Industry view

China Entity Setup for Industrial Manufacturers and Trade

Trading WFOE, import/export license, fapiao for customs, VAT-refund mechanics, FTZ vs non-FTZ for export-heavy operations.

Email Mike—

Y1 cost band

Mike's running benchmarks

—

Time to first revenue

Mike's running benchmarks

—

Common pivot at month 12

Mike's running benchmarks

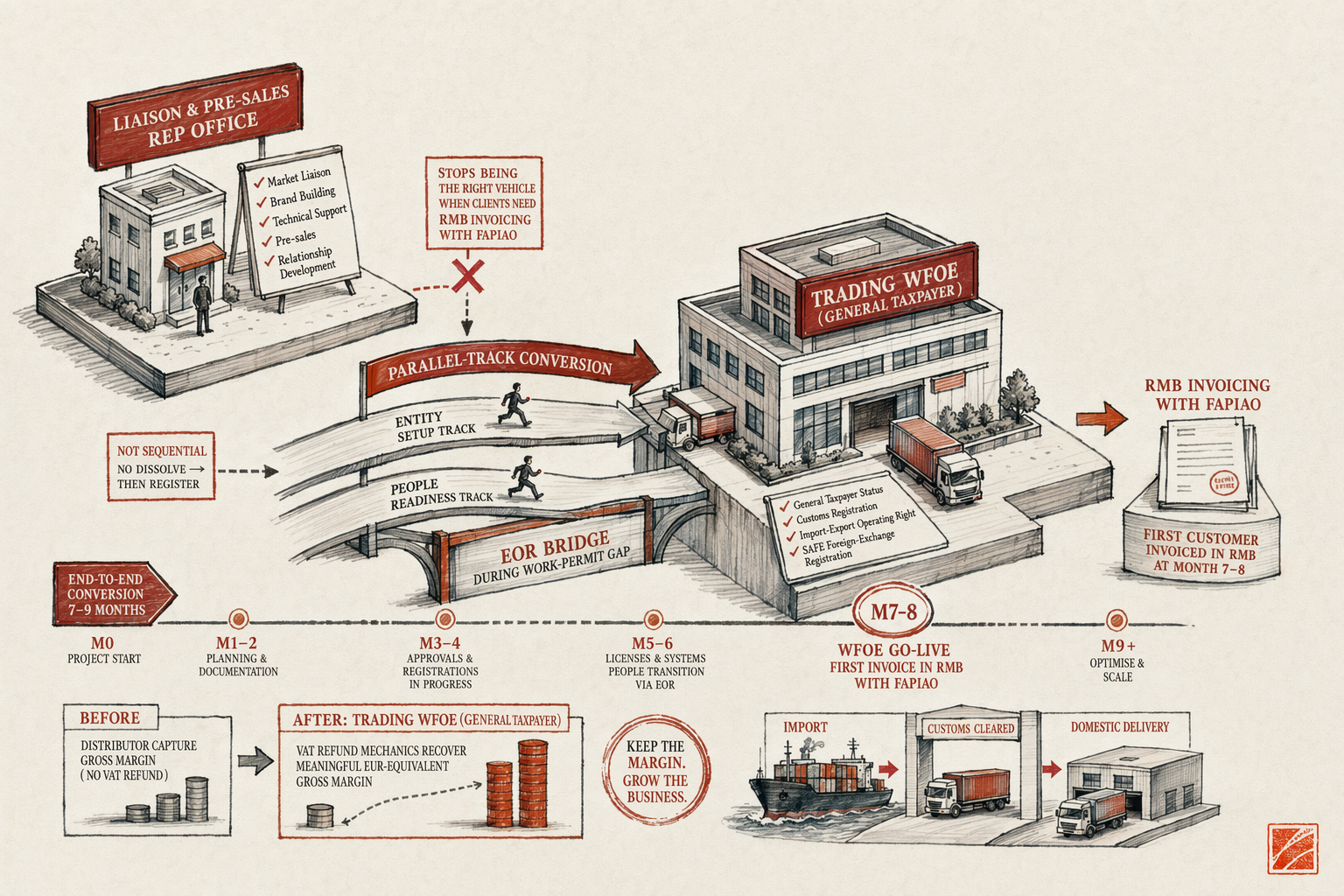

Foreign industrial manufacturers and trading businesses face a structural decision that does not apply to SaaS, cosmetics, or creators: the customers want fapiao, and a Rep Office cannot issue one. Sooner or later — usually when the largest mainland customer's procurement team standardizes on direct invoicing — the Rep Office model runs out of road. The replacement structure is a trading WFOE registered as a general taxpayer, with customs registration, import-export operating right, and SAFE registration in place. This is the heaviest entity stack of any of the asset-lead verticals, and it carries the longest realistic timeline. It also unlocks the most operational capability — direct fapiao, customs-recoverable VAT, in-name signed sales contracts, and the regulatory standing to grow into mainland operations of any scale.

This page walks through what industrial manufacturers and trading businesses typically need, the customs and trade regulatory layer specific to this vertical, the trading-WFOE structural pattern, the rejection-and-stall patterns we see in conversion and registration, and the realistic timeline and budget for a sequenced conversion engagement. If you run an industrial-products business with mainland customers asking for fapiao, the content below is the operational map for moving from RO (or no entity) to direct trade.

What industrial manufacturers and trade businesses typically need

The operational ask from an industrial-trade mainland-market establishment tends to cluster into five categories.

