Industry view

Cross-Border E-Commerce: Tmall Global, JD Worldwide, Douyin Global

Bonded warehouse model, platform selection, TP and POP fees, RMB settlement vs offshore. Cross-border vs domestic crossover threshold.

Email Mike—

Y1 cost band

Mike's running benchmarks

—

Time to first revenue

Mike's running benchmarks

—

Common pivot at month 12

Mike's running benchmarks

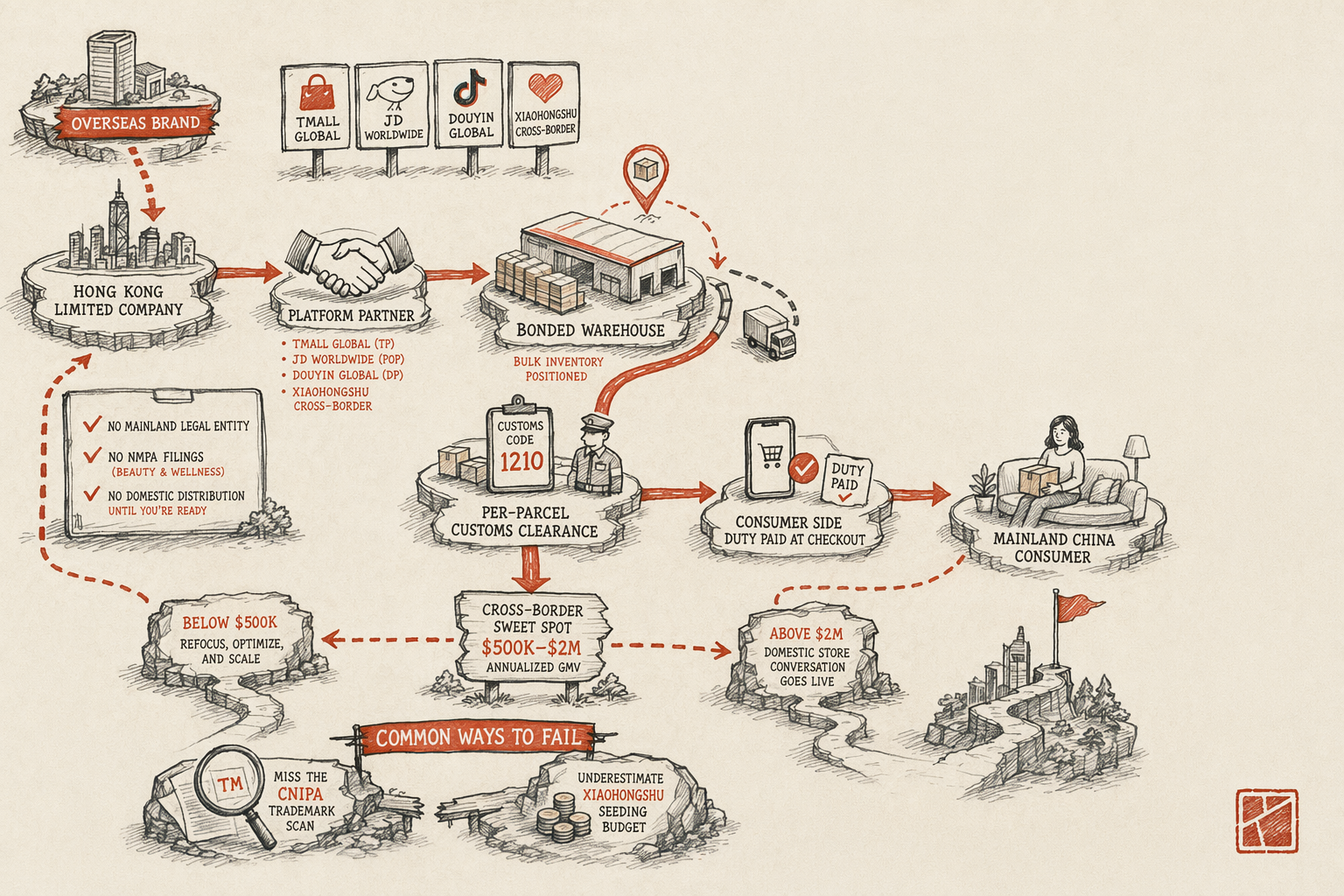

Mainland Chinese cross-border e-commerce — the regulated channel through which overseas brands sell physical consumer goods to mainland consumers via bonded warehouses, per-parcel customs clearance, and platform-side fulfillment — is the most-used market-entry path for foreign consumer brands. The reason is structural: cross-border bypasses NMPA filing for cosmetics, bypasses domestic-flagship inventory commitments, bypasses the need for a mainland operating entity, and bypasses most of the regulatory friction that domestic distribution carries. It is not a loophole; it is an explicit regulatory channel that the State Council and the General Administration of Customs have built and refined since 2014 to support overseas-brand market access.

The platforms that operate in this channel — Tmall Global (天猫国际), JD Worldwide (京东海外购), Douyin Global, Xiaohongshu's cross-border channel, and a handful of smaller specialty platforms — collectively cover the mainland e-commerce buyer base for foreign consumer goods. Each has different category strengths, different fee structures, and different operating-partner ecosystems. This page walks through what cross-border sellers actually need, the customs and regulatory layer that defines the channel, the entity-structure pattern that fits most launches, the rejection-and-stall patterns at platform enrollment, and the realistic timeline and budget for a sequenced engagement.

