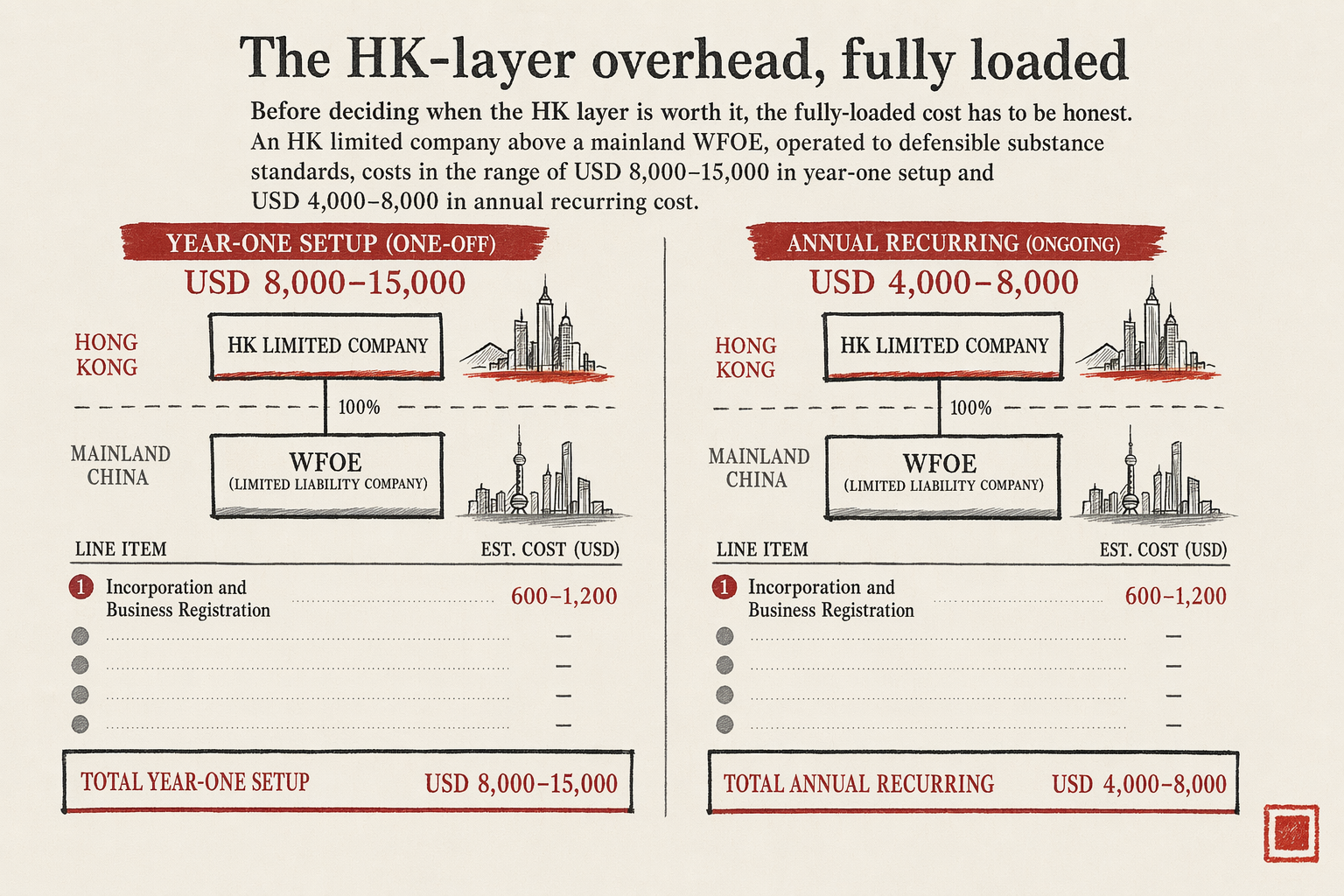

The HK-layer overhead, fully loaded

Before deciding when the HK layer is worth it, the fully-loaded cost has to be honest. An HK limited company above a mainland WFOE, operated to defensible substance standards, costs in the range of USD 8,000-15,000 in year-one setup and USD 4,000-8,000 in annual recurring cost. The line items:

- Incorporation and Business Registration. USD 600-1,200 one-off through a corporate-services provider.

- Registered office and company secretary. USD 800-1,500 per year.

- Annual return filing at the Companies Registry. USD 200-400 per year.