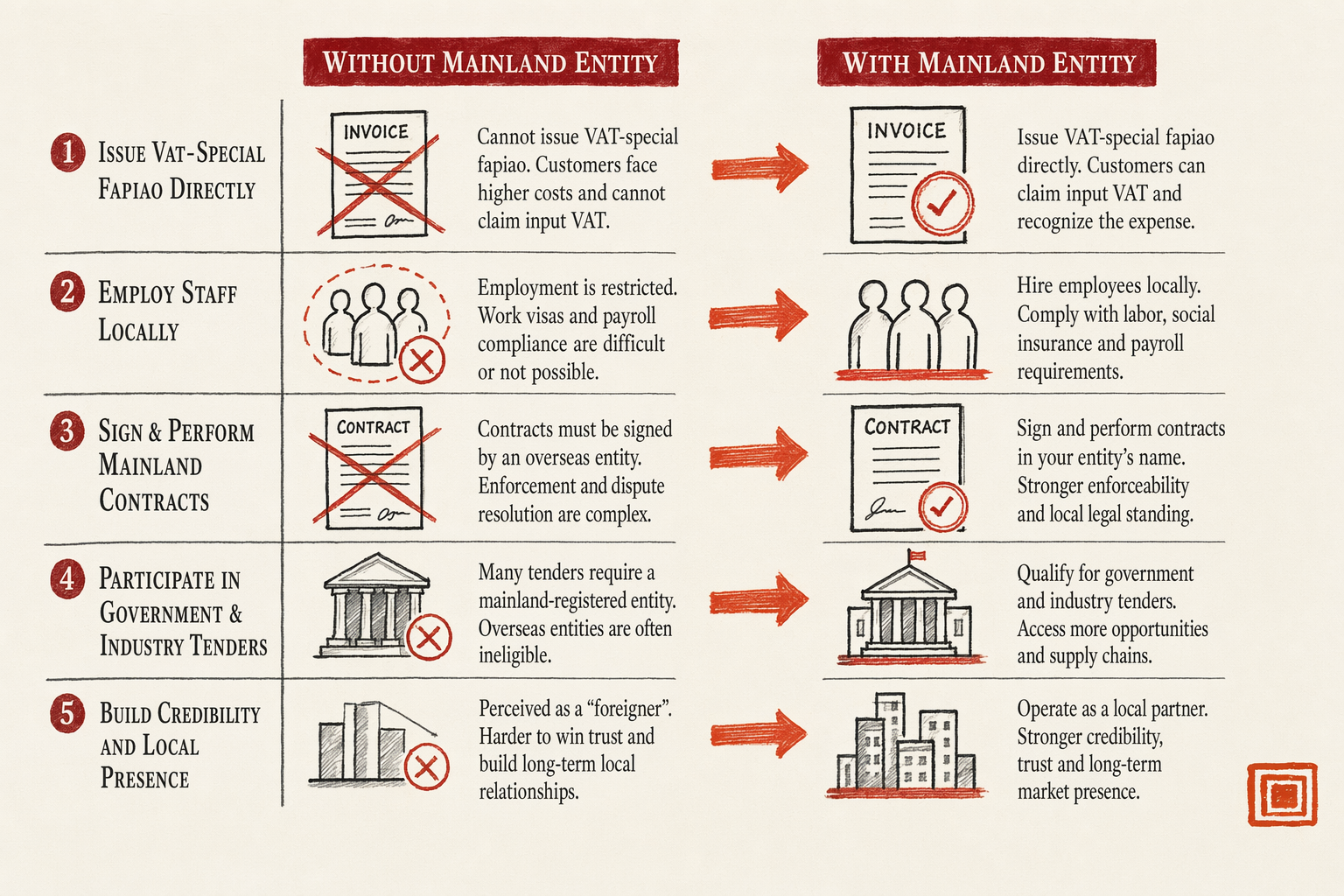

One — the ability to issue VAT-special fapiao (增值税专用发票) directly to mainland B2B customers. This is the single most common trigger for the structural conversation. Mainland enterprise AP teams require fapiao to recognize the purchase as a cost item for their own tax purposes, and they require VAT-special fapiao specifically (rather than the lighter VAT-general fapiao) to credit the input VAT on their purchase against their output VAT. Only mainland-registered general-taxpayer entities can issue VAT-special fapiao. Rep Offices, foreign operating companies, and HK Ltd companies cannot — only a mainland WFOE registered as a general taxpayer can.

Two — the ability to register as importer of record and recover input VAT on imports. When imported finished goods enter the mainland, the importer pays import duty and import VAT to mainland Customs. If the importer is the WFOE and the WFOE is a general taxpayer, the import VAT becomes an input-VAT credit that can be netted against output VAT on domestic sales, with the net excess refundable as cash on export-heavy months. If the importer is a customer or a distributor, the input-VAT credit lives in the customer's or distributor's books, not the brand's. Capturing the VAT-refund mechanics on the brand-owned WFOE is one of the largest commercial benefits of the conversion.

Three — the legal capacity to sign sales contracts directly in the WFOE's name. Mainland Chinese contract law gives substantive weight to the contracting entity. A sales contract signed by a foreign parent company on behalf of mainland delivery is enforceable but operationally awkward — the contracting party is in a different