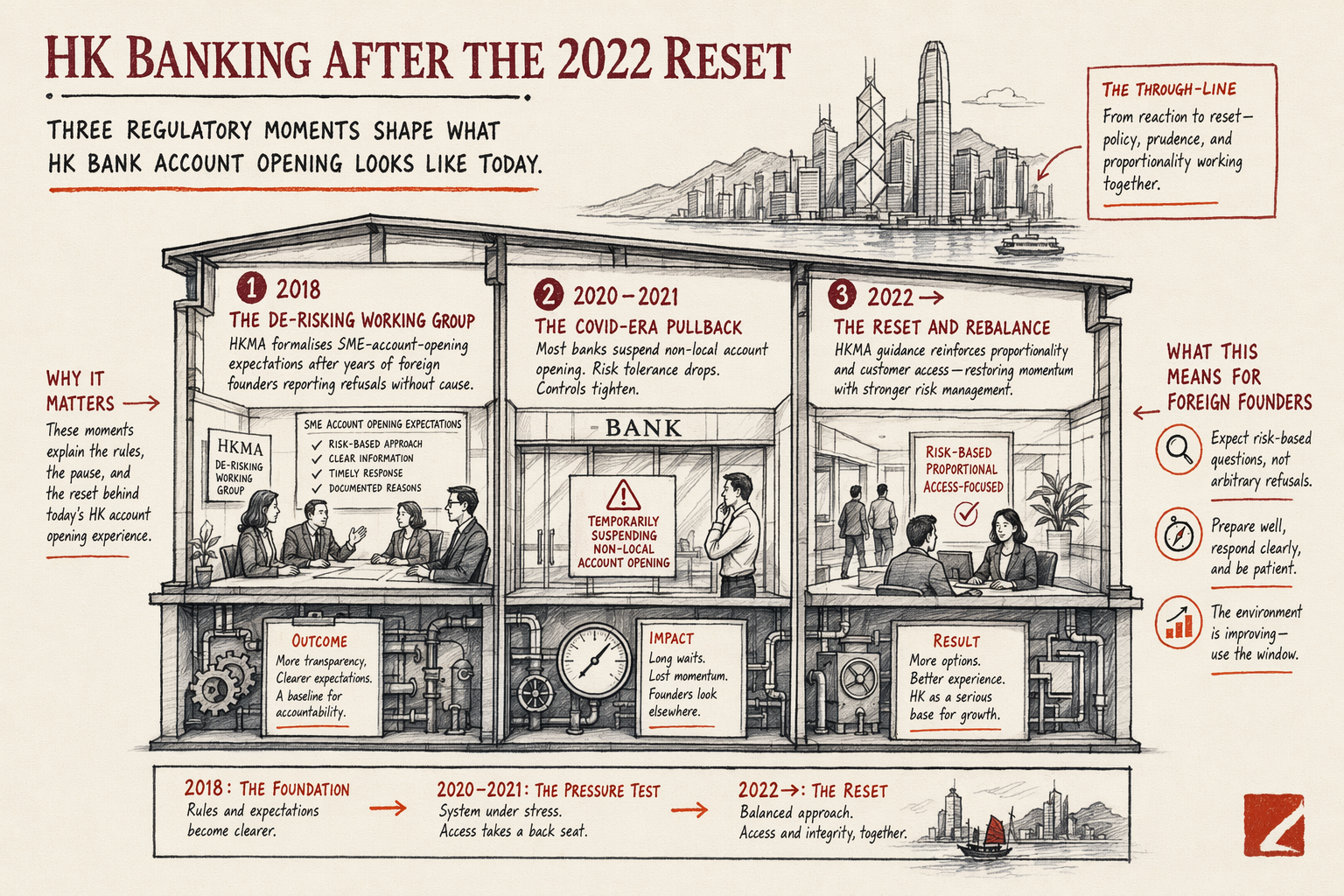

Three regulatory moments shape what HK bank account opening looks like today. The first was the HKMA's 2018 De-Risking Working Group, which formalised the SME-account-opening expectations after years of foreign founders complaining that accounts were being refused without cause. The second was the 2020-2021 COVID-era pullback, when most banks suspended in-person account opening for non-resident applicants and replaced it with limited remote KYC. The third was the post-2022 Companies Registry update, which tightened the Significant Controllers Register requirements and gave banks better documentary visibility into the ultimate beneficial owner.

