—

Time to launch

Mike's running benchmarks

—

Y1 cost band

Mike's running benchmarks

—

Outcome metric

Mike's running benchmarks

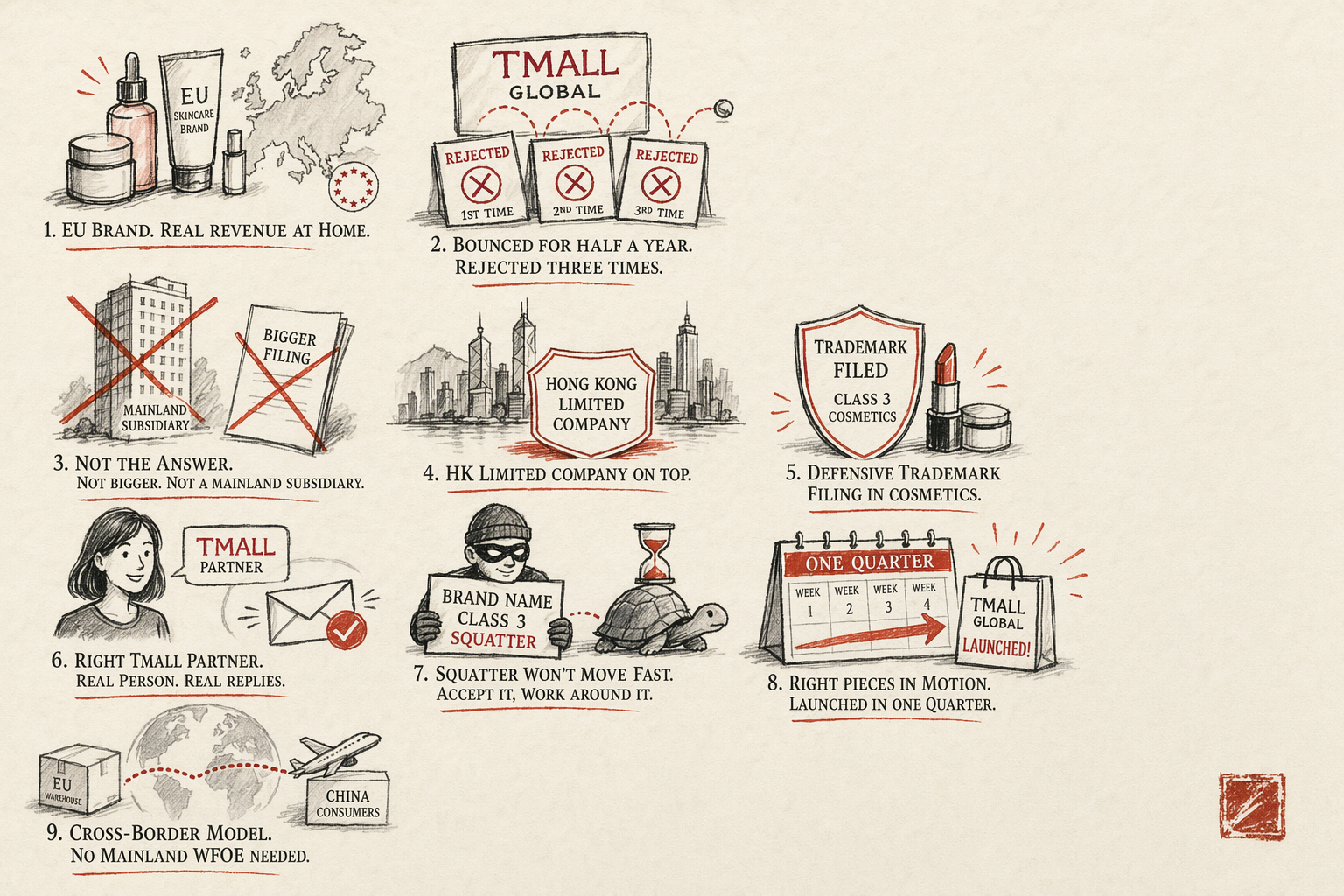

An eight-figure-euro EU skincare brand had been trying to land on Tmall Global for half a year. The founder kept hearing the same three things from the platform: trademark gap, document mismatch, sponsor confusion. Three rejection cycles in, the brand was no closer to enrollment and the European agency they had been working with was out of ideas. The fix, in the end, was not heroic. It was a Hong Kong limited company sitting above the EU operating company, a CNIPA (China National Intellectual Property Administration) defensive filing in Class 3 cosmetics, a Tmall Partner relationship with a partner who actually answered email, and a willingness to accept the trademark squatter who held the brand name in Class 3 was not going to disappear quickly.

This case study walks through what the brand looked like when they reached out, the three specific reasons their earlier attempts failed, the full-WFOE path we ruled out and why, and the structure we landed on that got them live on Tmall Global before the next quarter closed. Names, exact revenue numbers, and identifying detail are removed — the structure and the sequence are not.

The starting point — €8M GMV EU skincare brand, founder-led, no China presence

The brand was a roughly €8M GMV (Gross Merchandise Value) skincare label based in Western Europe, founder-led, with strong DTC (direct-to-consumer) traction at home and a small distribution presence in two adjacent EU countries. Year-on-year growth was solid in the home market but plateauing — the founder had identified the mainland Chinese cross-border channel as the next 18-month growth lever based on three signals: meaningful unprompted Xiaohongshu mentions in the prior six months, growing daigou (代购, personal-shopper) volume on the brand that they were not capturing margin on, and two unsolicited inbound offers from Chinese distributors that they had declined because the deals would have given up brand control.

The team was lean. Twelve people, mostly in product development, e-commerce operations, and customer service. No Mandarin speakers on staff. No prior experience with mainland Chinese platforms beyond the founder having spent a few weeks in Shanghai years earlier. The plan, before they reached out, had been to engage a European agency that advertised “China expansion” services to handle the Tmall Global setup end to end. That agency had been on the project for roughly six months. The brand had paid them mid-five-figures EUR. They had received three Tmall rejection notices and no clear explanation of why.

