WeChat Pay is the in-app payment rails on top of WeChat. It is operated by Tenpay Payment Technology Co Ltd, the Tencent subsidiary licensed by the People's Bank of China as a non-bank payment institution. For foreign brands selling into China, WeChat Pay is the table-stakes payment method. Skip it and you cut yourself off from the majority of mobile-first buyers, who think of cards as something for foreign travel.

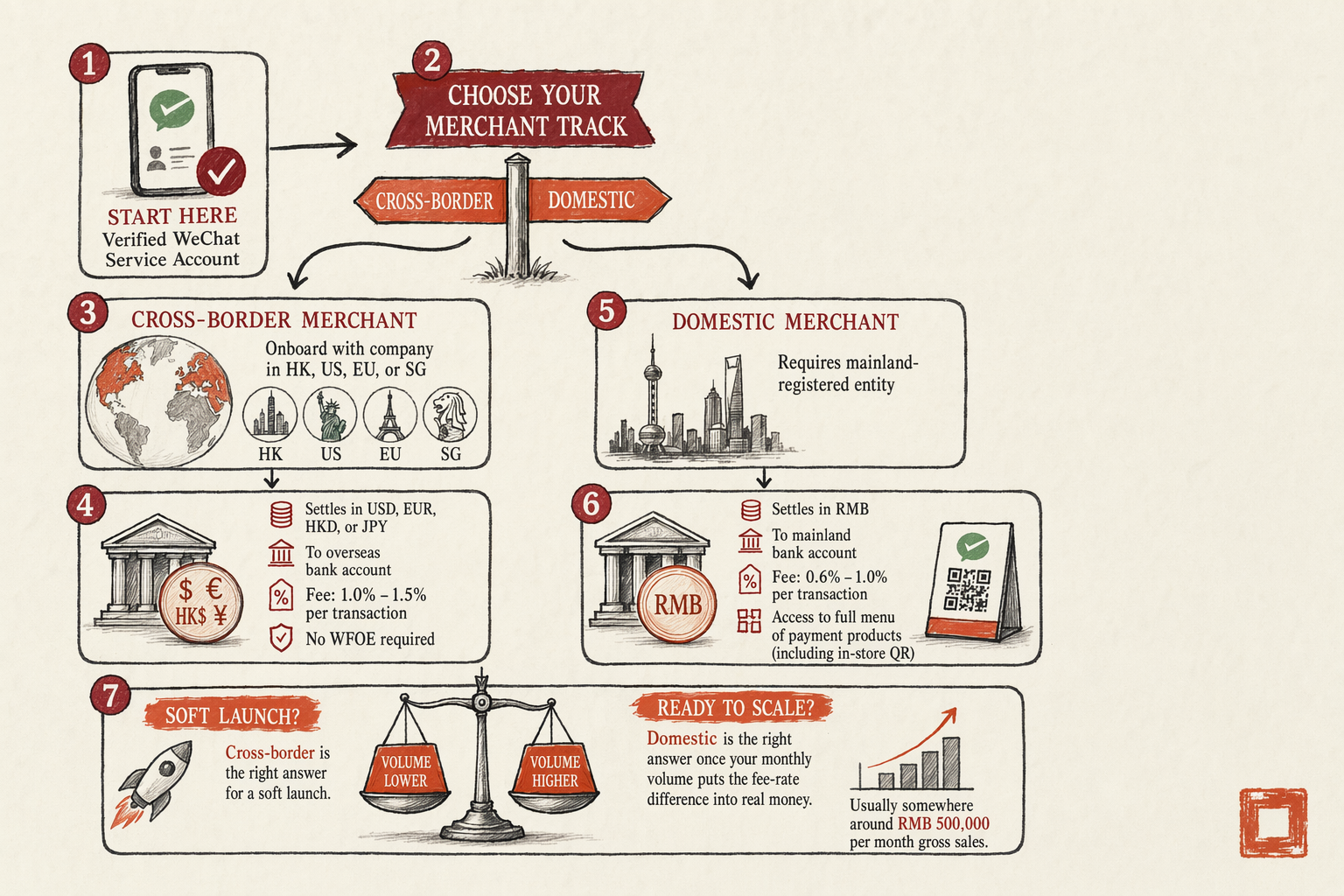

What most foreign founders don't know is that WeChat Pay has two distinct merchant tracks with very different requirements. Picking the wrong one is recoverable but expensive. This article walks both tracks, their actual rates, their settlement mechanics, and which one fits which business model. Both require a verified Service Account (服务号) first — Subscription accounts cannot onboard either track.

