Why the legal rep has to appear in person

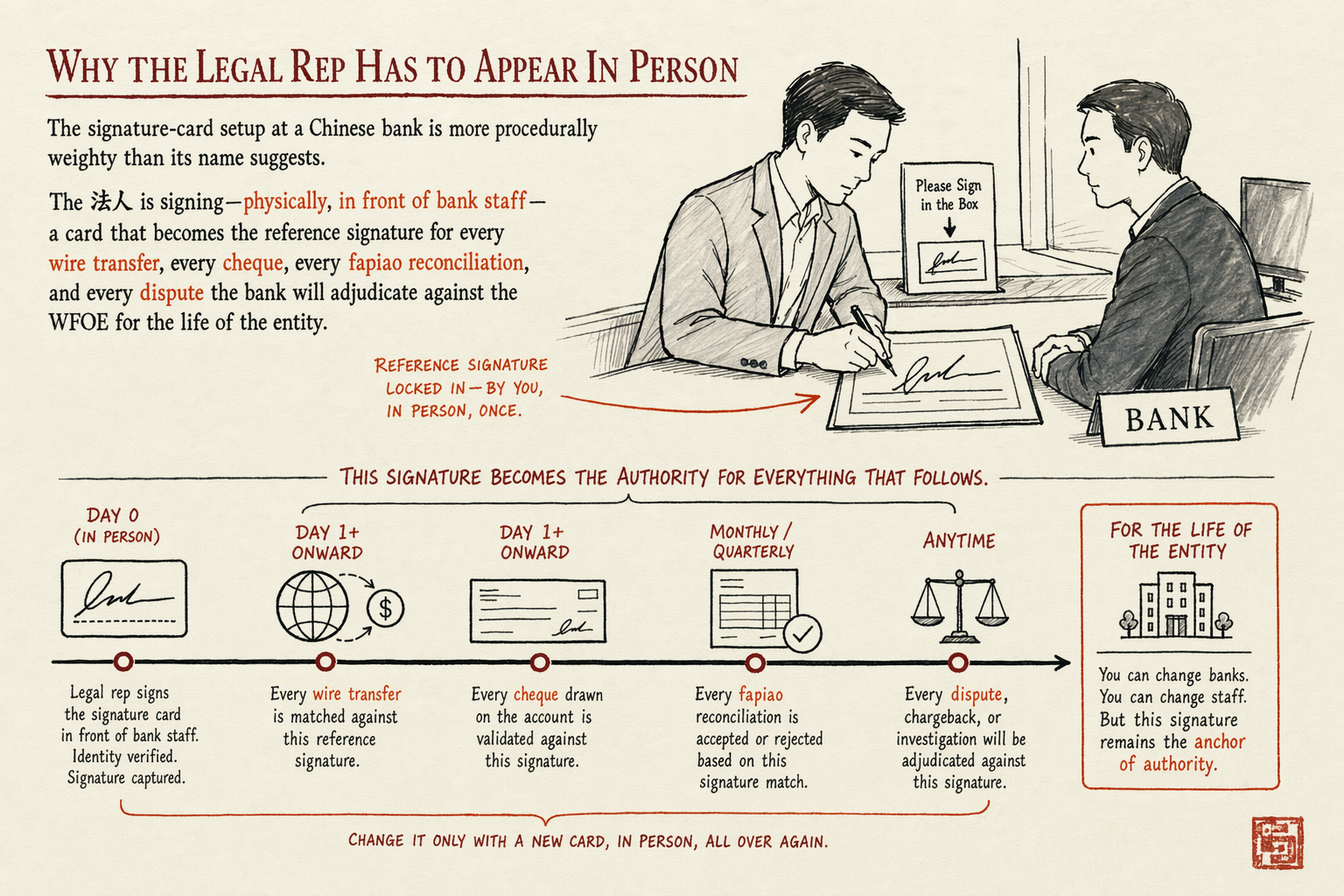

The signature-card setup at a Chinese bank is more procedurally weighty than its name suggests. The 法人 is signing — physically, in front of bank staff — a card that becomes the reference signature for every wire transfer, every cheque, every fapiao reconciliation, and every dispute the bank will adjudicate against the WFOE for the life of the entity. The signature card cannot be photocopied, faxed, scanned, or apostilled in. It has to be wet-inked at the counter, witnessed by a named bank officer, and stored with the original chops in the bank's custody.

