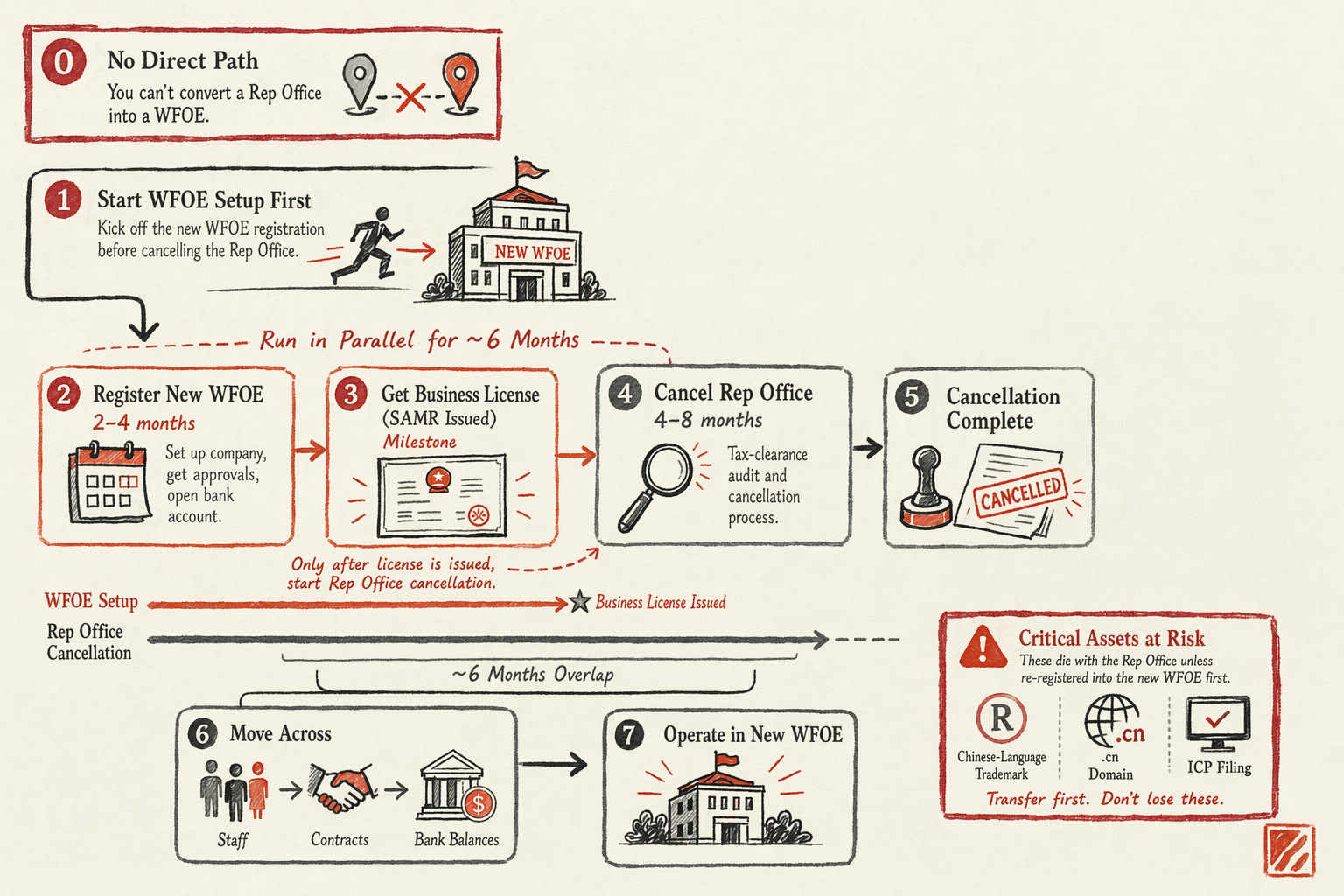

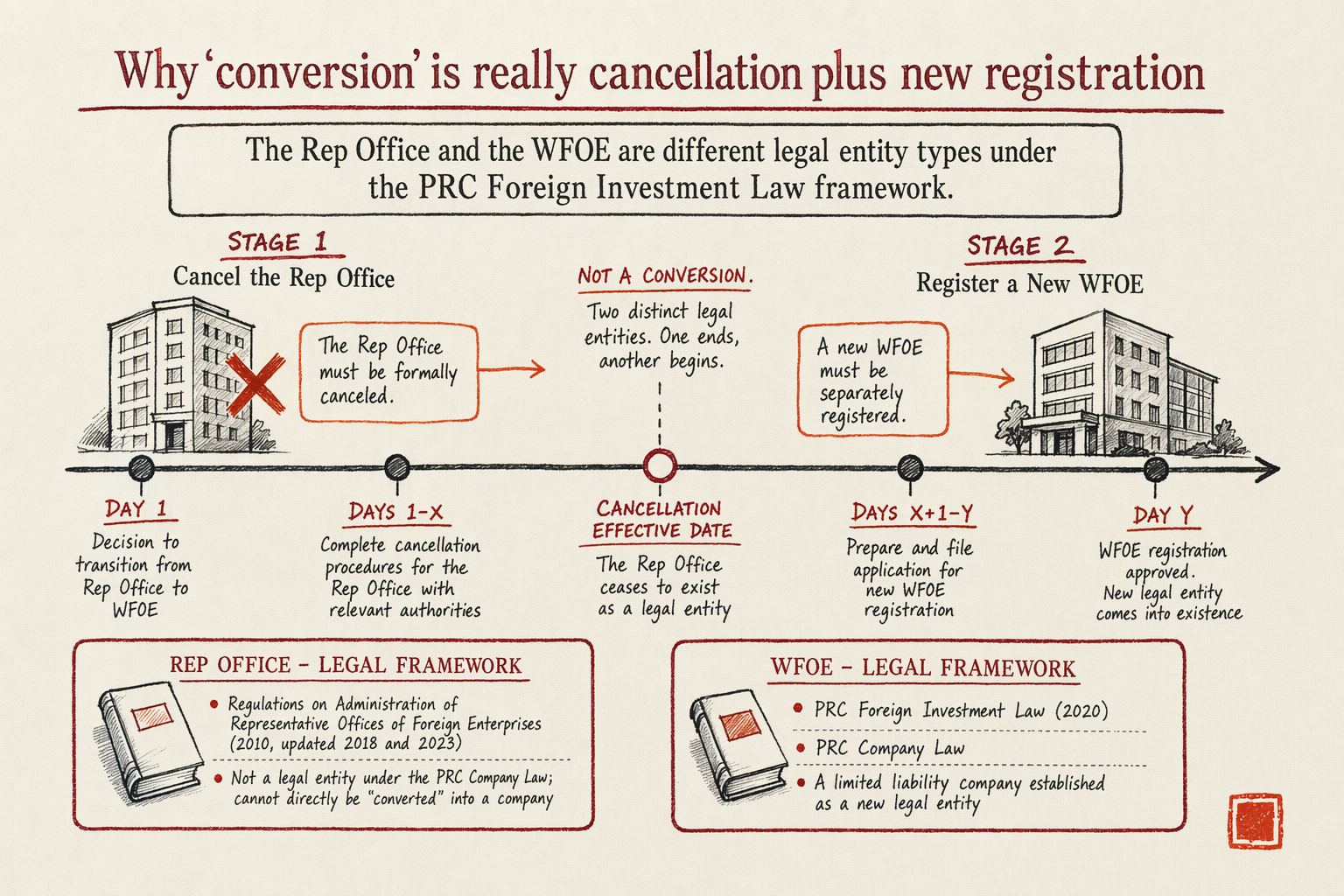

Why 'conversion' is really cancellation plus new registration

The Rep Office and the WFOE are different legal entity types under the PRC Foreign Investment Law framework. The Rep Office is governed by the Regulations on Administration of Representative Offices of Foreign Enterprises (2010, updated 2018 and 2023). The WFOE is governed by the PRC Foreign Investment Law (2020) and the PRC Company Law. Their registration paths diverge at the SAMR (State Administration for Market Regulation, formerly AIC) entry: Rep Offices file under foreign-enterprise representative-office rules; WFOEs file under foreign-investment company rules. Each has its own business license, its own social-credit code, its own bank-account registration, its own tax-bureau enrolment, its own social-insurance registration.

Because they are different entity types, SAMR has no procedure to mutate one into the other. The closest documented mechanism — a 分支机构 (fēnzhī jīgòu, branch) conversion — does not apply between Rep Offices and WFOEs because the Rep Office is not a branch of the foreign parent in a way that maps to PRC branch law. The practical pattern is a parallel two-track: register the new WFOE while the Rep Office is still operational, transition staff and operations across, then cancel the Rep Office on a planned timetable.