The brand's working theory when they reached out was that the rejections were unfortunate but solvable with more paperwork. The actual problem was structural: the agency had been trying to enroll a European operating company directly with the Tmall Global Partner network, the brand's trademark in mainland China had been registered by someone else in 2021, and the document chain — apostilled certificates of incorporation, brand-authorization letters, EU VAT numbers — was being submitted in formats that the Tmall enrollment team's reviewers were not used to seeing on cosmetic-brand applications. None of those problems were going to fix themselves with another submission.

The blockers — three Tmall Global rejection cycles in a single quarter

The three rejection cycles, in order, broke down like this.

The first rejection cited a trademark gap. The reviewer's note pointed to a 2021 CNIPA filing held by a third party in Class 3 (cosmetics, the relevant class for skincare). The brand's European trademark, registered through EUIPO in the home market for over a decade, was treated as not relevant to the mainland application. The founder's first reaction was that this had to be a misunderstanding — the brand existed in Europe long before the squatter's 2021 filing. That reaction is common and understandable. It is also wrong. First-to-file jurisdictions like mainland China give priority to whoever lodged the paperwork first within their borders, regardless of how long the brand existed elsewhere. The squatter's 2021 filing was, on the face of the CNIPA register, the senior mark in mainland China. The agency tried to argue around this on the second submission and lost the argument.

The second rejection cited document mismatch. The brand's certificate of incorporation, apostilled in the home country, had been translated by the agency's translator into Chinese characters using a brand-name transliteration that did not match the brand-name transliteration on the brand-authorization letter. Tmall's reviewers cross-check transliterations across the document chain. When they fail to match, the application stalls. The agency resubmitted with corrected transliterations on the third attempt.