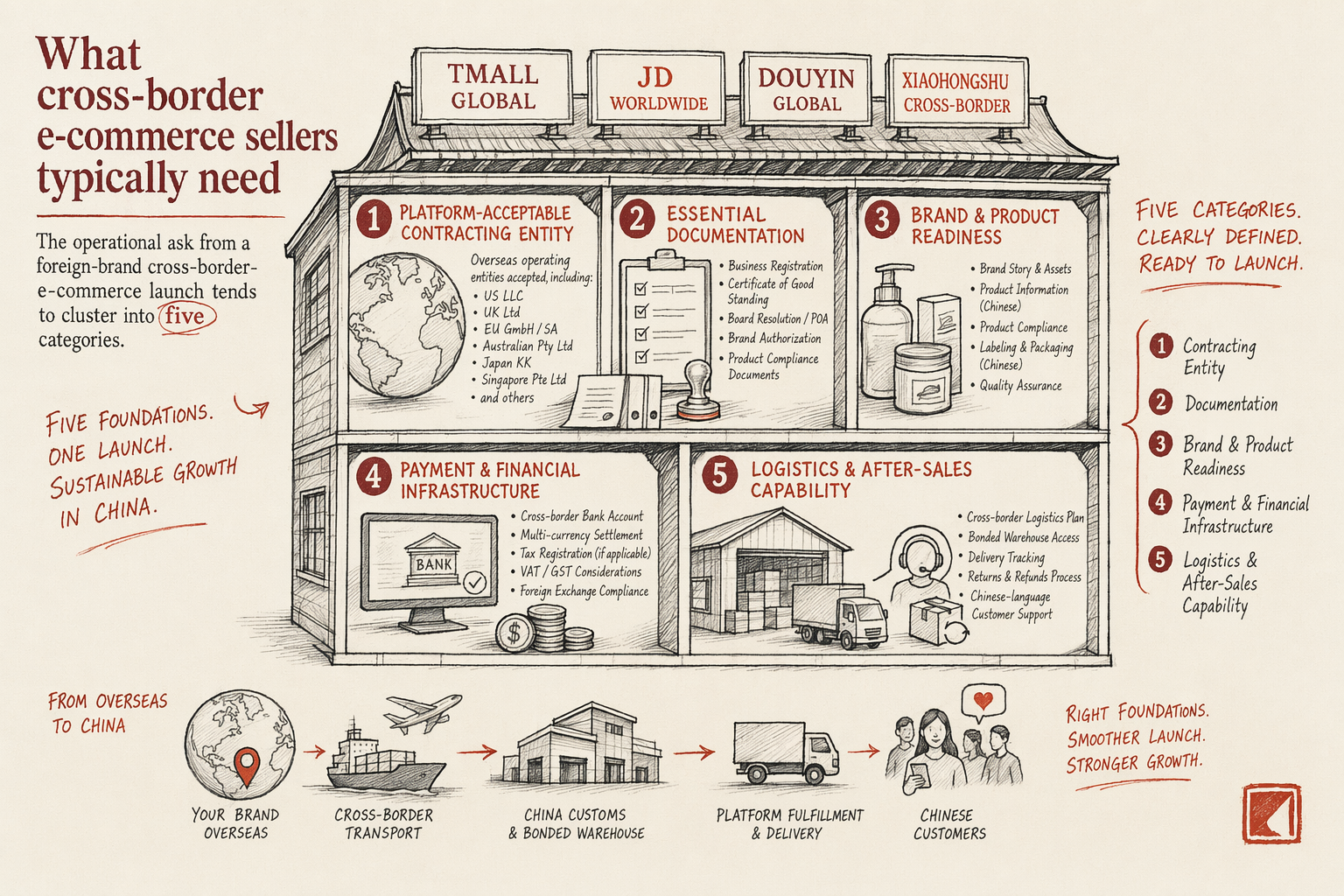

What cross-border e-commerce sellers typically need

The operational ask from a foreign-brand cross-border-e-commerce launch tends to cluster into five categories.

One — a platform-acceptable contracting entity. Tmall Global, JD Worldwide, Douyin Global, and Xiaohongshu cross-border each accept overseas operating entities (US LLC, UK Ltd, EU GmbH/SA, Australian Pty Ltd, Japan KK, Singapore Pte Ltd, and others) as the contracting party. The Hong Kong limited company is the most common entity because the document chain is the format the platforms see most often and the bilingual brand-name plate aligns cleanly with platform-side transliteration norms. The HK Ltd holds the platform agreement, the brand-authorization chain that flows to the platform partner, the mainland trademark portfolio, and the bonded-warehouse fulfillment contracts.

Two — a cleared CNIPA trademark register in the relevant classes. Trademark provenance is a hard gate at platform enrollment. The required filing class depends on the product category — Class 3 (cosmetics), Class 5 (pharmaceutical and dietary), Class 25 (apparel), Class 28 (toys and sports), Class 30 (food and confectionery), Class 35 (advertising and retail services). Most consumer-brand launches require filings in 2-4 classes. A squatter holding the senior mark on your brand in any required class blocks enrollment until the trademark situation is resolved through cancellation action or sufficient defensive sub-class coverage. The pre-launch CNIPA scan is the diagnostic; the trademark-squatting scanner is the cheap version of the scan.

Three — a working relationship with a platform partner. Tmall Partners (TP), JD Partners (POP), and Douyin Partners (DP) are the accredited third-party operating agencies that handle store setup, photography, customer service, platform operations, and ad management on behalf of overseas brands. Each platform has its own partner