Industry view

China Market Entry for SaaS Companies

Mainland-hosted SaaS, PIPL posture, WeChat Work, ICP for product surfaces, and the 2-5 local AE hire — sequencing for B2B SaaS market entry.

Email Mike—

Y1 cost band

Mike's running benchmarks

—

Time to first revenue

Mike's running benchmarks

—

Common pivot at month 12

Mike's running benchmarks

B2B SaaS companies entering the mainland Chinese market have one of the most structurally favorable profiles among the foreign-business categories. The product can run on global infrastructure with a mainland-region data plane for latency. The contracting entity does not have to be mainland-domestic for most enterprise buyers. The sales team can be sponsored through an Employer of Record rather than a WFOE. The customer-success channel runs cleanly on WeChat Work without any mainland operating commitment. None of that is the case for industrial manufacturers, cosmetic brands, or medical devices — those verticals all face structural floors that SaaS does not.

What SaaS does face is a specific data-handling regulatory layer (PIPL, ICP, MLPS), the procurement-side question of whether the contracting entity is one a mainland AP team can pay against, and the practical question of how the customer-facing latency feels to mainland end users. This page walks through what SaaS companies typically need, what the regulatory layer actually requires, the entity-structure pattern that fits most first-time entrants, the rejection patterns we see, and the realistic timeline and budget band for a sequenced market-entry engagement. If you are a B2B SaaS founder, COO, or head of international thinking about your first mainland buyers, the content below is the operational map.

What B2B SaaS companies typically need in the mainland market

The asks from a mainland B2B SaaS launch tend to cluster into five operational categories. Some are universal; some are conditional on the buyer profile.

One — contracting and invoicing capability that mainland procurement teams can process. Mainland enterprise AP teams need a contract they can categorize (international service vendor, software service vendor, or mainland-domestic software vendor), an invoice they can pay against (USD wire from offshore is acceptable for most multinationals; RMB-denominated with fapiao becomes a hard requirement for SOE buyers and a subset of Chinese-domiciled enterprises), and a vendor entity that maps to one of the recognized procurement-side classifications. A Hong Kong limited company contracting in USD covers most buyers. A mainland WFOE issuing fapiao covers the remainder. Most first-time entrants start with HK Ltd and graduate to WFOE when the buyer mix demands it.

Two — product latency and data residency that holds up in procurement security reviews. Mainland-end-user latency from US-hosted SaaS infrastructure is typically 180-280ms, which feels visibly slow on interactive UIs and is genuinely problematic for any product with real-time-collaboration features. Deploying the customer-data plane on a mainland-region cloud (Aliyun, Tencent Cloud, or AWS China) drops latency to sub-50ms. Beyond the user-experience benefit, the data-residency posture matters for procurement: mainland enterprise security reviews routinely ask where customer data is stored, and “mainland China” is the answer that clears the review fastest.

Three — a customer-facing communication channel that mainland buyers prefer. Mainland enterprise SaaS buyers run on WeChat Work (企业微信) as the primary day-to-day communication channel with vendors. Email is acknowledged for formal deliverables; WeChat Work is where the relationship lives. SaaS companies that try to run mainland customer success on email alone experience a friction that they often misdiagnose as “the customer is unresponsive.” The fix is a WeChat Work tenant on the SaaS company's contracting entity, integrated with the customer-success CRM.

Four — sales-team coverage that can engage Mandarin-only buyers. Early enterprise pilots can run on remote AE coverage from Singapore, Hong Kong, or the home country if the buyer is a multinational subsidiary with English-speaking procurement. Mainland-staff coverage becomes necessary when the addressable buyer profile shifts to Chinese-domiciled enterprises. Mainland-staff coverage does not require a WFOE — EOR sponsorship of 1-3 mainland-based AEs is the standard first-stage pattern.

Five — a regulatory posture (PIPL, ICP, MLPS) that holds up in security and procurement reviews. The mainland-specific regulatory layer is covered in the next section. The short version: you need a PIPL representative, a Chinese-language privacy policy, an ICP filing on any mainland-hosted customer-facing surface, and an MLPS-level-2 cybersecurity self-assessment if you cross specific volume thresholds.

The vertical's specific regulatory layer — PIPL, ICP, MLPS

Beyond the generic structure work, B2B SaaS has three vertical-specific regulatory regimes that determine whether the operation is compliant.