- Annual audit by an HK-registered CPA. USD 1,800-3,500 per year for a small HK Ltd; higher with operational complexity.

- HK profits-tax return preparation and filing. USD 500-1,200 per year, often bundled with the audit.

- HK bank-account opening. Free of bank fees per se, but the founder's flight to HK for KYC plus 6-10 weeks of paperwork — substantial real cost in time.

- HK bank-account ongoing fees. HKD 200-500 per month, partially offset by balance thresholds.

- HK-resident director or company secretary services (if no founder-side HK presence). USD 1,200-2,500 per year.

- Substance build (if HKSS or beneficial-owner status pursued). Add USD 30,000-100,000+ per year for an actual HK office plus HK-resident staff.

The substance build is the line that determines whether the HK layer earns its keep. A pure paper HK Ltd costs USD 4-8k per year and provides limited treaty benefit (the beneficial-owner test for 5% withholding rate may fail). An HK Ltd with real substance costs USD 50k+ per year but delivers the full benefit slate. The middle ground — a thin HK Ltd with token substance — is the worst of both worlds: enough cost to be felt, not enough substance to defend in audit.

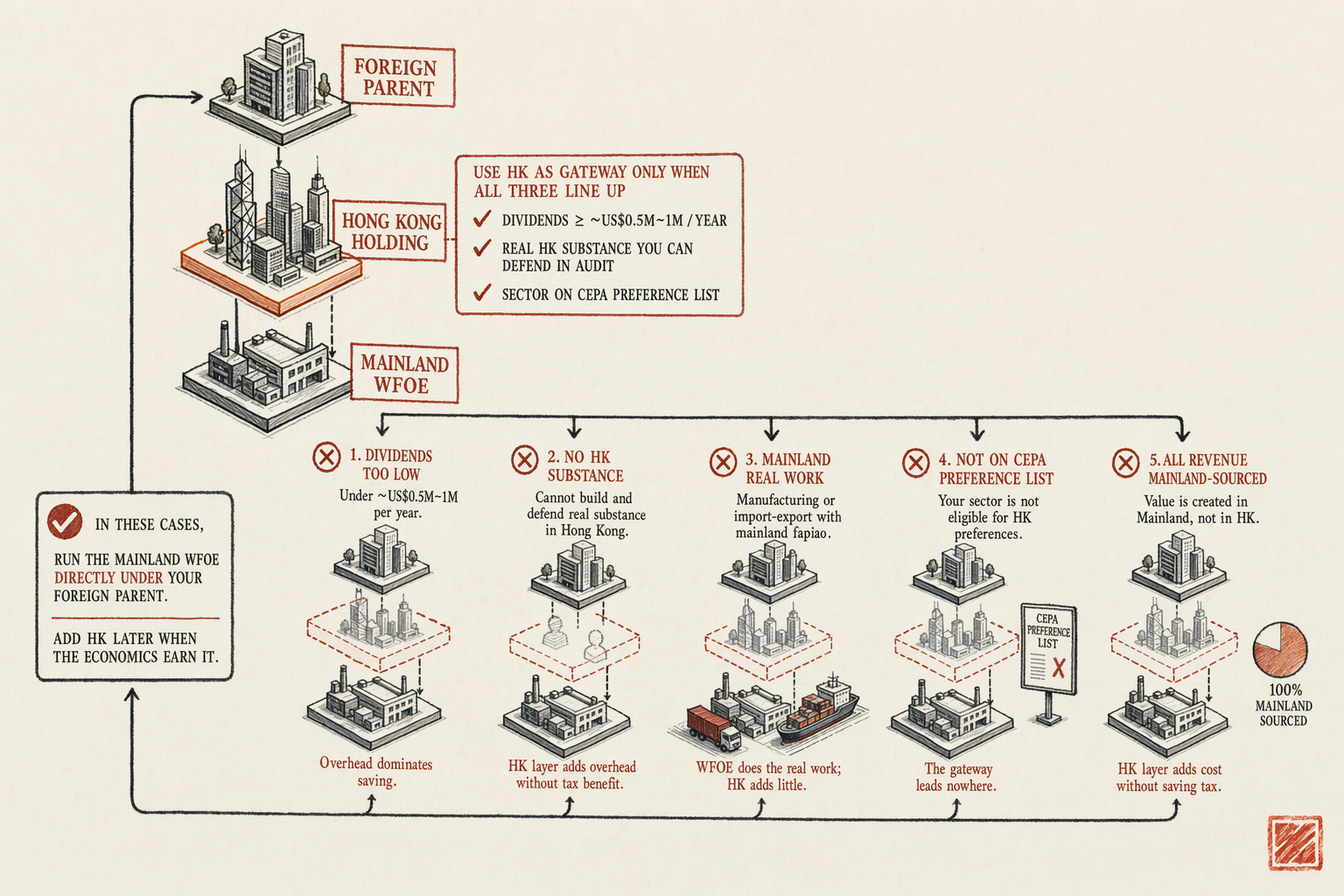

Scenario 1 — mainland-sourced revenue with no HK substance

The first scenario where Hong Kong fails to deliver: the business generates all of its revenue from mainland customers, with no operational footprint or commercial activity in Hong Kong. The structure looks like: foreign founder → HK Ltd (paper) → mainland WFOE (operational). All sales contracts are between the mainland WFOE and mainland customers. All services are delivered in the mainland. All decisions are made by the mainland WFOE's management. The HK Ltd exists on paper only.

Two consequences follow. First, HK profits tax delivers no benefit, because the HK Ltd has no HK-sourced income. The territorial-source rule means a paper HK Ltd with no HK operations has nothing to tax at HK rates; the structure does not produce HK-taxable income in the first place. The 8.25% / 16.5% headline rate is irrelevant.

Second, the dividend-withholding treaty benefit may fail. The 5% rate under the HK-mainland Double Tax Arrangement requires the HK Ltd to satisfy the beneficial-owner test in State Taxation Administration Bulletin 9 (2018). A pure paper HK Ltd without operational substance, without HK-resident directors, without HK office, without HK staff, often fails Bulletin 9 review. The mainland State Taxation Administration's audit of a treaty claim that fails the beneficial-owner test recharacterises the dividend withholding at the 10% non-treaty rate. The 5% saving never materialises.