ecosystem; partners specialize by category. TP selection in particular is a strategic decision — the partner you choose has working relationships with the platform-side reviewers for your specific category, which materially affects enrollment success rate and ongoing platform operations quality. Run an actual selection process across 3-5 candidate partners; ask for two reference calls with recent comparable launches; review the fee model (flat retainer plus percentage-of-GMV, pure percentage, or hybrid) against your expected scale.

Four — a bonded-warehouse fulfillment arrangement. The cross-border bonded-warehouse model requires bulk inventory positioned in a mainland bonded zone (the major ones are Hangzhou, Ningbo, Zhengzhou, Chongqing, Tianjin, Guangzhou, Shenzhen, Shanghai, with additional regional zones operating). The bonded-warehouse operator handles per-parcel customs clearance under the 1210 customs code, per-parcel logistics fulfillment to the consumer, and per-parcel returns processing. Operator selection is partly geographic (which mainland city matches your platform's preferred fulfillment integrations and your customer-base geography) and partly capability-based (some operators specialize in beauty, others in apparel, others in electronics).

Five — a content and amplification layer for discovery. Mainland consumer-goods commerce runs heavily on content-first discovery via Xiaohongshu, with secondary discovery flow through Douyin short-form content and Bilibili long-form content. Cross-border brands that enroll on Tmall Global without a Xiaohongshu content layer typically see flat conversion from platform traffic. The minimum operational answer is a Xiaohongshu brand account (cross-border verified) with consistent content cadence, seed-content engagement with paid KOC (Key Opinion Consumer) network, and selective KOL (Key Opinion Leader) partnerships for amplification. The Xiaohongshu setup topic covers the playbook.