Two WeChat Pay merchant tracks

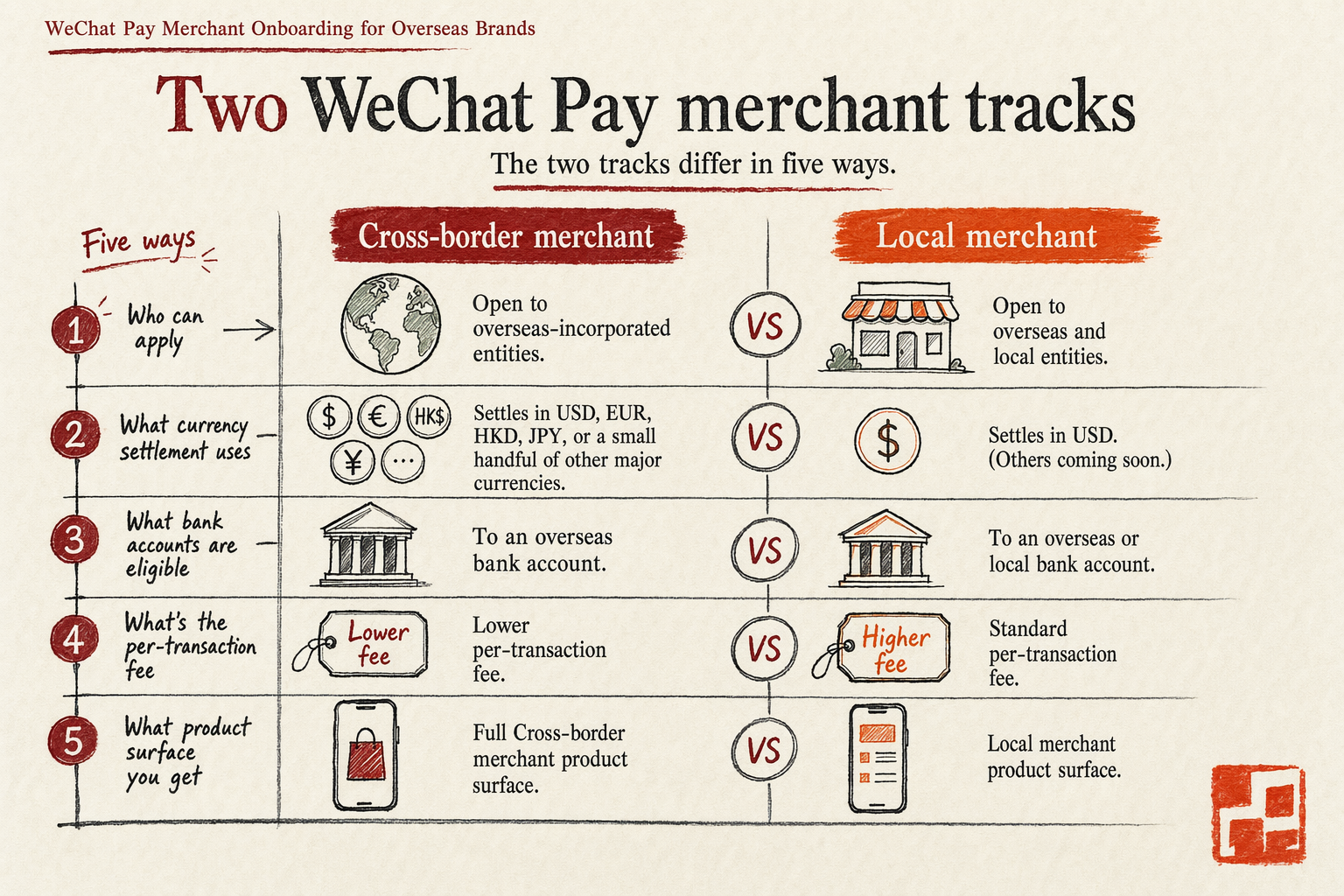

The two tracks differ in five ways: who can apply, what currency settlement uses, what bank accounts are eligible, what the per-transaction fee is, and what product surface you get. Side by side:

- Cross-border merchant (跨境商户). Open to overseas-incorporated entities. Settles in USD, EUR, HKD, JPY, or a small handful of other major currencies to an overseas bank account. Per-transaction fee 1.0-1.5%. Product surface: in-app payments inside Service-account menus, mini-programs, HTML5 pages, and merchant-initiated refunds.