This matters because the alternative — cancel the Rep Office first, then start the WFOE — creates a gap of four to eight months during which the foreign brand has no operating presence in mainland China. The gap is long enough for trademark squatters to file against the brand name, for the Chinese-language domain to become a target, for the existing customers to drift, and for any in-China bank accounts to be closed (which they will be, automatically, as part of the Rep Office cancellation).

The Rep Office cancellation procedure

The Rep Office cancellation is the longer half of the migration. Realistic timeline: 4-8 months from kickoff to deregistered final certificate. The procedure runs through five sequential clearances:

- Tax clearance (税务注销). The local State Taxation Administration office runs a final audit covering the past three fiscal years. Any outstanding tax liability — VAT, CIT under the expense-markup regime, IIT for rep-office staff — must be settled before clearance issues. Realistic time: 2-4 months. The audit is more thorough than the routine annual review; partner-firm support on the books is almost always needed.

- Social-insurance and housing-fund clearance. The Rep Office's 五险一金 enrolments for staff are cancelled. Any unpaid contributions must be settled. Staff who will transition to the WFOE get re-enrolled under the new entity. Realistic time: 4-6 weeks running in parallel with tax clearance.

- Customs and FX clearance. If the Rep Office held any customs registrations or had SAFE-side foreign-exchange records, both are closed out. SAFE confirmation that no outstanding cross-border flow obligations exist is a prerequisite for the next step.

- Bank account closure. The Rep Office's bank accounts (typically one basic account and one or two general accounts) are closed. Final balances are reconciled, transferred to the foreign parent or to the new WFOE's accounts (the latter requires the new WFOE to be operational, which is why the parallel-track timing matters). Realistic time: 4-8 weeks once the tax clearance certificate is in hand.

- SAMR deregistration. The final cancellation at SAMR, where the Rep Office's business license is formally revoked and the entity ceases to exist. Once SAMR issues the deregistration confirmation, the Rep Office is closed.

The full cancellation sequence cannot be shortened materially. The tax-clearance audit is the gate; everything else flows from it. Plan 6 months as a realistic baseline; plan 8 if the Rep Office has carried operations for more than three years and has correspondingly more historical records to audit.

Setting up the WFOE in parallel

The WFOE registration runs in parallel with the Rep Office cancellation, not after it. Total WFOE setup timeline: 2-4 months from filing to operational. Combined with the 6-month cancellation, this produces a 6-month overlap window where both entities exist legally and the migration of operations happens across it.

The WFOE-side timeline:

- SAMR business-license filing. Foreign-investor identity documents (apostilled), articles of association, business-scope draft, registered-address documents. The WFOE registers in the city where most operations will be — usually the same city as the Rep Office, but not always. 2-6 weeks for the SAMR business license itself.

- Tax-bureau enrolment. Separate filing at the local State Taxation Administration office. General-taxpayer status, if needed for fapiao issuance at the higher VAT rates, takes an additional 4-8 weeks after the basic enrolment.

- Social-insurance and housing-fund employer registration. Required before any staff can be transitioned across.

- Basic RMB account opening. The legal rep visits the chosen bank. 4-8 weeks. See basic vs general account.

- SAFE foreign-investment registration. If any cross-border capital is moving into the WFOE. See SAFE registration for cross-border FX inflows.

Two operational decisions matter inside this parallel window. First, when do staff transition from the Rep Office's payroll to the WFOE's payroll? The clean cut is the moment the WFOE's social-insurance employer registration completes. Each member of staff gets a single payslip on the old entity, then a single payslip on the new entity, with the transition documented in their employment contract amendment. Avoid running parallel payroll for the same person under two entities; it triggers IIT (Individual Income Tax) reconciliation problems for the staff member at year-end.

Second, when does the operating revenue switch over from Rep Office contracts (which cannot directly invoice in RMB anyway, by Rep Office rules) to WFOE-issued fapiao? As soon as the WFOE's general-taxpayer status is granted and the fapiao printer is delivered. Existing customer contracts get novated from the foreign parent (the contracting party under the Rep Office regime) to the new mainland WFOE. New customer contracts get signed by the WFOE directly.