Two PBOC regulations drive this. The Anti-Money Laundering Law of the People's Republic of China and PBOC Order No. 5 on Identification of Customers and Records of Identity Information require the entity's legal-rep identity to be verified through a face-to-face encounter at account opening. PBOC interpretive notices have softened this in narrow ways for digital banking and for face-recognition video flows, but the basic-account opening at a brick-and-mortar branch has not been carved out.

The second driver is 公章 (gōng zhāng — the company chop) custody. The bank receives the company chop, the financial chop, and a 法人 personal-name chop at the basic-account opening, and registers all three to the WFOE's bank-account profile. Chop registration is the moment the 法人 binds the entity to the bank's settlement system. Doing it remotely would create a custody-of-chop gap that the bank's compliance desk cannot reconcile.

What 'in person' actually means at the bank counter

The 法人 visit is one banking day, not a multi-week residence. Two to four hours at the chosen branch covers the full procedure. The visit deliverables:

- Signature-card setup. The 法人 signs a card in two or three places. The card stays at the bank.

- Chop registration. Company chop, financial chop, and 法人 personal chop are stamped onto bank-issued specimen forms, dated, witnessed by bank staff. The chops then leave with the WFOE; the bank keeps the specimens.

- Passport verification. The 法人 presents an original passport with a valid Chinese visa or residence permit. The bank scans both pages, attaches the scan to the file, returns the passport.

- Application form acknowledgement. The 法人 signs the basic-account application form, which has typically been pre-filled by the WFOE's accountant or by the brokering partner firm.

- Photograph at the counter. Most banks (CMB universally, ICBC at most branches, BoC at flagship branches) photograph the 法人 holding their passport beside the bank officer, time-stamped. This becomes part of the KYC file.

Operationally, the 法人 enters China on a Z-visa, an M business visa, or a regular tourist visa (the latter works for the bank visit, though it complicates downstream work-permit applications if the same 法人 is also a foreign employee). The bank visit can be scheduled for any banking day during the visa-valid stay; same-day appointments are typical at CMB, 1-2 day advance booking at ICBC and BoC.

The narrow documented exceptions

Three documented carve-outs exist. None of them remove the in-person basic-account signature-card requirement.