- Domestic merchant (内地商户). Open to mainland-registered entities only — WFOE, joint venture, mainland Ltd, or sole proprietorship. Settles in RMB to a mainland bank account at one of the standard mainland banks. Per-transaction fee 0.6-1.0% depending on industry category. Product surface: everything cross-border gets, plus in-store QR-pay, POS integration, JSAPI for offline merchant integration, mainland-only marketing tools.

The fee-rate difference looks small in percentage terms but compounds quickly. On RMB 1m of monthly volume, the gap between 1.2% and 0.8% is RMB 4,000 a month, RMB 48,000 a year. Whether that justifies the cost and overhead of running a mainland entity depends on your unit economics and how mature your operation is. We keep most clients on cross-border for year one and migrate to domestic once monthly volume crosses roughly RMB 500,000.

One non-obvious detail: a single WeChat Service Account can hold a domestic merchant relationship and a cross-border merchant relationship simultaneously, routing transactions to either depending on context (mainland customer to domestic, overseas customer to cross-border). This is the operating shape of brands at scale. For most first-time foreign brands, this is overkill and adds reconciliation complexity that is not worth it.

Cross-border track — overseas merchant, USD/EUR settlement

The cross-border merchant track is what you want if you are reading this and do not already have a mainland entity. The defining feature is that settlement bypasses China's RMB foreign-exchange controls — your customer pays in RMB inside WeChat, Tenpay converts at the daily fix, and the funds arrive in your overseas bank account in your chosen currency.

Eligible entities are overseas-incorporated companies in jurisdictions Tenpay accepts. The current accepted list includes Hong Kong, US, UK, EU member states, Singapore, Australia, Canada, Japan, South Korea, and a handful of others. Jurisdictions that are not on the list — anywhere FATF flags as high-risk for AML purposes — are rejected at intake.

Documents requested at application:

- Apostilled certificate of incorporation of the merchant entity, same standard as for OA verification.

- Beneficial-ownership disclosure — directors, officers, and any shareholder owning ≥25%, with passport scans and home addresses for each.

- Two years of audited financial statements, or alternatively a bank statement showing meaningful operating turnover.

- A description of the products or services you intend to sell, with sample URLs of the existing overseas-language storefront.

- Bank-account details for the settlement bank account, in the same name as the merchant entity, in an eligible currency.

- The verified WeChat Service Account ID this merchant relationship will attach to.

Review timeline is 5-15 business days when documents are clean, 20-40 when something goes back for revision. Reject rate on first submission runs around 18-30%, mostly for beneficial-ownership documentation issues (the standard is higher than for OA verification) and for industry-category restrictions (regulated medical, supplements, alcohol, financial services, and a few others either need additional licenses or are outright excluded).

Settlement cadence is T+1 or T+3 depending on currency. USD and EUR settle T+1; HKD and JPY settle T+3. The FX rate used is Tenpay's daily fix, which sits roughly 0.3-0.6% off the interbank mid-market rate. This is the hidden cost most foreign brands overlook — the 1.0-1.5% per-transaction fee is supplemented by a 0.3-0.6% FX margin on top.

Domestic track — mainland entity, RMB settlement

The domestic merchant track is the operating shape for any brand running a serious presence inside China. It requires a mainland-registered operating entity — almost always a WFOE (Wholly Foreign-Owned Enterprise), occasionally a joint venture, very occasionally a representative office (which is restricted in what it can transact). The merchant relationship attaches to that entity's business license and settles in RMB to a mainland corporate bank account.

Documents at application include the mainland business license (营业执照), the legal representative's Chinese national ID or passport, the corporate seal (公章) impression, a tax registration certificate, the mainland bank-account opening documents, and the verified Service Account ID. The application is in Chinese, filed through the WeChat Pay merchant portal, and reviewed by a Tenpay team that sits in Shenzhen.

Review timeline is shorter on this track — 3-7 business days for a clean submission, the entity having already cleared the much harder bar of WFOE formation. Reject rate is lower (closer to 8-15%) for the same reason; the entity is pre-vetted by SAMR and the mainland tax authority before WeChat Pay ever sees it.

Settlement cadence is T+1 to the mainland bank account. No FX conversion happens. The per-transaction fee is 0.6-1.0% depending on industry category — physical goods 0.6%, services 0.6%, virtual goods 1.0%, regulated categories (where allowed) up to 1.0%.