Protecting the Chinese-language brand and domain in the gap

The single biggest non-obvious risk in a Rep Office cancellation is the gap on protectable Chinese-language IP. Three vulnerable assets need active protection through the migration:

The Chinese-character brand mark. If your brand has a Chinese transliteration filed at CNIPA (China National Intellectual Property Administration) under the Rep Office or its foreign parent, confirm the registration is in the foreign parent's name. CNIPA registrations belong to the named registrant; they do not transfer automatically when the holder is cancelled. If the registration is under the Rep Office's name (which happens when an over-eager local agent files it that way), file an immediate assignment to the foreign parent or directly to the new WFOE before the Rep Office cancellation completes. See Chinese transliteration trademark.

The .cn and .com.cn domains. Domains registered under the Rep Office's identity get re-verified under CNNIC (China Internet Network Information Center) real-name rules if the registrant changes. Plan the domain re-registration into the new WFOE's name before the Rep Office cancellation completes; the re-verification takes 1-2 weeks, but it cannot start until the new WFOE has its SAMR business license.

The ICP filing. ICP filings under the Rep Office are tied to the Rep Office's business license. Once the Rep Office is cancelled, the ICP filing is automatically void. The new WFOE has to file a fresh ICP under its own license, which takes 4-8 weeks for the 备案 (filing). Plan the new ICP filing to land before the Rep Office cancellation completes so there is no window where the mainland-hosted site is unfiled.

None of these are surprises if planned for. All of them turn into emergencies if the Rep Office cancellation runs faster than the WFOE setup. The default broker recommendation is to start the WFOE setup first, get it to the point where its SAMR business license has issued, and only then initiate the Rep Office cancellation. The cancellation will run slower than the WFOE; that asymmetry is the safety margin.

Staff visas, bank accounts, and the 6-month overlap

During the six-month parallel window, three operational concerns dominate.

Z-visa work permits. Foreign staff whose Z-visas are sponsored by the Rep Office cannot have those visas transferred directly to the new WFOE; the work permit is tied to the sponsoring entity. The staff member's existing permit remains valid until its expiry under the Rep Office, but for any renewal during or after the cancellation, the WFOE has to issue a new work-permit invitation, the staff member files for a new Z-visa, and the new permit is issued under the WFOE. Plan around expiry dates. If a permit expires within six months of the Rep Office cancellation kickoff, accelerate the WFOE setup so its work-permit-issuance authority is operational before the renewal window.

Bank accounts. The Rep Office's bank accounts get closed as part of cancellation step 4. Final balances either return to the foreign parent (via a SAFE-registered outbound flow) or transfer to the new WFOE's accounts. The latter is cleaner and faster, but requires the WFOE's basic account to already be open. Sequence: WFOE basic account opens at month 3 of the parallel window; Rep Office balance transfers to WFOE accounts at month 4-5; Rep Office accounts close at month 5-6.

Customer-facing communications. Customers do not need to know the entity is changing. Your contracts, invoices, and email signatures reference the operating brand, which does not change. Only the legal contracting party in the contract signature block changes — from 'X Foreign Corp Representative Office' to 'X Trading (Shanghai) Co Ltd' or whichever WFOE-name applies. Existing contracts get novated; new contracts use the new entity from the day the WFOE is operational. Most customers will not notice unless you tell them; the brand experience stays continuous.

For the topic hub covering the entity-choice landscape see WFOE vs Rep Office vs HK Ltd. For the parent service see China company formation. For the tax framework around the expense-markup regime that drives most migrations see Rep Office 20% expense-markup tax.

In plain English

If you only read one paragraph: There is no direct path that converts a Rep Office into a WFOE. You cancel the Rep Office and register a new WFOE in parallel, running both for six months while you move staff, contracts, and bank balances across. The cancellation takes four to eight months because of the tax-clearance audit; the new WFOE takes two to four months to set up. Start the WFOE setup first, get the SAMR business license issued, and only then begin the Rep Office cancellation, so the slower side acts as a safety buffer. The biggest non-obvious risks are the Chinese-language trademark, the .cn domain, and the ICP filing — all of which die with the Rep Office unless re-registered into the new WFOE first.

Related

7 min read

WFOE vs Representative Office vs Hong Kong Limited

Scope of permitted activity, minimum capital reality, tax exposure side-by-side, deregistration cost, conversion paths between structures.

6 min read

Representative Office 20% Expense-Markup Tax Explained

The deemed-profit tax that makes Rep Offices expensive — how it's calculated, why it surprises foreign founders, when an RO still makes sense.