jurisdiction, dispute-resolution defaults to a foreign forum or to PRC arbitration with cross-border complications, and the customer's procurement records show an offshore counterparty rather than a mainland one. A WFOE that signs contracts in its own name removes all of that friction.

Four — staff continuity through the transition and beyond. Industrial businesses typically have mainland-based staff — customer-facing engineers, field service technicians, sales managers, finance liaisons. Work-permit sponsorship for non-mainland-national staff has to live in a mainland legal entity. The Rep Office sponsors the work permits in the pre-conversion state. After conversion, the WFOE sponsors them. The transition has to manage the work-permit chain carefully — work permits cannot transfer between entities and must be cancelled and reapplied. Bridge through an EOR (Employer of Record) for the 2-4 week window when neither entity can cleanly sponsor.

Five — banking infrastructure for RMB collection, FX conversion, and capital injection. A general-taxpayer WFOE needs an RMB business account for domestic sales receipts and an FX capital account (registered with SAFE) for inbound capital and dividend repatriation. Account opening requires the legal representative's in-person attendance for the major mainland banks (ICBC, BoC, CMB, CCB). The chops (公章, 财务章, etc) have to be carved and registered before the account-opening visit. Plan the legal-rep visit calendar carefully — it is the bottleneck on banking timing.

The vertical's specific regulatory layer — customs, HS codes, import/export operating right

Beyond the generic entity work, industrial and trade businesses face four vertical-specific regulatory regimes.

