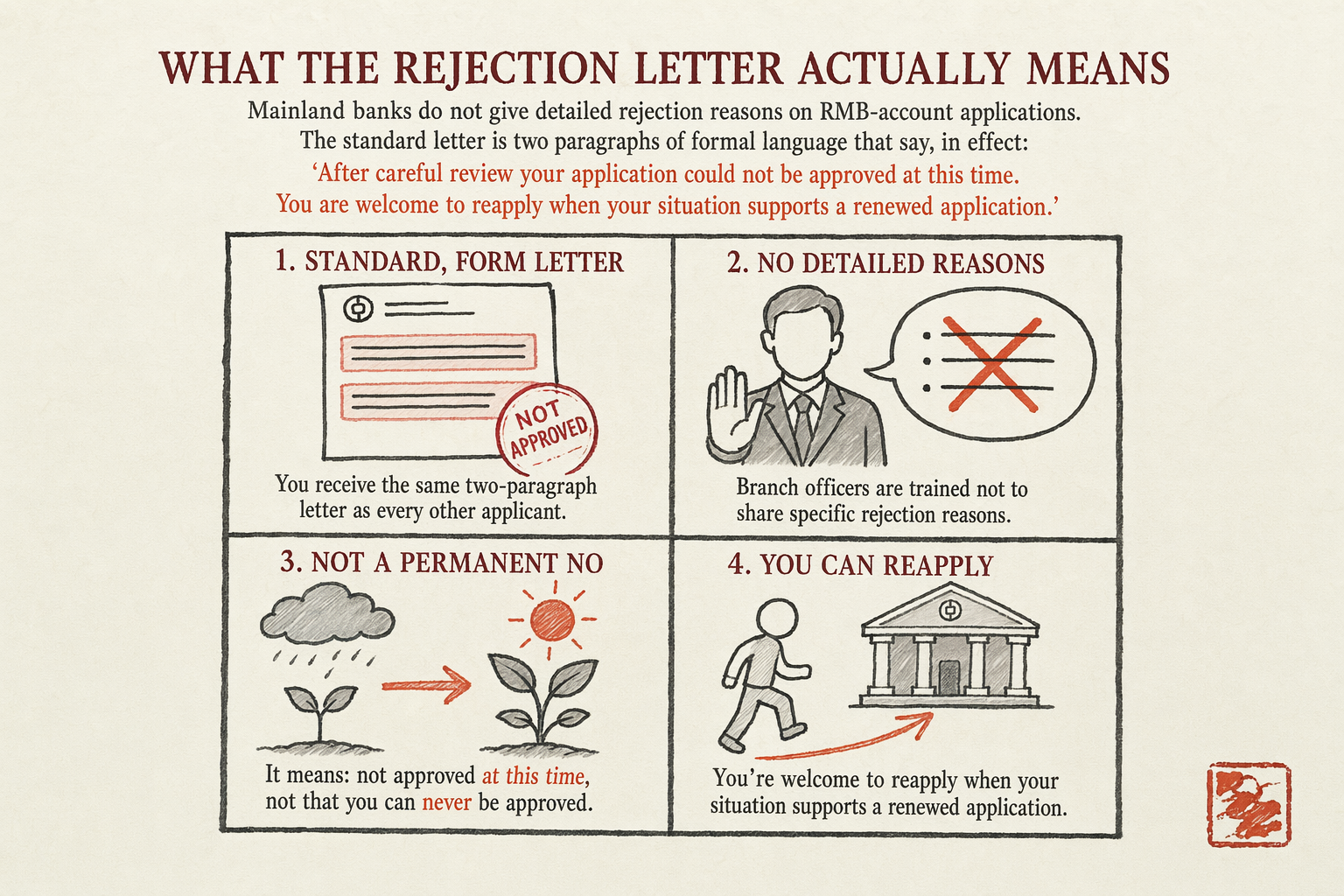

What the rejection letter actually means

Mainland banks do not give detailed rejection reasons on RMB-account applications. The standard letter is two paragraphs of formal Chinese that say, in effect: 'After careful review your application could not be approved at this time. You are welcome to reapply when your situation supports a renewed application.' Branch officers are trained not to disclose specific decline reasons because the underlying compliance flags often come from PBOC anti-money-laundering watchlists, internal sanctions screens, and aggregate KYC risk scores that the bank treats as confidential.