The vertical's specific regulatory layer — 9610/1210 customs codes, bonded zones, per-parcel duty

Cross-border e-commerce in mainland China operates under a specific regulatory regime that is distinct from both general international trade and domestic mainland commerce. Three layers define the channel.

9610 and 1210 customs codes. The cross-border e-commerce customs codes are the regulatory identifiers that define how the channel works. 9610 (海关跨境电商直邮, also called B2C direct mail) covers individual cross-border parcels shipped directly from overseas to the mainland consumer, customs cleared per parcel at the receiving customs office. 1210 (海关跨境电商保税进口, also called bonded import) covers inventory shipped in bulk to a mainland bonded zone, customs cleared per parcel at the time of consumer purchase. The 1210 model is the typical Tmall Global / JD Worldwide / Douyin Global structure because the bonded-warehouse positioning gives much faster consumer-side delivery (1-5 days versus 7-21 days for direct mail). 9610 is used for low-volume long-tail SKUs where bonded-warehouse positioning is not economical, or as a launch-phase model before bonded inventory commits.

Bonded zones and the comprehensive cross-border pilot zones. The bonded zone (保税区) and the comprehensive cross-border e-commerce pilot zone (跨境电商综合试验区) infrastructure has expanded materially since 2014. Major bonded-zone cross-border e-commerce hubs include Hangzhou (the original pilot zone and still the largest for beauty), Ningbo (apparel-strong), Zhengzhou (electronics and general goods), Chongqing (inland-distribution-focused), Tianjin (northern coast), Shanghai, Shenzhen, Guangzhou, and additional regional zones. Each zone has slightly different customs-clearance processing times, slightly different platform-fulfillment-partner ecosystems, and slightly different per-parcel duty calculation conventions. The choice of bonded zone is part of the platform-partner discussion — most platform partners have preferred fulfillment-zone integrations.

Per-parcel duty and the consumer-side payment. Cross-border e-commerce parcels pay duty calculated under the cross-border duty schedule (跨境电商综合税), which is generally lower than the general-trade import duty rate for the same goods. The duty is calculated per parcel based on the declared value of the goods, with caps on per-parcel value (currently RMB 5,000 per parcel) and per-person annual value (currently RMB 26,000 per consumer per year). The consumer pays the duty at checkout — it is added to the final price the consumer sees and remitted to customs at parcel clearance. The brand does not absorb the duty, but the duty does affect price elasticity at the consumer level. Plan SKU pricing with the all-in consumer-side price (product + duty + shipping if applicable) in view.

Cross-border negative list. The Ministry of Commerce maintains a negative list (跨境电商零售进口商品负面清单) of goods that cannot be imported through the cross-border channel. The list is updated periodically and currently excludes certain drug categories, some medical devices, certain food products with mainland-specific labeling requirements, products containing prohibited ingredients, and a few other regulated categories. Most consumer goods are eligible. Check your SKU mix against the current negative list during diligence; mainland-specific SKU adjustments may be needed if any line items are on the list.

Typical entity-structure pick — HK Ltd plus platform partner plus bonded warehouse

The default structure for first-time foreign-brand cross-border e-commerce market entry runs three components.

Component one — a Hong Kong limited company as the dedicated mainland-market brand entity. The HK Ltd holds the platform agreement, the brand-authorization chain that flows to the platform partner, the CNIPA trademark portfolio, the bonded-warehouse fulfillment contracts, and the cross-border payment-receipt flow for platform settlements. Setup runs under €3,000 all-in; annual carry €4,000-7,000 for a lean entity. For brands at meaningful scale ($2M+ annual GMV) the HK layer pays for itself in payment-rail and trademark-portfolio benefits alone; for smaller brands the HK layer is sometimes deferred until volume justifies it, with the home-country operating entity contracting directly with the platform in the launch phase.

Component two — a platform-partner operating relationship. Tmall Partner, JD Partner, Douyin Partner, or Xiaohongshu cross-border operator (the partner ecosystem differs by platform; some agencies are accredited across multiple platforms). The partner handles day-to-day store operations, customer service, photography, copy, ad management, and the platform-side relationship. Partner fees structure varies: full-service partners typically charge a flat retainer plus 12-25% of GMV depending on services scope; lean operations-only partners charge 5-12% of GMV with the brand handling more of the content and ad work in-house. Select based on category specialization, reference base, and fee-model fit to your operating model.