The cleaner structure for this scenario: foreign founder → mainland WFOE directly, with the HK layer removed. The mainland WFOE distributes dividends to the foreign founder's home-jurisdiction parent at the 10% non-treaty withholding rate, but the structure saves the entire HK overhead and the parent jurisdiction may have its own tax treaty with mainland China that reduces the withholding rate independent of any HK layer.

Scenario 2 — manufacturing or import-export with mainland fapiao

The second scenario: the business does manufacturing inside mainland China, or runs import-export operations that require fapiao (发票, official tax-receipt invoices) issuance for customs and VAT purposes. The operating structure necessarily includes a mainland trading or manufacturing WFOE, because fapiao can only be issued by a mainland tax-resident entity. The HK Ltd cannot issue mainland fapiao; the HK Ltd cannot replace the mainland WFOE for the operational purpose.

In this scenario, the HK Ltd's incremental benefit is limited to dividend-withholding optimisation and overseas-counterparty contracting. Both real, but rarely large enough to justify the overhead when the mainland WFOE is doing all the operational lift. The most common pattern that works: foreign parent → mainland WFOE directly, with overseas-counterparty contracting handled through the foreign parent's existing home-jurisdiction structure rather than a freshly-created HK Ltd.

The exception is when the manufacturing or trading operation has a significant cross-border treasury function — say, a manufacturer that sells globally with foreign-currency receivables and wants a centralised treasury hub. In that case, an HK Ltd as a treasury vehicle (separate from the mainland operating WFOE) earns its keep through FX management and intercompany settlement efficiency rather than through tax arbitrage. This is a different rationale from the standard 'HK above WFOE for tax savings' framing.

Scenario 3 — regulated sector where CEPA does not apply

The third scenario: the business operates in a mainland sector where the foreign-investment regime is restrictive, but the sector is not on the CEPA Service Trade Agreement's preferential list, or the founder does not intend to pursue HKSS (Hong Kong Service Supplier) qualification. The headline 'HK as gateway' benefit collapses because the gateway leads nowhere — the HK layer does not unlock additional market access that a generic foreign-investment entity would not also have.

Sectors where this often applies in 2026: heavy manufacturing under foreign-investment encouragement catalogue (already open to foreign capital without HK help), pure cross-border e-commerce on bonded-warehouse models (the bonded-zone regime applies regardless of structure above the operating entity), real-estate development (HK does not provide preferential treatment), some natural-resources and environmental-services categories.