The third rejection cited the wrong store-type classification. The agency had submitted the application as an overseas-brand official store (海外旗舰店), which has the strictest documentation requirements and the highest scrutiny on trademark provenance. With the squatter still holding the senior Class 3 mark, the official-store path was effectively closed. The reviewer suggested the brand reconsider the store-type election and reapply. The agency, at this point, ran out of ideas and the founder asked for outside help.

Three rejections in a single quarter is not unusual on first-time Tmall Global cosmetic-brand enrollments where the agency does not know the platform's evidentiary preferences and the trademark layer was not cleared in advance. Every one of these problems was visible from the trademark register and the public documentation requirements before the first submission. Nobody had looked.

What we ruled out — full WFOE and the mainland flagship route

The first thing many founders look at when their cross-border attempt has stalled is the obvious bigger structure: just incorporate a WFOE (Wholly Foreign-Owned Enterprise, the 100%-foreign-owned mainland entity), get a mainland Tmall flagship, and have all the platform options. We ruled this out fast and in writing, for four reasons.

One — the brand's revenue model did not need a WFOE. Cross-border bonded-warehouse sales on Tmall Global, JD Worldwide, and Douyin Global are explicitly designed for overseas brands without a mainland entity. The product ships in bulk from the overseas warehouse to a bonded zone, customs-cleared individually by parcel at the time of purchase, with the consumer paying the per-parcel duty as part of checkout. The brand's product mix sat comfortably under the per-parcel duty thresholds. There was no commercial reason to be a mainland-domestic seller.

Two — the regulatory floor on a mainland-domestic cosmetic store is materially higher. NMPA (National Medical Products Administration) registration is required for cosmetics sold through a domestic-mainland flagship, not just on Tmall Global cross-border. NMPA filing for general cosmetics is currently 6-18 months; for special-use cosmetics (whitening, anti-aging claims, sunscreen) it is 12-30 months and may require new safety testing. The brand had three SKUs that would have triggered the special-use bucket. Going domestic would have moved the launch out of the current calendar year and possibly the next one.

Three — the WFOE adds ongoing operating cost the brand did not need. A real mainland WFOE means RMB bookkeeping, monthly tax filings, social-insurance and housing-fund (五险一金) registration for any mainland employees, annual audits, real-estate registration for the office, and an active legal representative with personal exposure. That is meaningful overhead before a single product moves. The cross-border model carries effectively zero of that overhead — the platform handles customs and fapiao, the brand stays in its home jurisdiction for accounting.

Four — the squatter problem does not magically resolve with a WFOE. Even if the brand had a mainland WFOE, the senior Class 3 trademark still belonged to the squatter. Going domestic would not have unblocked the trademark issue; it would have made the trademark issue more acute, because a domestic flagship inspects trademark provenance more carefully than a cross-border enrollment does.

The decision matrix made the call obvious. Cross-border on Tmall Global was the correct channel. The structure question was not WFOE-or-not. It was what overlay above the EU operating entity would clean up the document chain at the Tmall Partner level and unblock the trademark.

The actual fix — HK-Ltd structure plus CNIPA Class-3 defensive filing

The structure we landed on had four moving parts, layered in a specific order so each unlocked the next.

Part one — a Hong Kong limited company sitting above the EU operating entity. The HK Ltd was not strictly required for Tmall Global cross-border in 2026 — overseas operating entities are accepted — but the HK overlay solved three real frictions. First, HK certificates of incorporation, business-registration certificates, and notarial certifications are formats Tmall's Partner reviewers see every day, which removed the “unfamiliar document” rejection class. Second, HK gave the brand a clean bilingual entity name (English and traditional Chinese characters) that the brand-authorization chain could be issued under in a way that matched Tmall's transliteration norms. Third, the HK layer became the holding vehicle for the mainland trademark portfolio, which was a clean separation from the operating company's brand asset register at home. The HK formation cost was modest — under €3,000 all-in for incorporation, first-year secretary and registered office, and bank-introduction work.