The net effect for a foreign-founder HK Ltd in 2026 is: HSBC and Standard Chartered require the founder to fly to Hong Kong for in-person KYC at a branch, with 4-6 weeks of documentary review before and after the visit. DBS HK accepts remote video KYC for some applicant profiles but prefers in-person. ZA Bank is fully digital, accepts applicants without an HK visit, and clears most accounts in 1-3 weeks — at the cost of lower account caps and narrower service.

The post-2022 expectations baseline that all four banks apply: the HK Ltd must have an HKD share capital (not just nominal — banks want HKD 10,000 minimum, paid up, with a documented funding source); the directors and significant controllers must be identifiable natural persons (banks do not lend trust to opaque BVI / Cayman structures above the HK Ltd unless the chain is short and explainable); and the operating plan must reference some HK economic activity (not necessarily an HK office, but at minimum HK-counterparty contracts, HK-sourced revenue, or HK-resident staff).

HSBC and Standard Chartered — the incumbent path

HSBC's Business Banking division and Standard Chartered's SME and Business banking offering are the incumbent rails. They handle the largest volume of foreign-founder HK Ltd accounts, the relationship-manager network is the deepest, and the eventual range of services (trade finance, USD wires, multi-currency, FX desk, RMB clearing through their mainland branches) is the broadest. They are also the slowest and the most documentary-heavy.

The typical foreign-founder HSBC HK Ltd account opening:

- Pre-application document review. A relationship manager reviews the Certificate of Incorporation, Articles of Association, Business Registration Certificate, Significant Controllers Register, directors' passports, founders' addresses, and the operating-plan summary. 1-2 weeks.

- In-person KYC at an HK branch. All directors fly to Hong Kong, present originals of identification documents, sign the account-opening forms, undergo a brief interview on the operating plan. 2-4 hours at the branch.

- Post-visit compliance review. The branch submits the file to regional compliance for KYC sign-off. 2-4 weeks. The compliance desk may come back with follow-up questions, particularly on the operating plan and the funding source for the HKD share capital.

- Account activation. Once compliance signs off, the account number is issued and the founder receives the welcome pack with online banking credentials, debit card, cheque book, and security tokens. 1-2 weeks after compliance sign-off.

Total elapsed time, document-clean: 6-10 weeks. Required initial deposit: typically HKD 10,000-50,000 depending on the account tier. Monthly maintenance fees: HKD 200-450 for the basic SME tier, waived above certain balance thresholds.

Standard Chartered's process is structurally identical with slightly different documentation phrasing and a similar 6-10 week timeline. The choice between HSBC and Standard Chartered for a foreign-founder HK Ltd usually comes down to which one has a relationship manager who responds to the initial enquiry. Both produce a similarly good outcome.

DBS HK — middle-ground for tech-sector founders

DBS Bank (Hong Kong) sits between the incumbent rails and the virtual-bank alternative. The bank has a strong SME focus, accepts remote video KYC for some applicant profiles, and clears most foreign-founder accounts in 3-6 weeks — meaningfully faster than HSBC or Standard Chartered. The trade-off is a narrower service offering: less developed trade finance, smaller RMB clearing capacity, fewer relationship-manager resources at higher account tiers.

DBS HK's video-KYC option works for foreign founders where the structure above the HK Ltd is relatively clean (the natural-person UBO is identifiable through one or two layers, the operating plan is plausible, the HKD share capital is documented). The video session itself runs 30-45 minutes through DBS's mobile app, with the founder holding identification documents to the camera and answering pre-set verification questions. Approval typically lands inside the same 3-6 week window as in-person applications.

For a tech-sector foreign founder with an HK Ltd above a mainland WFOE — the most common chinaonramp structure — DBS HK is often the right primary choice. Faster than HSBC, broader than ZA Bank, and the digital banking is competitive with the virtual-bank category despite DBS being a traditional bank. Account caps and monthly fees sit between the incumbent and virtual ranges: HKD 10,000-30,000 initial deposit, HKD 150-300 monthly maintenance, waived at modest balance thresholds.