Component three — bonded-warehouse fulfillment arrangement. Bonded-warehouse operator handles per-parcel customs clearance, per-parcel logistics fulfillment, and per-parcel returns processing. Fees typically run 4-7% of GMV. Operator selection is partly geographic (matching platform-fulfillment-integration preferences and customer-base geography) and partly capability-based (category specialization, integration with the platform's preferred logistics carriers, returns-processing capability). For multi-platform launches, the bonded-warehouse operator should ideally handle inventory across all enrolled platforms from a single bonded position to avoid inventory fragmentation.

What is explicitly not in the default structure: no mainland WFOE, no domestic Tmall flagship, no NMPA registration. Each of those activates at a different stage. The mainland Tmall flagship becomes relevant when cross-border GMV crosses the $500k-2M threshold and the bonded-warehouse markup is materially compressing margin. The NMPA filing activates alongside the domestic flagship for beauty and wellness goods. The WFOE conversation activates when the domestic-distribution decision is made — at that point a mainland operating entity becomes structurally necessary. Until then, cross-border is the right channel.

Common rejection patterns specific to cross-border e-commerce

The rejection and stall patterns specific to cross-border e-commerce launches cluster around four themes.

Pattern one — trademark squatter blocking platform enrollment. The most common single stall. A third party holds the senior CNIPA mark on the brand in the required class, and the platform-side trademark gate rejects the enrollment. The fix is the pre-launch CNIPA scan and the defensive-filing-plus-cancellation-action sequence. The EU skincare case study covers this pattern in operational detail.

Pattern two — bonded-warehouse classification mismatch. The bonded-warehouse intake misclassifies the SKU under an HS code that does not match the platform-side product-category record, or the per-parcel duty calculation is off because the SKU declared value at intake differs from the listing price at checkout. Parcels are held in customs review, sometimes pushed back to the consumer with a duty surprise that the consumer rejects. The fix is to work with the bonded-warehouse operator's customs declarant to pre-map the full SKU catalog to correct HS codes and to confirm the declared-value-to-listing-price chain matches before the first bulk shipment ships.

Pattern three — store-type election mismatch with trademark status. The platform-partner submits the enrollment as an overseas-brand official store (海外旗舰店) — which has the strictest trademark-provenance requirements — when the trademark situation does not yet support an official-store classification. The reviewer rejects the application. The fix is to match the store-type election to the trademark status at the time of submission: overseas-brand authorized store (海外授权店) for trademark-receipt-only status, overseas-brand official store for fully-certificated status. The partner should make this distinction; if they do not, push back on the recommendation.

Pattern four — content-copy claim-language failure. Product copy makes a claim that the platform-side reviewer flags as medical (re-classifying the product), special-purpose without supporting registration (whitening, anti-aging for cosmetics), or otherwise prohibited (specific outcome promises with quantitative claims). The listing is rejected or held pending claim-language revisions. The fix is to build the copy library with mainland-claim rules in mind from the start, and to have the platform-partner pre-screen claim language as part of pre-enrollment work. This pattern overlaps materially with the cosmetic-brand vertical; the cosmetic-brands industry page covers the claim-language layer in more detail.

The bundled engagement — sequence, indicative budget, realistic timeline

For a foreign consumer brand at home-country revenue of $5-50M annual launching mainland cross-border e-commerce, the bundled engagement covers these sequenced workstreams.

Phase one — diligence and entity (weeks 1-6). CNIPA trademark scan in relevant classes. Cross-border negative-list check against SKU mix. HK Ltd incorporation. CNIPA defensive filings; cancellation-action prep if a squatter is identified. HK bank-account introductions and cross-border payment processor setup.

Phase two — platform partner selection (weeks 4-10). Platform shortlist (Tmall Global, JD Worldwide, Douyin Global, Xiaohongshu cross-border — typically launching on 2-3 of these in parallel). Platform-partner shortlist for each chosen platform (3-5 candidates per platform). Reference calls, fee-model comparison, engagement-letter execution. Bonded-warehouse operator selection.