Part two — a CNIPA defensive filing in Class 3 (cosmetics) plus Class 35 (advertising, retail services). The squatter's senior mark in Class 3 still existed and was not going to be removable inside the launch window. What we could do was lodge defensive filings in Class 3 (covering all sub-classes adjacent to the squatter's narrower coverage) and Class 35, and simultaneously file a three-year non-use cancellation action against the squatter's 2021 mark. The defensive filings gave the brand a CNIPA-issued filing receipt within five weeks, which is what Tmall actually accepts at enrollment. The non-use cancellation is a parallel track that may take 14-18 months to resolve, but the launch did not depend on it resolving — only on the defensive filings landing.

Part three — a working relationship with a Tmall Partner (TP). Tmall Partners are accredited third-party operating agencies who handle store setup, customer service, and platform operations on behalf of overseas brands. Selecting a TP is not just a vendor choice. Different TPs specialize in different categories, have different reviewer relationships, and have different fee structures. We identified three category-appropriate TPs, briefed them on the brand's situation including the prior rejections and the squatter problem, and ran a selection process. The chosen TP had operated four comparable cosmetic-brand cross-border launches in the prior year, had a working file format that Tmall's reviewers were used to, and was willing to handle the brand-authorization chain end to end. Their fee was a percentage of platform GMV with a modest setup component — the model the brand preferred to a large upfront retainer.

Part four — the actual Tmall Global enrollment package, resubmitted clean. With HK in place, the defensive filing receipts in hand, and the TP managing the submission, the enrollment package was re-prepared from scratch. The brand-authorization chain ran from the HK Ltd (trademark holder, on filing receipts) to the EU operating entity (product source) to the TP (operator). All transliterations matched. All certificates were apostilled and translated by the TP's preferred translation desk. The store-type election shifted from official store to overseas brand store, which was achievable inside the trademark constraints.

The submission cleared review on the first attempt under the new structure.

The result — live before the next quarter closed

From the moment the HK Ltd was incorporated to the moment the brand's Tmall Global storefront opened to consumers, the timeline ran roughly 14 weeks. The breakdown:

- Weeks 1-3: HK Ltd incorporation, first-year secretary and registered office in place, HKD and USD bank accounts opened with a virtual bank for working capital and a legacy HK bank for cross-border settlement.

- Weeks 2-7: CNIPA defensive filings in Class 3 and Class 35 lodged. Three-year non-use cancellation action against the squatter's senior mark filed in parallel. Filing receipts issued in week 5 and week 6 respectively.

- Weeks 4-6: Tmall Partner selection process. Three TPs evaluated. Engagement letter signed in week 6.

- Weeks 6-10: Brand-authorization documentation chain re-prepared with the TP. Product images, copy, and ingredient lists localized for Chinese platform norms. Brand-authorization letters issued from HK Ltd downstream.

- Weeks 10-12: Tmall Global enrollment submission. First-pass clearance on the trademark gate, document-chain gate, and store-type gate.

- Weeks 12-14: Store-build phase. Visual design, category configuration, payment-and-logistics setup, customer-service playbook. Bonded-warehouse inventory positioned in Hangzhou.

- Week 14: Live to consumers.

First-year results, with the caveat that one founder's numbers do not generalize: the brand cleared mid-seven-figures RMB GMV in the first 12 months on Tmall Global, with cross-border duty and platform fees netting them gross margin that was within 4 percentage points of their home-market DTC margin. The daigou volume that had been on the brand pre-launch consolidated meaningfully into the official store — the daigou operators continued to exist but most consumer-direct buyers migrated, which the brand had wanted. The Xiaohongshu organic mentions that had originally signaled the demand turned into a paid KOC (Key Opinion Consumer) program in year two, but the launch did not depend on that.