Customs registration (海关注册). An entity that will be the importer or exporter of record in mainland China must be registered with mainland Customs under a customs-registration certificate. The registration is a separate administrative step after the business-license issuance, requiring a customs-declaration agent on file, a declared scope of goods categories under specific HS codes, and the legal representative's identity documentation. Customs registration takes 4-8 weeks from application and is required before the first shipment can clear.

HS-code classification (海关编码). The Harmonized System (HS) is the international goods-classification system, with mainland Customs using a 10-digit extension of the 6-digit international HS code. Every shipment must declare an HS code, which determines the import-duty rate, the import-VAT rate, any inspection requirements, and whether the goods are subject to import licensing or quota. For industrial products this classification is non-trivial — precision parts, machinery components, and specialty industrial goods often have multiple defensible classifications with different duty implications. Customs misclassification carries financial penalties that compound across shipments. The pre-conversion best practice is to map the full product catalog to correct HS codes during the project's diligence phase, before the first shipment ships.

Import-export operating right (进出口经营权). Separate from customs registration, the entity must register the import-export operating right with the Ministry of Commerce (MOFCOM, 商务部) through the local commerce-bureau filing. This is the administrative permission to engage in import-export trade as a business activity. The filing is straightforward for properly-scoped trading WFOEs, but it is a distinct step running 4-6 weeks. Without this, the entity cannot legally engage in import-export trade even if customs registration is complete.

SAFE foreign-exchange registration. Capital flows into and out of the mainland WFOE are governed by SAFE (State Administration of Foreign Exchange, 外汇管理局). The WFOE's registered capital must be paid in through an FX capital account that is SAFE-registered. Ongoing FX conversions (RMB sales proceeds converting to USD or EUR for dividend repatriation, or USD/EUR converting to RMB for working capital injection) require SAFE-authorized banking channels and documentation. Failure to register or to follow the SAFE rules can result in capital being trapped in the mainland or in administrative penalties. The SAFE registrations are typically handled by the WFOE's banking partners as part of account-opening, but the legal rep needs to understand the framework.

Typical entity-structure pick — trading WFOE for direct sales and fapiao

The default structure for foreign industrial-product and trading businesses graduating from Rep Office (or from a distributor-only model) to direct mainland sales runs the following stack.

Component one — a trading WFOE registered in an appropriate jurisdiction. Shanghai, Beijing, Shenzhen, Guangzhou, and the Free Trade Zones are the most common WFOE-registration locations for trading entities. The choice depends on customer-base geography, supply-chain logistics, and any sub-sector-specific local incentives. Shanghai is the default for businesses with northern and central-coast customer concentration. Shenzhen and Guangzhou for southern customer concentration and Hong Kong-adjacent supply chains. Beijing for businesses with strong SOE-buyer profiles or government-sector exposure. FTZ jurisdictions (Shanghai FTZ, Shenzhen Qianhai, Tianjin, others) for export-heavy or re-export trading models. Registered capital should be sized to actual working-capital needs, not artificially inflated — see realistic WFOE registered capital for 2026.

Component two — general-taxpayer (一般纳税人) VAT status. The WFOE defaults to small-scale-taxpayer status at incorporation. The general-taxpayer application is a separate post-incorporation filing, typically lodged in weeks 16-18 after the business license issues and approved in weeks 20-24. General-taxpayer status is operationally non-negotiable for a trading WFOE — only general-taxpayer entities can issue VAT-special fapiao and recover input VAT. The application requires evidence of the business's qualifying scale (typically the WFOE attests to expected qualifying revenue), accounting-system readiness, and a registered fapiao printer.

Component three — customs and import-export registration stack. Customs registration, import-export operating right, and SAFE FX registration, all as discussed above. These are administrative-track workstreams that run partly in parallel with the WFOE business-license issuance and partly sequential to it. Plan for 8-12 weeks of post-business-license work before the WFOE is structurally complete to operate as an importer-of-record with general-taxpayer VAT status.