What you can do, in practice, is read the silence. The branch officer who handled the application will usually accept a follow-up conversation that goes one of two directions. Direction one: there is one specific document the officer can quietly point to that needs revision, and they will name it. Direction two: the rejection is at the regional compliance desk's level rather than at the branch's, and the officer cannot help further. Direction one means a documentary fix is possible. Direction two means a structural fix or a different bank.

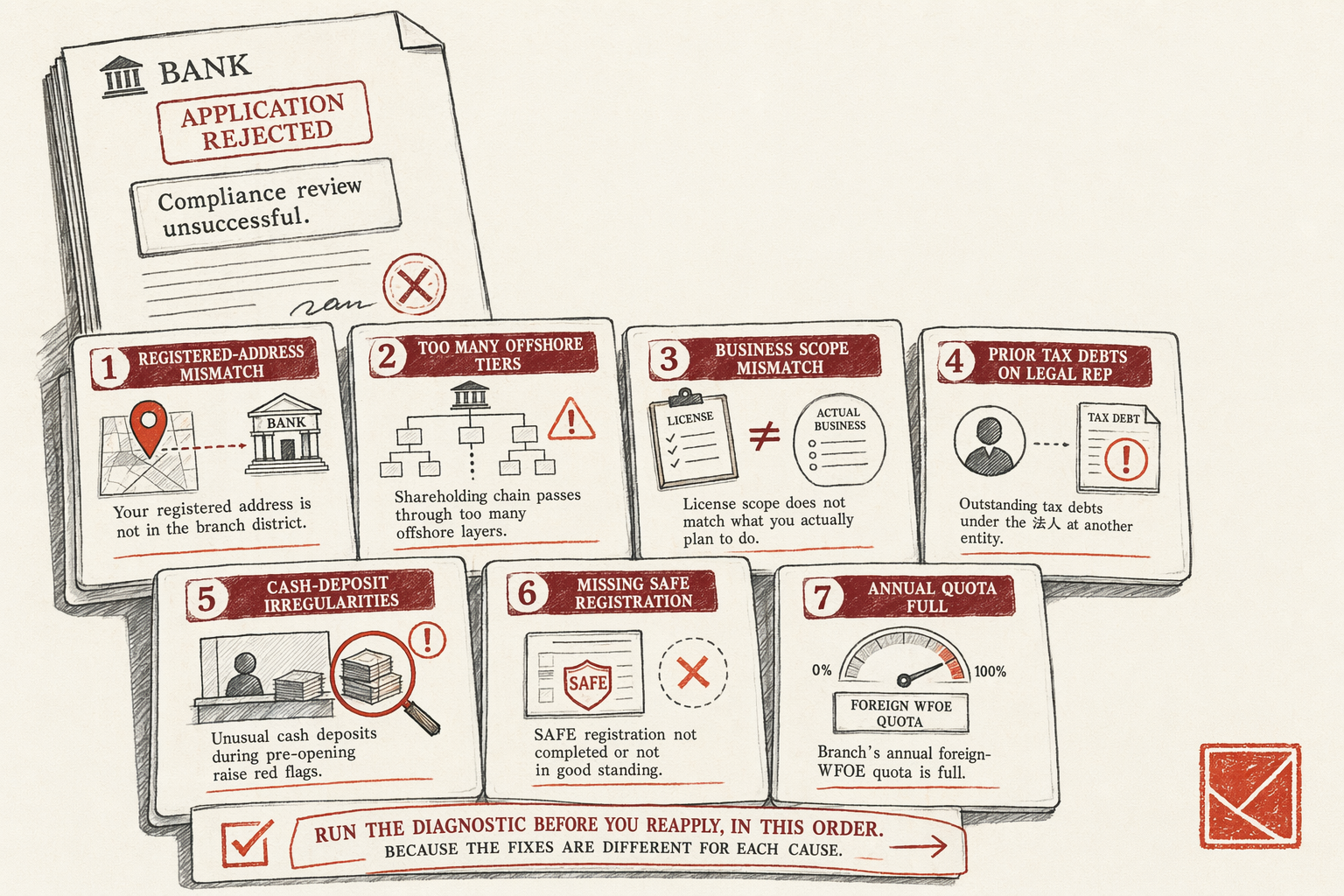

The seven causes below cover roughly 90% of brokered-engagement rejections. The other 10% spread across edge cases — bank's annual quota for foreign-WFOE openings already filled (yes, this happens in Q4), random sanctions-screen false positives that clear on reapplication, regional bureau policy interpretation that changes between the application date and the review date.

Cause 1 — registered-address mismatch

Single most common cause. The WFOE's registered address on the SAMR (State Administration for Market Regulation) business license must match the branch jurisdiction where the basic account is being applied for. The matching standard varies by bank and by city:

- ICBC and BoC. Usually require same-district match in Tier-1 cities (Beijing, Shanghai, Shenzhen, Guangzhou). Same-city match is sometimes accepted in Tier-2 and Tier-3 cities.

- CMB. Same-district match in most cities, with narrow same-city exceptions for branches that have foreign-WFOE specialist desks.

A Pudong-registered WFOE that applies at a Puxi ICBC branch fails on this cause. A Qianhai-registered WFOE that applies at a Luohu CMB branch fails on this cause. The fix is either to apply at the correct-district branch — usually the cleanest path — or, if the registered address is being changed anyway, to file the SAMR address-change first and apply at the new district's branch.

A second-order version of this cause shows up when the registered address is a virtual office. AIC site inspections at virtual-office addresses sometimes find no operational presence, the address gets flagged in the AIC's central database, and the bank picks up the flag at KYC review. See AIC site-inspection triggers for the inspection-side mechanics.