The diagnostic check: if your sector is on the published CEPA Service Trade Agreement preference list AND you intend to pursue HKSS qualification with the multi-year substance build it requires, the HK layer carries strategic value. If either condition is missing, the HK layer's market-access benefit is zero. Make the structural decision on the cleaner basis of dividend-withholding economics and treasury efficiency alone.

For the CEPA mechanics see CEPA service-trade benefits.

Scenario 4 — economic-substance rule unfailable

The fourth scenario: the founder cannot, even theoretically, build the HK substance that the treaty and operational benefits depend on. No HK office is in the cards (the team will not relocate, the budget will not stretch). No HK-resident staff will be hired (the operating model has no role for HK personnel). No HK-counterparty contracts will arise (the customer base is entirely mainland or entirely outside HK). The substance build that the treaty rates and the FSIE regime require is simply not happening.

An HK Ltd without substance is at risk on multiple lines. The beneficial-owner test for the 5% dividend withholding rate may fail. The FSIE (Foreign-Sourced Income Exemption) rules on offshore passive income (dividends from the mainland WFOE, intercompany interest, royalties) require substantive economic activity, and a no-substance HK Ltd defaults to HK profits tax on the passive income that previously enjoyed territorial-source exemption. The 2022 FSIE amendments specifically targeted this kind of paper structure.

The clean alternative: skip the HK layer and operate directly through the foreign parent's home-jurisdiction structure → mainland WFOE. The foreign parent's home jurisdiction may have its own tax treaty with mainland China (the US-China treaty provides 10% on dividends, similar to the non-treaty mainland rate; the UK-China treaty provides 5% on certain qualifying shareholders; the Germany-China treaty provides 5%; the Singapore-China treaty provides 5%). The right structural answer is often a treaty-aware direct parent rather than a substance-light HK intermediary.

Scenario 5 — revenue under USD 1M making overhead disproportionate

The fifth scenario: the mainland WFOE generates less than USD 1 million in annual revenue, with corresponding profit in the small-low-profit-bracket range (RMB 3M = ~USD 420k or below). The mainland CIT effective rate in this bracket is 5-10%, already lower than the HK profits-tax 8.25% rate even before HK overhead is added. The HK layer cannot improve the headline tax math at this revenue scale; it can only add overhead.

The dividend-withholding optimisation that justifies the HK layer at higher revenue scales also collapses. On a USD 100,000 annual dividend remittance, the 5% vs 10% withholding difference is USD 5,000. The HK overhead (USD 4,000-8,000 per year minimum) consumes the saving entirely. On a USD 50,000 annual dividend, the difference is USD 2,500 and the HK overhead exceeds the saving by 2-3x.

The structural rule of thumb that emerges across brokered engagements: the HK layer makes economic sense when annual dividend flows from the mainland WFOE reach USD 500,000-1,000,000 or higher. Below that threshold, the overhead dominates the saving. Above that threshold, the saving plus the treasury and contracting benefits combine to justify the HK overhead and the substance build.

For the small early-stage WFOE, the recommended pattern is: foreign parent → mainland WFOE directly, with the HK layer deferred until revenue scales. The structure can be restructured later — a holding-company insertion between parent and WFOE is a documented procedure that takes 4-8 weeks and does not disrupt operations. Setting up the HK layer at the wrong time costs more than waiting and adding it when the economics support it.

For the topic hub covering HK as gateway see Hong Kong as Your Mainland Gateway. For the parent service see China company formation. For the tax math that drives the threshold calculation see HK profits tax vs mainland CIT.

In plain English

If you only read one paragraph: Hong Kong is the right offshore layer above your mainland WFOE only when three things line up — meaningful dividend flows (above roughly half a million to one million USD per year), real HK substance you can defend in audit, and a sector where the HK preferences actually help. If your revenue is all mainland-sourced and you cannot build HK substance, the HK layer adds overhead without saving tax. If you are manufacturing or import-export with mainland fapiao, the mainland WFOE is doing the real work and HK adds little. If your sector is not on the CEPA preference list, the gateway leads nowhere. If your revenue is under one million USD, the overhead dominates the saving. In any of these five cases, run the mainland WFOE directly under your foreign parent and add HK later only when the economics earn it.

Related

7 min read

Hong Kong as Your Mainland-China Gateway

HK Ltd holding mainland WFOE, CEPA benefits, banking dual-track, tax treaty position, common pitfalls.

6 min read

Setting Up an HK Ltd to Hold a Mainland WFOE

Why and how foreign founders use an HK Ltd to hold a mainland WFOE — substance requirements, treaty benefits, banking dual-track.