ZA Bank — fully digital, capacity-constrained

ZA Bank is the virtual-bank option that most foreign founders consider first because the marketing emphasises 'no HK visit needed.' The reality is more nuanced. ZA Bank does accept fully remote applications, and the account-opening turnaround is 1-3 weeks for clean applications — faster than any traditional bank. The trade-offs are real: lower transaction caps (suitable for a small HK Ltd, restrictive for a high-volume one), fewer multi-currency options (HKD and CNH primarily, with USD on a limited basis), and a less developed FX desk if the HK Ltd needs to move significant volumes between currencies.

ZA Bank is the right pick when:

- The founder genuinely cannot travel to Hong Kong (no HKMA-tier bank account is fully remote-only otherwise).

- The HK Ltd is operating at a smaller scale where ZA Bank's transaction caps are not constraining (annual revenue under HKD 10M, individual transactions under HKD 500,000).

- The HK Ltd serves as a holding entity above a mainland WFOE, where the primary banking volume is at the WFOE level on the mainland side, and the HK Ltd needs only modest operational banking.

ZA Bank is the wrong pick when:

- The HK Ltd is the primary operating entity invoicing customers, particularly cross-border customers. The transaction caps will bite.

- The HK Ltd needs trade-finance services, large USD wires, or RMB clearing into the mainland WFOE at scale. ZA Bank's infrastructure is too lean.

- The structure above the HK Ltd is complex. ZA Bank's KYC is fast but not deep; complex structures are better routed to a traditional bank that can review more thoroughly.

A common pattern: open ZA Bank first as the fast-to-launch operational account, while applying in parallel for HSBC or DBS HK as the eventual primary. ZA Bank is operational at week 2; the traditional bank is operational at week 8-10; the HK Ltd has continuous banking throughout.

What substance looks like to an HK banker

'Substance' is the term every HK bank uses but rarely defines. In practice, it means three things the bank wants to see at KYC review:

First, a coherent operating plan. Not a business plan in the venture-capital sense — a short, plain-English summary of what the HK Ltd will actually do. Who are the customers? Where are they (geographically)? What does the HK Ltd sell, deliver, or operate? Where does the money come from and where does it go? A 200-word operating plan that answers these questions cleanly clears KYC more reliably than a 20-page glossy deck.

Second, an identifiable beneficial owner. The Significant Controllers Register is the documentary proof, but banks also want a brief written narrative of who controls the HK Ltd ultimately. A natural person named, with their nationality and country of residence. If the chain above the HK Ltd passes through a BVI, Cayman, or Seychelles entity, the bank wants to know why — and 'tax optimisation' alone is not a great answer; 'limitation of liability for unrelated business segments' is a better one. Be ready to explain.

Third, some HK economic nexus. Not an HK office necessarily — the HKMA explicitly does not require one for SME accounts — but some connection. Examples that satisfy: HK-counterparty contracts, HK-sourced revenue, HK-resident director or shareholder, HK-resident staff, HK-issued service agreements, regular travel to HK for business purposes. The nexus is documentary; the bank reads it from the operating-plan summary and the supporting contracts.

For the topic hub covering HK as gateway see Hong Kong as Your Mainland Gateway. For the parent service see China company formation. For when the HK layer is the wrong call see when NOT to use Hong Kong. For the tax framework above the HK Ltd see HK profits tax vs mainland CIT.

In plain English

If you only read one paragraph: HSBC and Standard Chartered need you to fly to Hong Kong and take six to ten weeks of paperwork; they are the right choice if you need full trade finance and big multi-currency wires. DBS HK is faster, accepts video KYC for some founders, and is the most common right answer for a tech-sector HK Ltd above a mainland WFOE. ZA Bank is fully digital and clears in one to three weeks, but its transaction caps and FX scope are narrow, so it works as a fast-launch account or as a holding entity's banking but not as the primary operating account for high-volume businesses. Banks all want to see three things at KYC: a coherent operating plan, an identifiable natural-person beneficial owner, and some HK economic nexus.

Related

7 min read

Hong Kong as Your Mainland-China Gateway

HK Ltd holding mainland WFOE, CEPA benefits, banking dual-track, tax treaty position, common pitfalls.

6 min read

Setting Up an HK Ltd to Hold a Mainland WFOE

Why and how foreign founders use an HK Ltd to hold a mainland WFOE — substance requirements, treaty benefits, banking dual-track.