PIPL (Personal Information Protection Law, 个人信息保护法). Enacted 2021, effective 2021. The mainland-Chinese analog to the EU GDPR (General Data Protection Regulation). PIPL applies to processing of personal information of natural persons located in mainland China, regardless of where the processing happens. For B2B SaaS, this means any product that handles end-user data — names, emails, phone numbers, IP addresses, behavioral data, device identifiers — for mainland users is in scope. Minimum compliance obligations include: appointing a PIPL representative (a designated person or organization in mainland China that can receive regulatory communications), publishing a Chinese-language privacy notice that meets PIPL's specific content requirements, providing data-subject access and deletion mechanisms accessible in Mandarin, executing a Standard Contract (the CAC-issued template) for any cross-border transfer of personal information, and maintaining a record of processing activities.

The thresholds where PIPL escalates from minimum compliance to active CAC assessment: cross-border transfer of personal information for more than 100,000 individuals annually, transfer of sensitive personal information for more than 1,000 individuals annually, transfer of personal information from a CIIO (Critical Information Infrastructure Operator), or transfer of important data as defined by sector-specific guidance. SaaS at early-mainland-entry scale is usually below all of these thresholds, which means the Standard Contract pathway is sufficient and the full CAC security assessment is not required. Track your customer-data volume; the thresholds can be crossed quickly at scale.

ICP (Internet Content Provider) filing or license. Required for any website or web-application surface hosted on mainland-China-resident servers. For B2B SaaS, the trigger is whether the customer-facing product UI is hosted in mainland China. If yes (because you put the data plane on Aliyun and the UI lives there too), ICP filing is mandatory — and the filing is held by the entity that operates the surface, not by Aliyun. If your contracting entity is an HK Ltd, the filing has to be sponsored through a licensed mainland sponsor (Aliyun and Tencent Cloud both operate enterprise-sponsor programs for overseas operators), or you have to put a mainland entity in the structure to hold the filing directly. ICP filing for a B2B SaaS product surface is typically the lighter 备案 tier, not the heavier 许可证 license — the license tier triggers when the product handles payment, marketplace activity, or distributed content. Most B2B SaaS sits cleanly under filing-tier scope. The ICP filing guide covers the full picture.

MLPS (Multi-Level Protection Scheme, 网络安全等级保护, often called 等保 or DJBH). The mainland-Chinese cybersecurity classification system. Five levels, with Level 1 being the lightest (self-assessment, low-risk systems) and Level 5 being the heaviest (national-security-critical systems requiring direct regulator inspection). For B2B SaaS handling enterprise customer data of mainland buyers, Level 2 is the typical assessment level — a documented self-assessment of the security posture against the MLPS Level 2 control set, filed with the local cybersecurity bureau, refreshed periodically. Some procurement teams (especially in financial services, healthcare, and SOE buyers) require MLPS Level 3 from their vendors, which is a substantively more demanding assessment that includes third-party testing. Map your buyer profile to the MLPS level you will need; design the security posture to meet it from day one rather than retrofitting.