The three-year non-use cancellation against the squatter resolved in their favor 16 months after the launch. By that point the brand's own active marks in Class 3 had progressed toward certificate. The brand never paid the squatter.

The lesson for the next EU beauty founder reading this

If you are an EU or US skincare or cosmetic founder thinking about mainland Chinese cross-border, the generalizable lesson from this engagement is shorter than the case study itself. It runs to four points.

One — clear the trademark register before you do anything else. Run a CNIPA search on your brand name and any common transliterations in Class 3 and Class 35 before you commit any other budget to the project. A trademark squatter holding your senior mark is the single most common reason cosmetic-brand Tmall Global enrollments stall. The trademark-squatting scanner is the cheap diagnostic for this. If the register is clear, file your own marks defensively in Class 3 and Class 35 immediately. If it is not, get help with the cancellation strategy before you do anything else.

Two — the cross-border model is built for you. Do not get talked into a WFOE you do not need. Cross-border Tmall Global, JD Worldwide, and Douyin Global exist specifically for overseas brands without mainland entities. Unless you have a specific reason that requires a domestic flagship — an SKU that cannot ship cross-border, a category-restricted positioning, a partner network that requires local invoicing — the cross-border model is faster, cheaper, and lower-risk. Agencies who pitch you a WFOE on day one are often selling their own services, not solving your problem.

Three — a Hong Kong layer above your operating entity is often worth its modest cost. HK incorporation is under €3,000 all-in. The annual carrying cost is €4,000-7,000 if you keep it lean. What you get is a clean bilingual brand entity, document formats Tmall's reviewers see daily, and a holding vehicle for your mainland trademark portfolio that keeps it cleanly separated from your home-country brand asset register. When the HK layer is worth it and when it is not is the longer read on the trade-off.

Four — your Tmall Partner is a strategic choice, not a vendor choice. Different TPs specialize in different categories and have different relationships with Tmall's reviewers. Run an actual selection process. Brief candidates on your situation including any prior rejections. Ask for references from two recent cosmetic-brand launches. Read the engagement letter carefully — TP fees can range from a flat retainer to a percentage of GMV to a hybrid, and the right model depends on your expected scale and how much in-house operating capacity you have.