Cause 3 — business-scope mismatch with operations

The 经营范围 (jīngyíng fànwéi — business scope) on the SAMR business license is the legally-defined set of activities the WFOE is allowed to conduct. The application form for the basic account asks what the WFOE actually plans to do operationally. When the two answers diverge, the bank flags the mismatch.

The two common patterns:

- Scope is broader than operations. The business license lists 'technology development, technology consulting, technology services, sales of mechanical equipment, import-export trade' and the WFOE actually plans to do only SaaS sales. The bank asks why the licensed scope is so much broader than the planned operations, and the answer 'we wanted future flexibility' often does not satisfy compliance review for foreign-owned entities. The fix is to narrow the scope at SAMR before the bank application.

- Scope is narrower than operations. The business license says 'technology consulting' but the WFOE's planned operations include 'e-commerce sales of consumer products through Tmall Global.' The bank refuses on grounds that the licensed scope does not cover the planned operations. The fix is to expand the scope at SAMR.

Scope amendments at SAMR take 2-4 weeks for foreign-owned WFOEs. They are not free of friction (especially expansions into licensed-industry scope categories) but they are routine. See WFOE business-scope language for the drafting framework that reduces this rejection cause.

Causes 4-7 — the rest of the cluster

Cause 4 — Prior 法人 tax debts under another entity. Mainland tax-bureau records cross-reference the legal rep's identity. If the 法人 named on the WFOE's SAMR business license also serves as 法人 on a different entity that has outstanding tax debts, social-insurance arrears, or unresolved disputes, the new bank application gets declined. The bank does not always tell you the cross-reference is the cause; the founder discovers it when the same 法人 fails repeatedly across multiple banks. The fix is to clear the outstanding obligations on the prior entity, or to swap the 法人 to a clean candidate before the next application.