One operational catch worth flagging: the mainland bank account that receives settlement is subject to the standard tax-reporting and AML monitoring that any mainland corporate account is. Out-bound RMB conversion to send funds back to a parent overseas is governed by SAFE (State Administration of Foreign Exchange) rules, which we cover under the RMB bank account topic hub. The domestic merchant track is faster and cheaper at the per-transaction level; the friction lives at the repatriation layer.

Rates, settlement cadence, dispute handling

Realistic 2026 rate ranges, by industry category, after the standard onboarding negotiations:

- Physical goods (cross-border): 1.0-1.2%.

- Physical goods (domestic): 0.6%.

- Digital / virtual goods (cross-border): 1.2-1.5%.

- Digital / virtual goods (domestic): 1.0%.

- Services (consulting, professional, education): 0.6% domestic / 1.0% cross-border.

- Travel and hospitality: 0.6% domestic / 1.0-1.2% cross-border.

- Regulated categories (where permitted): case by case, 1.0-2.0%.

Dispute handling is the part nobody warns you about. WeChat Pay chargebacks are rare compared to Western card networks — the consumer-side dispute model is more limited because WeChat Pay sits closer to a bank-transfer than to a credit-card rail. But Tencent's customer-protection programme (in 2022-2024 they tightened buyer-protection rules significantly) does allow disputes for non-delivery, materially-misrepresented goods, and counterfeit-product claims. Average dispute rate across our brokered engagements runs 0.2-0.8%, with most disputes resolved by the merchant providing delivery proof or partial refund.

The settlement holdback is the part to budget for. Tenpay holds a 1-3% reserve on cross-border merchant balances for the first 90 days, releasing the holdback monthly thereafter as long as your dispute rate stays clean. Domestic merchants do not face the same holdback, but mainland tax-reporting requirements mean settlement balances above certain thresholds get visible to the tax authority quickly.

Which to pick by business model

Plain-language mapping:

- DTC brand, $0-5k monthly volume. Cross-border. The per-transaction fee gap doesn't matter at this volume and the WFOE setup cost would dwarf the savings. See the overseas-entity OA path for the prerequisite Service-account verification.

- DTC brand, $5-50k monthly volume. Still cross-border. By month 12 you have data on whether your unit economics support the WFOE setup; until then, the cross-border track is cheaper all-in.

- DTC brand, $50k+ monthly volume. Time to evaluate the domestic track. The fee-rate savings are now material, and the WFOE setup cost amortises within 12-18 months.

- SaaS / digital-goods brand, any volume. Cross-border first, because the 0.4% fee-rate gap is offset by the WFOE overhead and the digital-goods category is friendlier to cross-border settlement than to domestic tax-treatment.

- Industrial / B2B brand selling to mainland buyers on invoice. Often skip WeChat Pay entirely — corporate buyers pay by bank transfer, not WeChat. The OA is for content and lead capture, not transactions.

- Travel / hospitality brand. Domestic merchant once you have a mainland entity, because the in-store QR-pay product is only on domestic and is a meaningful conversion driver for walk-up business.

For the underlying account types both tracks require, see the Service Account vs Subscription Account walkthrough. For the verification path that gates everything, see the WeChat OA verification playbook.

In plain English

If you only read one paragraph: WeChat Pay has two merchant tracks for overseas brands. The cross-border merchant track lets you onboard with a Hong Kong, US, EU, or Singapore company, settles in USD, EUR, HKD, or JPY to an overseas bank account, charges 1.0-1.5% per transaction, and does not need a WFOE (Wholly Foreign-Owned Enterprise) in China. The domestic merchant track requires a mainland-registered entity, settles in RMB to a mainland bank account, charges 0.6-1.0%, and gives you access to the full menu of payment products including in-store QR. Both tracks require a verified WeChat Service Account first. Cross-border is the right answer for a soft launch. Domestic is the right answer once your monthly volume puts the fee-rate difference into real money — usually somewhere around RMB 500,000 per month gross sales.

Related

7 min read

WeChat OA Verification Playbook for Overseas Brands

服务号 vs 订阅号, the overseas-entity verification path, RMB 600 annual fee, payment-API access, menu architecture.

6 min read

How to Choose an ICP Sponsor for Your Domain

Picking an ICP sponsor — entity-tied filings, sponsor fee ranges, support quality, what happens when a sponsor disappears.