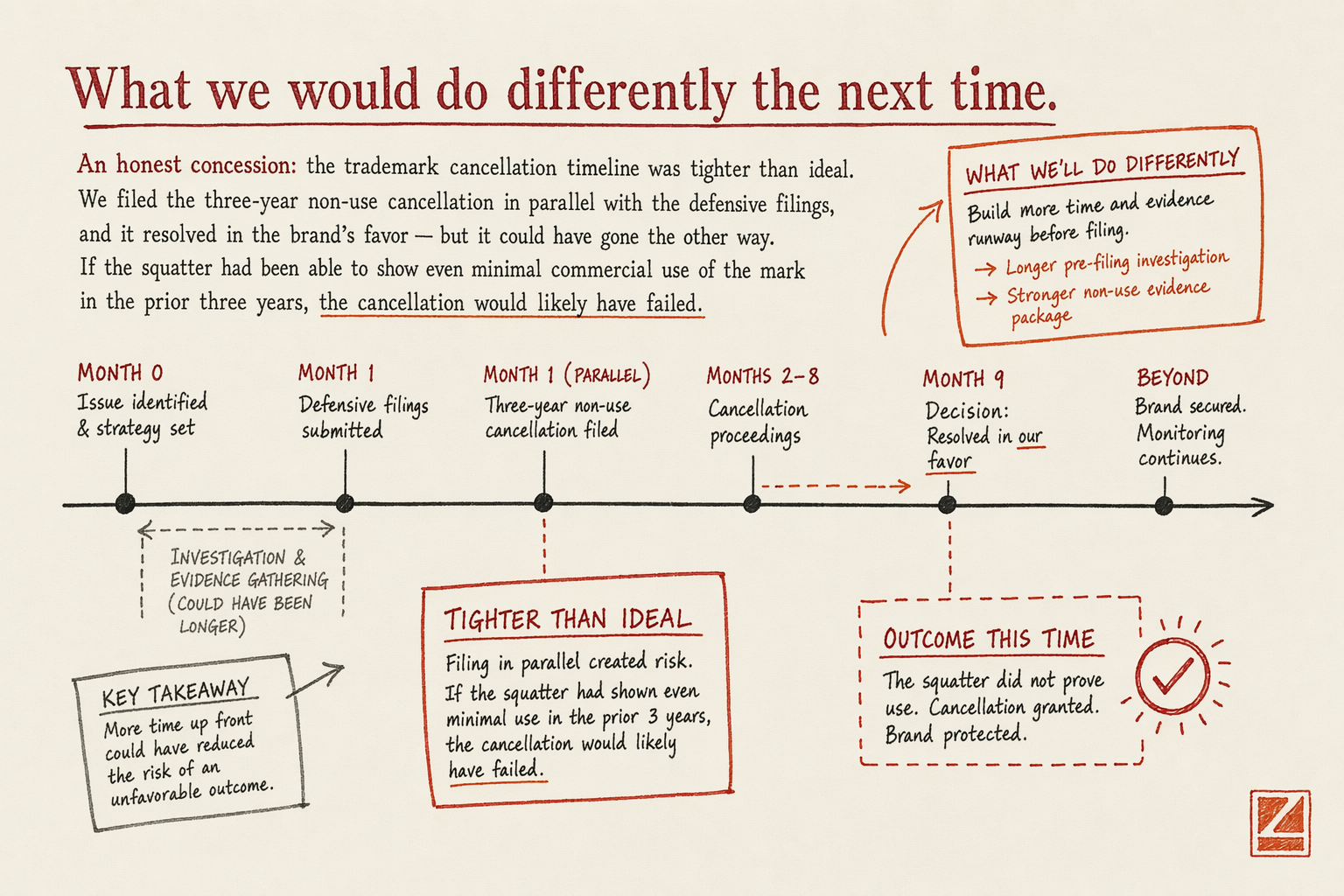

What we would do differently the next time

An honest concession: the trademark cancellation timeline was tighter than ideal. We filed the three-year non-use cancellation in parallel with the defensive filings, and it resolved in the brand's favor — but it could have gone the other way. If the squatter had been able to show even minimal commercial use of the mark in the prior three years, the cancellation would have failed, and the brand would have been operating with defensive filings in Class 3 sub-classes adjacent to the squatter's holding, rather than with a clean Class 3 register. Operationally that would still have worked for Tmall enrollment, but it would have meant ongoing risk of the squatter contesting the brand's marketing once it reached scale.

What we would do differently: commission a deeper use-evidence investigation against the squatter's mark before filing the cancellation, so the cancellation is filed only when the use-evidence record is genuinely thin. That investigation runs $2,000-4,000 and adds 3-4 weeks to the prep. It would have moved the launch back a month. In exchange, the cancellation success probability would have been much closer to certain. On a project of this scale, that is a trade worth taking.

The other small concession: we underestimated the Xiaohongshu organic-mention base the brand already had. The KOC program got started in year two, but the data we had at launch suggested it should have been live in month three. The seed-content velocity was the bottleneck — the brand's home-country creative team was not set up to ship China-tuned content at the cadence Xiaohongshu rewards, and the localization team was added late. Build the Xiaohongshu content layer earlier next time, even if it is small.

RELATED READING

Compare this engagement's structure decision to the US SaaS company that also avoided a WFOE through HK invoicing — different vertical, similar structural pattern. For the broader vertical view, the cross-border e-commerce industry page covers platform selection across Tmall Global, JD Worldwide, and Douyin Global. To stress-test your own brand's trademark exposure, run the trademark-squatting scanner against your name and adjacent transliterations.