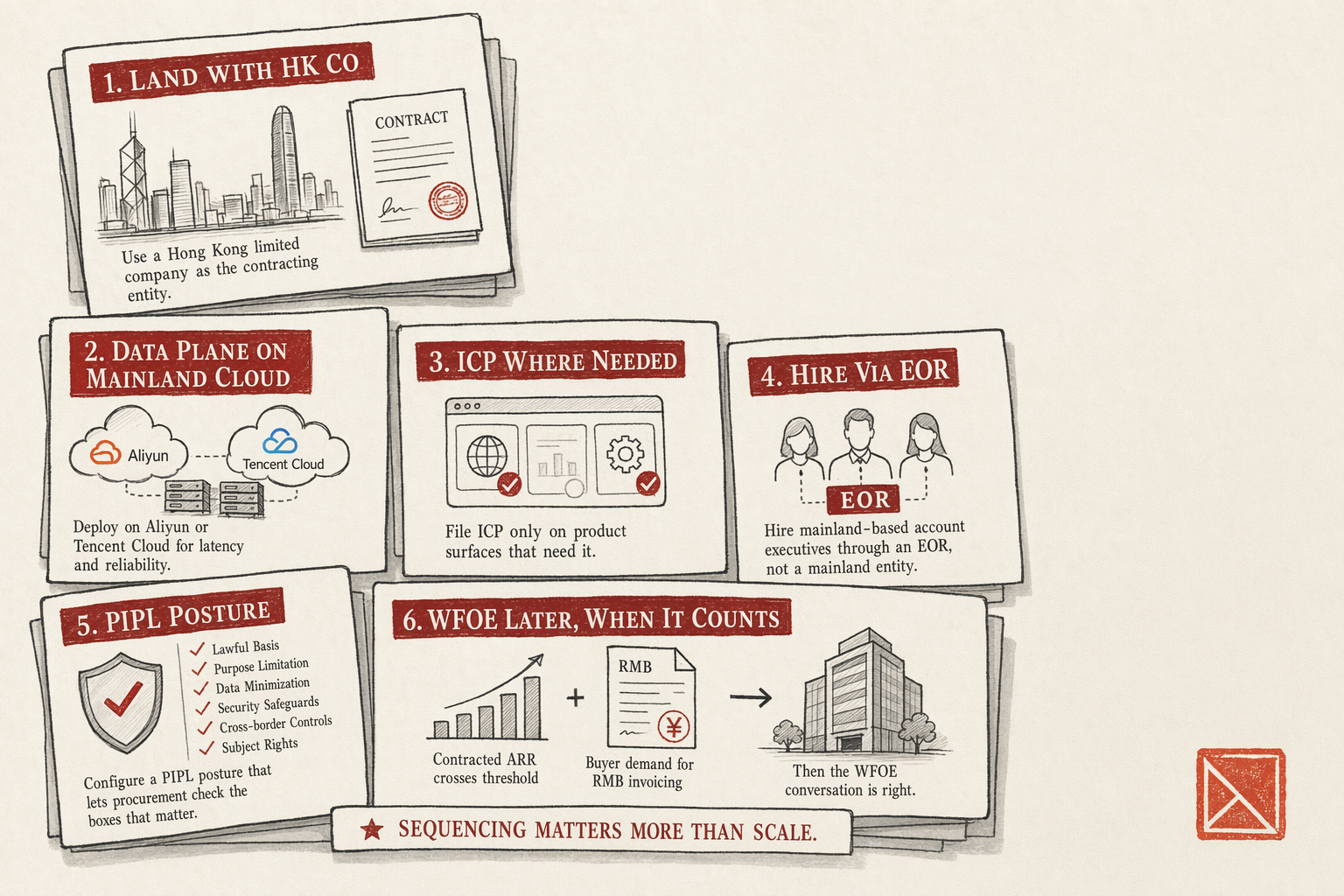

Typical entity-structure pick for SaaS — HK Ltd plus EOR is the default

The default structure for first-time B2B SaaS market entry to mainland China runs three components.

Component one — a Hong Kong limited company above the operating parent. The HK Ltd is the dedicated mainland-market contracting and invoicing entity. It contracts with mainland customers in USD (or in some cases HKD), receives payment through HKD-and-USD multi-currency accounts at a HK bank, holds the mainland-market trademark portfolio, and holds the WeChat Work tenant and ICP-sponsorship relationship. HK setup costs are typically €2,500-4,000 for incorporation and first-year fees; annual carry sits at €4,000-7,000 for a clean, lean entity. The HK layer is right for SaaS that expects mainland-attributable ARR to scale into the meaningful range; it is structurally cargo-cult for SaaS that wants to test the market with two pilot conversations and then decide.

Component two — EOR (Employer of Record) for mainland sales coverage. When mainland-domiciled buyers become a meaningful share of the pipeline, mainland-based account executives become necessary. Sponsoring those AEs through a WFOE requires the WFOE to be the right answer for the broader business, which it may not yet be. EOR is the bridge — a third-party employer of record (typically a mainland HR-services firm) sits as the legal employer of the AE, handles payroll, social-insurance contributions, housing-fund contributions, and work-permit sponsorship for non-Chinese-national AEs. The SaaS company directs the AE's work and pays the EOR a service fee on top of the salary cost. EOR fees typically run 15-25% of the AE's gross salary, which is materially less than the all-in carrying cost of a WFOE for a small team. The local-representation service hub covers the EOR mechanics in detail.