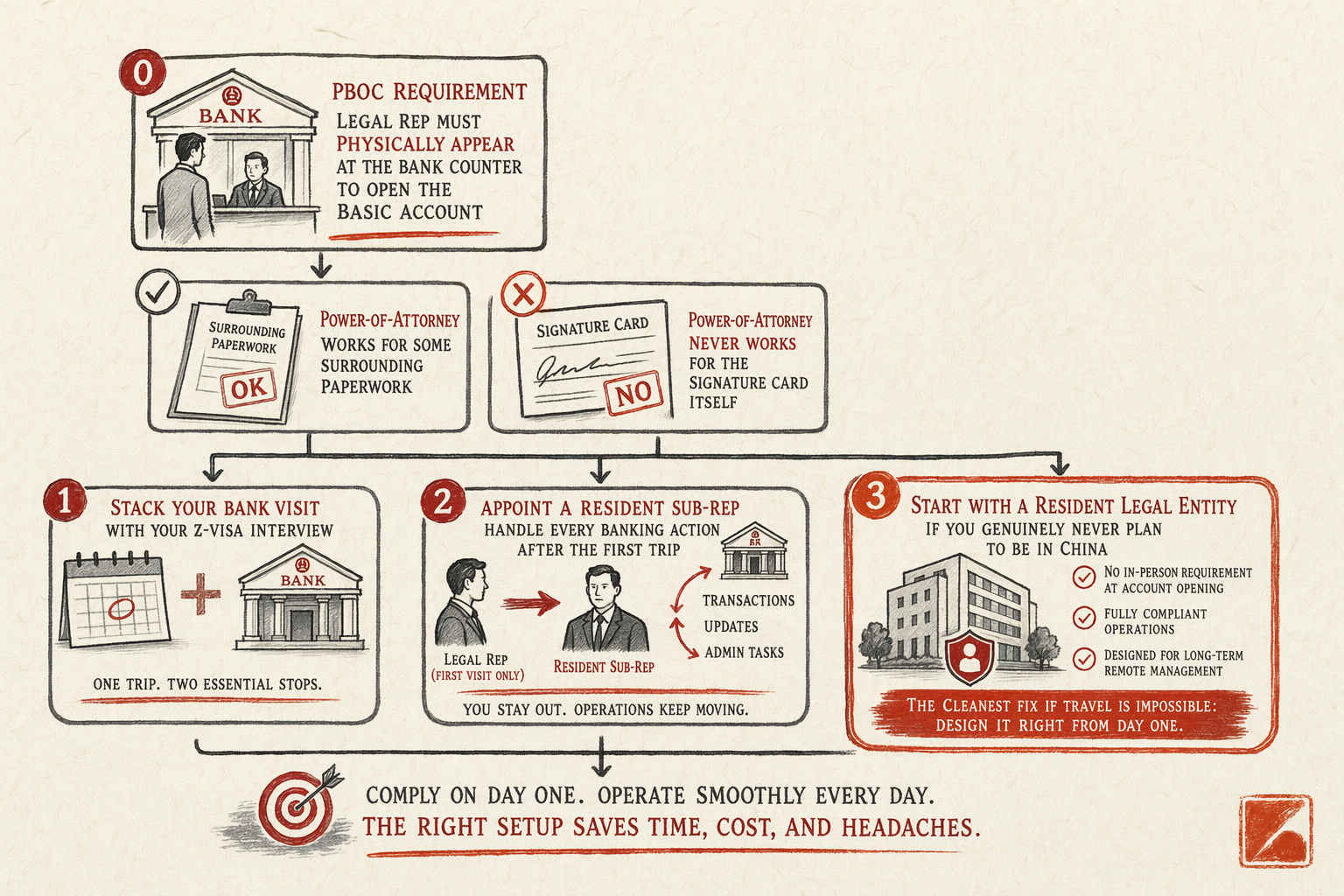

Exception 1: Power-of-attorney for non-signature-card paperwork. Some branches at all three of ICBC, BoC, and CMB accept an apostilled power-of-attorney for specific documents that flank the signature card — the application form itself, the supporting tax declarations, the chop-registration acknowledgement. The 法人 still has to appear for the signature card, but the rest of the paperwork can be pre-signed remotely. This saves a few hours of counter time, not the trip.

Exception 2: Face-recognition video opening (sub-accounts only). CMB and BoC have piloted face-recognition video sessions for adding sub-accounts and general accounts after the basic account is already open. The 法人 connects via the bank's mobile app, holds the passport to the camera, speaks pre-set verification phrases. The video session is recorded, indexed against the prior in-person KYC, and accepted as identity confirmation. This works for opening additional general accounts at the same bank after the basic is live. It has not been extended to first-time basic-account opening for any of the three banks under their current PBOC-approved protocols.

Exception 3: Banking days in Hong Kong for the HK-side accounts only. If your structure uses a Hong Kong limited company above the mainland WFOE (see HK Ltd holding mainland WFOE), the HK-side bank account opening (HSBC, Standard Chartered, ZA Bank) happens under Hong Kong banking rules, which permit a remote video meeting for some account categories. The mainland WFOE's basic account still requires the 法人 to fly to the mainland; it cannot be opened from Hong Kong.