Phase three — content and operational preparation (weeks 8-14). Product photography localized for mainland platform norms. Product copy localization and claim-language compliance review. Store-design templates prepared per platform. Brand-authorization documentation chain from HK Ltd downstream. Xiaohongshu seed-content plan and initial KOC engagement.

Phase four — enrollment and launch (weeks 12-18). Tmall Global enrollment with the new structure. JD Worldwide enrollment in parallel. Douyin Global enrollment in parallel if applicable. Xiaohongshu cross-border brand account verification. Bonded-warehouse inventory positioning. Multi-platform store-build. Live to consumers in weeks 16-20.

Phase five — operations and amplification (week 16 onwards). Xiaohongshu content cadence operational. KOL partnerships activated for amplification. Platform-side ad-management activated. Customer service playbook live across all enrolled platforms. Cross-channel analytics and inventory-allocation processes established.

Indicative budget band: For a multi-platform cross-border e-commerce launch of this profile, the first-year structural budget runs $60,000-200,000 all-in, before inventory and paid-media spend. Breakdown: HK Ltd setup and first-year carry $8,000-15,000; CNIPA filings across 3-4 classes $2,500-8,000; cancellation-action work if needed $5,000-15,000; platform-partner setup fees and first-year minimum commitments across 2-3 platforms $20,000-80,000; photography and copy localization $10,000-30,000; bonded-warehouse onboarding $5,000-15,000; Xiaohongshu seed-content and initial KOC engagement $10,000-40,000. Inventory and paid-media are separate budget categories sized to the GMV target.

Realistic timeline: 14-20 weeks for a clean multi-platform engagement. Trademark complications can extend the timeline by 6-12 weeks. Multi-platform launches (Tmall + JD + Douyin + Xiaohongshu in parallel) typically run on the same overall timeline as single-platform because the documentation overhead overlaps materially across platforms. To model the budget against your specific situation, run the expansion-budget estimator.

Case study match — how the EU skincare brand cleared Tmall Global enrollment

The structure pattern on this page is what the EU skincare brand case study walks through end-to-end. An €8M-GMV EU skincare brand had been rejected three times on Tmall Global over a single quarter — trademark gap, document mismatch, wrong store-type election. The fix was a Hong Kong limited company above the EU operating entity, CNIPA defensive filings in Class 3 and Class 35 plus a parallel three-year non-use cancellation action against the squatter, a working Tmall Partner relationship after a real selection process, and a clean resubmitted enrollment package. The submission cleared review on the first attempt under the new structure. The brand launched on Tmall Global inside 14 weeks and crossed mid-seven-figures RMB GMV in the first 12 months.

The case study covers the three specific reasons the earlier attempts failed, the full-WFOE path some agencies would have pushed and why we ruled it out, the four-component structure that worked, and honest concessions about what we would do differently next time. While the case study is beauty-specific, the platform-enrollment and structure pattern generalizes to other consumer-goods verticals — apparel, accessories, household goods, food and beverage, electronics. The specific class filings differ; the structural sequence is the same.

Working in this industry?

Tell us your constraints — we'll reply with the partner firm and filing sequence that fits this niche.

Frequently asked questions

Do I need a Chinese entity for cross-border e-commerce?

No. Tmall Global, JD Worldwide, and Douyin Global are explicitly built for overseas brands without a mainland entity. You sell through a Tmall Partner (TP) or directly with a foreign-entity contract.

What does the bonded-warehouse model actually cost?

Bonded-warehouse storage and per-order fulfillment runs 4-7% of GMV depending on volume. Tmall Partner fees add 8-30% depending on services. Plan for 25-35% blended deduction from gross before margin.

When should I graduate to a domestic store?

Typically when cross-border GMV exceeds $500k/yr and you want to (a) avoid the bonded-warehouse markup, (b) sell categories restricted on cross-border, or (c) ship at faster speeds than bonded customs clearance allows.

Do you have a relevant case study?

Yes — the case-studies index lists four anonymized engagements across DTC, SaaS, industrial, and creator personas.

Or skip the form

Book a call with Mike

30 minutes, Zoom or Tencent Meeting. No discovery-call gauntlet.