Cause 5 — Cash deposit irregularities during pre-opening verification. Some banks (most ICBC branches, some BoC branches) require a small temporary deposit during the pre-opening capital verification, typically RMB 10-100. The deposit clears through a temporary account before the basic account opens. If the deposit comes from an unexpected source (a personal account of the 法人 rather than the WFOE's pre-incorporation capital channel), the bank flags the irregularity. The fix is to route the temporary deposit through the documented capital channel.

Cause 6 — SAFE pre-registration missing. Banks check SAFE's database during the basic-account application for any WFOE expecting foreign capital. If the SAFE foreign-investment information registration is not on file, the bank declines pending SAFE completion. See SAFE registration for cross-border FX inflows for the SAFE-side prerequisites.

Cause 7 — Bank's annual foreign-WFOE quota already filled. Each mainland branch has internal allocation targets for new foreign-owned WFOE accounts, usually set at the regional headquarters level. In Q4, branches that have hit their target for the year sometimes stop accepting new foreign-WFOE applications until January. The decline letter does not name this cause; the branch officer will sometimes mention it informally. The fix is to apply at a different branch within the same bank, or to wait until the new fiscal year.

Diagnostic order before reapplying

Before reapplying anywhere, run through this diagnostic in order. Each step is cheap to check and the order is roughly highest-likelihood to lowest-likelihood for foreign-WFOE rejections:

- Verify registered address vs branch district. Cheapest check. Look up the bank's branch list for the registered-address district; confirm the branch you applied to is on the list.

- Map the shareholding chain end-to-end. Count the entities between the natural-person UBO and the mainland WFOE. If the count is 3+, prepare a UBO-disclosure document with rationale for each intermediate.

- Compare business scope with operations plan. Read the SAMR business license and the bank application side-by-side. If the two diverge, file a scope amendment at SAMR before reapplying.

- Check the 法人's record on other entities. Run a National Enterprise Credit Information Publicity System query (国家企业信用信息公示系统, the public AIC database) on the 法人's name. If the 法人 is named on other entities with adverse records, swap or resolve before reapplying.

- Confirm SAFE registration is in place. Pull the SAFE database entry to confirm the WFOE's foreign-investment information registration exists.

- Confirm temporary-deposit channels are documented. If a temporary deposit was made during verification, confirm the source-of-funds documentation matches the pre-incorporation capital channel.

- Ask the branch officer informally about quota. If everything above checks out and the rejection happened in Q4, ask the branch officer (off the record) whether the foreign-WFOE quota has been hit for the year.

Diagnostic time: 2-4 hours for the full sweep. The cost of running the diagnostic in order is much lower than the cost of resubmitting at a second bank and getting the same rejection for the same documentary reason.

For the parent topic linking up to all RMB-banking articles see RMB Bank Account That Clears. For the parent service see Ongoing Compliance.

In plain English

If you only read one paragraph: Banks do not tell you why they declined your RMB-account application; the letter just says 'compliance review unsuccessful.' Seven causes cover almost all foreign-WFOE rejections: registered-address mismatch with the branch district, shareholding chains that pass through too many offshore tiers, business scope on the license not matching what you actually plan to do, prior tax debts on your 法人 under a different entity, cash-deposit irregularities during pre-opening, missing SAFE registration, and the branch's annual foreign-WFOE quota being full. Run the diagnostic before you reapply, in that order, because the fixes are different for each cause.

Related

7 min read

Opening an RMB Business Account That Actually Clears

Basic vs general account, legal-rep in-person rules, KYC red flags, cross-border FX (SAFE) registration, ICBC vs BoC vs CMB.

6 min read

How to Choose an ICP Sponsor for Your Domain

Picking an ICP sponsor — entity-tied filings, sponsor fee ranges, support quality, what happens when a sponsor disappears.