Component four — work-permit sponsorship for mainland staff. Work-permit sponsorship can begin once the WFOE has its business license. For businesses converting from a Rep Office, the EOR bridge during the work-permit reapplication window keeps the staff continuously employed and visa-compliant. For businesses starting fresh without prior mainland staff, this component activates at the moment the first mainland hire is ready to start. The local-representation service hub covers the EOR mechanics.

Optional layer — a Hong Kong limited company above the WFOE. The HK Ltd as the WFOE's parent (with the foreign operating company sitting above the HK Ltd) is the layer that unlocks the 5% dividend-withholding treaty rate under the HK-PRC tax treaty (versus the 10% standard rate). For mainland-attributable dividend flows above $200-300k annually, the HK layer pays for itself. Below that, the HK layer is structural overhead the business may not need. The HK gateway analysis covers the trade-off in detail.

Common rejection patterns specific to industrial and trade businesses

The rejection and stall patterns specific to industrial-trade mainland-market establishment cluster around four themes.

Pattern one — HS-code misclassification penalty after the first audit. The WFOE imports under HS codes the catalog was classified to during onboarding, and a subsequent customs audit (typical: 12-24 months after operations begin) identifies that one or more product families have been declared under codes with too-low import duty. The penalty assessment covers the duty differential plus a multiple plus administrative costs, sometimes running into six-figures EUR for high-volume traders. The fix is the pre-conversion classification analysis — work with a customs declarant who specializes in your category to map the catalog correctly, and accept that some products may belong in higher-duty codes than the commercial team would prefer. Getting the classification right before the first shipment is much cheaper than fixing it after the audit.

Pattern two — general-taxpayer application stalled on accounting-system readiness. The general-taxpayer application requires the WFOE to demonstrate accounting-system readiness to issue and track VAT-special fapiao. New WFOEs that have not yet set up a proper mainland accounting system, or that are running the books offshore through the parent company's ERP, can have their general-taxpayer application stalled or rejected. The fix is to set up the mainland accounting system at the same time as the business-license registration, not after. Most local accounting partners will provide a Kingdee, Yonyou, or SAP-mainland-localization-compliant book setup as part of their onboarding.

Pattern three — work-permit gap during the RO-to-WFOE conversion. The Rep Office sponsors work permits for the staff during the pre-conversion state. When the RO begins dissolution and the WFOE has not yet been issued a business license, the work-permit sponsorship chain becomes fragile. Staff whose work permits expire during this window face renewal-rejection risk because the sponsoring entity is mid-dissolution. The fix is the EOR bridge, as discussed in the German manufacturer case study. Some advisors will tell you to time the conversion perfectly so no EOR is needed; in practice the timing has too many moving pieces (tax-clearance dates, business-license issuance, work-permit-renewal dates) and the EOR bridge for 2-4 weeks is the cleaner risk position. Plan for it.

Pattern four — chop custody and legal-rep exposure misjudgment. The mainland chop (公章) is a binding instrument under PRC contract law — possession of the chop equals capacity to sign on behalf of the entity. The legal representative (法定代表人, 法人) bears personal liability for the entity's contractual and regulatory obligations under PRC law. Foreign businesses sometimes treat the chop and the legal-rep role as administrative formalities and discover later that they have given chop custody to a local partner without proper controls, or that the named legal rep has personal exposure they did not understand. The fix is to install proper chop-custody controls (locked storage, dual-signature usage logs, video-recorded use for high-stakes transactions) and to brief the legal rep fully on the role's exposure before they accept it. The legal-rep liability article covers what is and is not on the legal rep's plate.

The bundled engagement — sequence, indicative budget, realistic timeline

For a foreign industrial-products business at mid-eight-figures EUR annual revenue converting from Rep Office to trading WFOE, the bundled engagement covers these sequenced workstreams.

Phase one — diligence and decision (weeks 1-4). Confirm trading-WFOE versus manufacturing-WFOE scope. HS-code classification analysis on the existing product catalog. Customs-duty impact modeling against current and projected revenue. Jurisdiction selection (Shanghai, Shenzhen, Guangzhou, or FTZ). Registered-capital sizing decision. Legal-rep selection and briefing.