Three workarounds for travel-restricted legal reps

Three patterns we have brokered for foreign-resident 法人 who genuinely cannot travel:

Workaround 1: Combine with a planned Z-visa or work-permit visit. If the 法人 is also the WFOE's first foreign employee, the Z-visa application requires an in-person work-permit interview at the local PSB (Public Security Bureau) entry-exit desk anyway. Stacking the bank visit on the same trip is the cleanest pattern. Two to four banking days inside one Z-visa entry covers the basic account, the general account, and the work-permit interview. Total mainland time: 5-10 days.

Workaround 2: Appoint a resident sub-rep with executive power-of-attorney. The 法人 remains the legally-named legal representative on the SAMR business license, but an apostilled executive power-of-attorney delegates day-to-day banking authority to a named mainland-resident individual. This person — often a trusted accountant, a partner from the brokering firm's network, or a local hire — holds the chops, signs operational documents, and reconciles the bank-account flows. The 法人 still has to appear at the bank for the signature-card setup, so this workaround does not skip the first trip; it skips every subsequent trip for the life of the entity. Compatible with nominee director risk-mitigation.

Workaround 3: Switch the 法人 to a resident person before account opening. The cleanest workaround if the original 法人 will not be able to travel at all. The WFOE registers initially with a resident Chinese national or a foreign passport-holder already inside China as the 法人, opens the bank account in that person's presence, and runs operations under that 法人. The original founder remains the shareholder and the ultimate beneficial owner; only the legal-representative line on the business license changes. The trade-off is non-trivial: the resident 法人 carries personal liability under PRC Company Law for the entity's actions, so the structure requires a written escrow agreement and ongoing trust between the parties. Covered in detail at escrow agreements between foreign owner and nominee.

When swapping the legal rep is simpler

For some foreign founders, particularly those who never intend to physically operate inside China, the workaround that actually fits the long-term structure is to designate a different 法人 from day one. The 法人 does not have to be the largest shareholder. The 法人 does not have to be the CEO. The 法人 has to be one named natural person who accepts the PRC Company Law liability and who can physically be at the bank counter, the AIC site inspection, and the tax-bureau interactions that crop up two to four times per year.

Three profiles work for this resident-法人 pattern:

- A senior employee already on the WFOE's first hires — typically the General Manager or the Country Lead — who relocates as one of the first two foreign hires. Z-visa, work permit, residence permit, then 法人 swap.

- A trusted Chinese-national executive hired into the General Manager role. Mainland resident from day one, no visa friction.

- A nominee director from a partner firm's panel. Lowest founder-management overhead, highest fee, requires careful liability-allocation in the engagement letter.

Swapping the 法人 after the entity already exists requires AIC filing, tax-bureau notification, social-insurance bureau update, and bank-side signature-card re-registration. The bank step alone takes 2-4 weeks. A 法人 swap initiated before the basic account is open is much cleaner than one done after; if you know the original founder cannot travel, design for a resident 法人 from day one. For the parent topic linking up to all RMB-banking articles see RMB Bank Account That Clears. For the topic on nominee risks see Nominee Director — Risks and Safeguards.

In plain English

If you only read one paragraph: PBOC requires the legal rep to physically appear at the bank counter to open the basic account. Power-of-attorney works for some surrounding paperwork but never for the signature card itself. The three real workarounds are: stack the bank visit with your Z-visa interview, appoint a resident sub-rep to handle every subsequent banking action after the first trip, or switch to a resident 法人 from day one if you genuinely never plan to be in China. The cleanest fix if travel is impossible is the third — design with a resident 法人 from the start rather than swapping later.

Related

7 min read

Opening an RMB Business Account That Actually Clears

Basic vs general account, legal-rep in-person rules, KYC red flags, cross-border FX (SAFE) registration, ICBC vs BoC vs CMB.

6 min read

RMB Basic Account vs General Account — Which First

Why the 基本户 must come first, what the general account 一般户 unlocks, and the 6-step opening sequence that minimizes downtime.