Component three — Aliyun or Tencent Cloud mainland region for the data plane. The cloud-side commitment is usage-priced, scales with traffic, and does not carry the operating-entity overhead a WFOE would. The ICP filing on the customer-facing surface is sponsored through the cloud provider's enterprise program, attached to the HK Ltd or a partner mainland entity, depending on the sponsor's specific structure. PIPL representative, Standard Contract for cross-border transfers, Chinese-language privacy policy, and MLPS Level 2 self-assessment all attach to the HK Ltd as the operating entity. None of this requires a WFOE.

The WFOE comes later. When mainland-attributable ARR crosses the threshold where the WFOE operating cost is a small share of margin, when a meaningful share of buyers wants RMB-fapiao invoicing, or when mainland-based engineering or data-handling responsibilities require a mainland legal entity for compliance reasons, the WFOE conversation becomes live. Until then, HK Ltd plus EOR plus cloud-region plus regulatory-posture stack is the right answer for most B2B SaaS.

Common rejection and stall patterns specific to SaaS

The rejection and stall patterns specific to B2B SaaS market entry to mainland China cluster around three themes.

Pattern one — the procurement-side PIPL audit. Mainland enterprise security reviews routinely include a PIPL-specific audit of the SaaS vendor's data-handling. The audit checks whether the vendor has a PIPL representative (yes/no), whether the privacy policy is in Mandarin and meets PIPL notice requirements (assessed), whether cross-border transfers have a Standard Contract (yes/no), and whether the vendor's data-residency claim is technically verifiable. SaaS companies that have not done the PIPL work in advance fail this audit at the procurement stage. The fix is to do the PIPL posture work before the first procurement security review, not in response to it. Customers do not give you a second pass.

Pattern two — ICP-sponsorship mismatch with the contracting entity. SaaS companies sometimes set up the ICP filing through a generic mainland-host sponsor without checking that the filing entity matches the contracting entity. The mismatch creates a procurement-side document chain that does not hold up: the contract is from HK Ltd, the invoice is from HK Ltd, but the ICP-filing footer on the product UI is in a different (Chinese-host-affiliated) entity name. Mainland buyers' procurement teams notice this. The fix is to use an enterprise-tier ICP-sponsor program (Aliyun and Tencent Cloud both offer one) that explicitly links the foreign operating entity to the filing in a clean documented chain, rather than the cheaper retail-tier sponsorship that hides the foreign operator behind the mainland host's umbrella in a way that is not transparent.

Pattern three — WeChat Work tenant not properly verified or not properly used. Mainland customer-success runs on WeChat Work. SaaS companies that set up a WeChat Work tenant without proper enterprise verification, or that set it up and then have the AEs continue to communicate by email, do not capture the benefit. The customer's experience defaults to “this vendor does not really communicate in our channel.” The fix is twofold: complete WeChat Work enterprise verification at the HK Ltd level (a 5-10 business day platform-side process), and operationally require the customer-facing team to use WeChat Work as the primary channel for mainland accounts. Channel of record is a discipline; if it is optional, it does not happen.

Pattern four — registered-capital and substance gaps on the HK Ltd. Some mainland procurement teams check the HK contracting entity's business-registration record. An HK Ltd that has zero employees, zero leased office space, and a sole non-resident director can fail procurement-side substance checks, particularly with SOE buyers and buyers in regulated industries. The fix is modest substance: a HK-resident director on contract (commonly provided by the company-secretary firm), a serviced HK office address (not a mail-forwarding service), and at minimum a HK-side contracting administrator or operations-manager role. The cost is low five figures USD annually; the procurement-side defensibility is materially better. The HK gateway analysis covers the substance question in depth.

The bundled engagement — sequence, indicative budget, realistic timeline

For a B2B SaaS company at the Series A-to-B scale entering the mainland market with the structure pattern above, the bundled engagement covers the following sequenced workstreams.

Phase one — entity and posture setup (weeks 1-6). HK Ltd incorporation, first-year company secretary and registered office, HK bank-account introductions (virtual bank in week 1-2, legacy bank in week 4-6), PIPL representative appointment, Chinese-language privacy policy drafting, Standard Contract execution template prepared.

Phase two — cloud and ICP (weeks 4-12). Cloud-provider selection (Aliyun, Tencent Cloud, or AWS China), enterprise-tier account opening, data-plane deployment to the mainland region (this is engineering work and runs on the SaaS team's timeline rather than the structure timeline), enterprise-tier ICP sponsorship setup, filing application, MIIT review, 30-day PSB sub-filing. ICP timeline runs roughly 18-25 business days for the MIIT review plus the 30-day PSB clock.