Phase two — parallel RO dissolution and WFOE registration (weeks 1-22). RO dissolution: tax-clearance application (longest-pole item, 4-5 months), customs deregistration, SAFE deregistration, AIC deregistration. WFOE registration: name pre-approval, AIC registration (12 weeks for a Shanghai trading WFOE with clean documents), chop carving and registration. EOR bridge for staff work permits during the 2-4 week gap.

Phase three — post-license operational scaffolding (weeks 14-28). RMB and FX bank-account opening (requires legal-rep in-person visit). SAFE FX-capital-account registration. General-taxpayer status application and approval. Customs registration. Import-export operating right registration. Accounting system setup. First fapiao-printer registration.

Phase four — operational handover and first invoicing (weeks 24-32). Customer-facing communication about the new contracting entity. Internal handover from RO accounts to WFOE accounts. Re-papering of customer contracts with the WFOE as counterparty. First customer order processed through the WFOE with VAT-special fapiao issued. Inventory-and-supply-chain transition.

Indicative budget band: For a conversion of this scope, first-year structural budget runs $40,000-150,000 all-in, with the RO dissolution and WFOE registration costs sitting at $20,000-50,000, the general-taxpayer and customs registration adding $5,000-15,000, EOR bridge costs $15,000-30,000 for the staff continuity period, banking and accounting-system setup $5,000-15,000, and legal advisory across the conversion $10,000-30,000 depending on the complexity of customer-contract re-papering. Operating costs after structurally-complete (the WFOE's standalone running cost) run $80,000-250,000 annually depending on staff size, office, and book-keeping scope. The expansion-budget estimator models these against your specific numbers.

Realistic timeline: 7-9 months from project start to first RMB-fapiao invoice issued. The RO dissolution tax-clearance is the longest-pole item and cannot be compressed. The WFOE registration itself is 12-16 weeks for a clean trading scope. Plan for 8 months from green-light to first fapiao; deliver in 7-10 depending on which milestones run on schedule.

Case study match — how the German manufacturer converted RO to WFOE

The structure pattern on this page is what the German manufacturer case study walks through end-to-end. A €18M precision-parts manufacturer had been running a Shanghai Rep Office for seven years with two distributors handling fapiao and customer-facing invoicing. When the top mainland customer's procurement team standardized on direct-invoicing with RMB-fapiao and refused the distributor model, the structural conversation became unavoidable. The fix was a Shanghai trading WFOE registered in parallel with the RO dissolution, general-taxpayer status, customs registration, import-export operating right, SAFE FX registration, and an EOR bridge for the staff work-permit window. End-to-end the conversion ran roughly 8 months. By the end of the first full year on the new structure the business was issuing fapiao, collecting RMB directly, recovering meaningful EUR-equivalent VAT on imports, and starting to think about regional-headquarters status.

The case study covers the specific HS-code classification work, the parallel-track sequencing that kept the staff continuously employed, the customs-and-tax registration sequence after the business license, an honest concession about the HS-code classification work being underestimated and the EOR window being tighter than ideal, and what we would do differently next time. If you are running a Rep Office that is reaching the end of its operational scope, the case study reads as the operational playbook.

Working in this industry?

Tell us your constraints — we'll reply with the partner firm and filing sequence that fits this niche.

Frequently asked questions

Can a Rep Office issue fapiao for customs?

No. Rep Offices can't issue VAT-special invoices, which is what customs and B2B buyers need. This is the most common trigger for the RO-to-WFOE conversion.

How long for the import/export license post-WFOE?

4-8 weeks for the registration with customs, plus 2-3 weeks for foreign-exchange permit registration. After that you can ship under your own name and recover VAT.

Is the FTZ worth the slightly higher registered-address cost?

For pure export operations, yes — bonded zones and FTZ areas have meaningful processing-fee differences. For domestic trading, the FTZ premium often isn't recovered.

Do you have a relevant case study?

Yes — the case-studies index lists four anonymized engagements across DTC, SaaS, industrial, and creator personas.

Or skip the form

Book a call with Mike

30 minutes, Zoom or Tencent Meeting. No discovery-call gauntlet.