Phase three — communication and team (weeks 6-14). WeChat Work tenant provisioning and enterprise verification, integration with customer-success CRM, mainland-based AE recruiting (if applicable), EOR contract execution, work-permit sponsorship for non-mainland-national AEs. WeChat Work enterprise verification runs 5-10 business days; AE recruiting and work-permit sponsorship are calendar-dependent on the candidate and the visa category.

Phase four — MLPS and security posture (weeks 8-16). MLPS Level 2 self-assessment scoped, security-controls inventory mapped, documentation prepared, filing with local cybersecurity bureau. If buyer mix requires MLPS Level 3, this phase extends materially — third-party assessment, additional documentation, longer review cycles.

Indicative budget band: For a B2B SaaS at this scale, the first-year structural budget for everything above sits in the $50,000-150,000 range, depending on the scope of the cloud-side deployment, the size of the mainland sales team if any, and the specific buyer-driven MLPS level. The budget breaks down roughly as: HK Ltd setup and first-year carry $8,000-15,000; cloud and ICP setup $15,000-40,000; WeChat Work and integration $5,000-15,000; PIPL posture and Standard Contracts $5,000-15,000; MLPS Level 2 self-assessment $10,000-25,000; EOR-sponsored AEs (per-head) typically 1.15-1.25x of gross salary annually. These are indicative bands, not quotes — every engagement is scoped to the specific situation.

Realistic timeline: 14-18 weeks for a clean engagement where the SaaS team's engineering work on the cloud deployment runs on schedule and there are no candidate-recruiting delays on the AE side. Faster is possible for SaaS that can skip the mainland-AE phase (covering pilots from offshore); slower is common when the engineering work on the data-plane region split is more involved than estimated. Plan for 16 weeks; deliver in 14-22.

To stress-test the structure decision against your specific numbers, run the structure-decision matrix and the expansion-budget estimator.

Case study match — how the US Series-A SaaS landed without a WFOE

The structure pattern on this page is the same one that the US Series-A SaaS case study walks through end-to-end. A $8M-ARR US-based B2B SaaS had mainland enterprise pilots stalled on the invoicing question. The fix was Hong Kong Ltd as the contracting and invoicing entity, WeChat Work for customer-side communication, Aliyun mainland region for product latency and PIPL posture, and selective ICP filing on the product surfaces that needed mainland hosting. The two stalled pilots closed inside four weeks of go-live; mainland customer count reached 14 by the end of the first year; the WFOE conversation landed on a future quarter's board agenda when it was the right decision rather than a panicked one.

The case study covers the specific board-side dynamics that ruled out a WFOE on day one, the structure space between “full WFOE” and “pure offshore” that most founders do not realize exists, the 14-week implementation timeline, and the honest concession about what we would do differently next time (run the WeChat Work onboarding earlier and pick the Aliyun primary region based on the buyer-base geography, not the engineering team's default preference). If your SaaS company is in a similar window, the case study reads as the operational playbook.

Working in this industry?

Tell us your constraints — we'll reply with the partner firm and filing sequence that fits this niche.

Frequently asked questions

Do we need a WFOE on day one?

No. Many SaaS companies serve mainland customers from an HK Ltd or even from offshore for the first 6-12 months, then graduate to a WFOE once recurring contracts pass a board-defined threshold (commonly $1-2M ARR).

What's the PIPL minimum we need?

Appoint a PIPL representative for the mainland, publish a Chinese-language privacy policy, accept data-subject access requests in Chinese, and ensure cross-border data transfers have a Standard Contract on file. The cross-border data security assessment kicks in at higher thresholds.

Aliyun vs AWS China?

AWS China (operated by Ningxia Western Cloud Data Technology and Beijing Sinnet) works but has thinner foreign-brand customer reference base for ICP filings. Aliyun is more documentation-friendly for first-time foreign tenants.

Do you have a relevant case study?

Yes — the case-studies index lists four anonymized engagements across DTC, SaaS, industrial, and creator personas.

Or skip the form

Book a call with Mike

30 minutes, Zoom or Tencent Meeting. No discovery-call gauntlet.